By Chris Becker

A big spike in US interest rates overnight still couldn’t hold back the Dow making a new record high, although the broader S&P500 failed to get over 3000 points again. European stocks continued to wobble while the USD barely moved following the latest core inflation data.

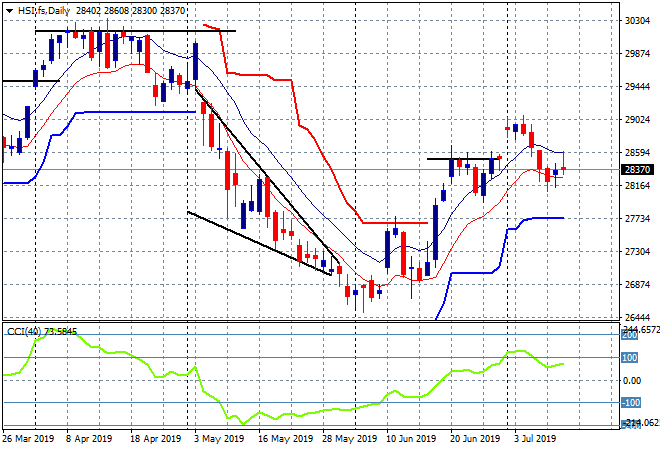

Looking at the action in Asia yesterday, where the Shanghai Composite was unable to get traction again, treading water to be up only a handful of points, closing at 2917 or barely 0.1% higher. The Hang Seng Index however continued its come back with a solid 1% rise, closing at 28431 points, just below the previous set of highs at 28500 as it bounces off support at 28000. The daily chart still looks quite relaxed here however, with prices within the sideways moving average band, so I’m not expecting much upside today, watching the high moving average level at 28600 for a possible breakout: