By Chris Becker

A much firmer response from the risk on crowd overnight as US stocks pushed to new highs while US interest rates plumbed new lows. Sentiment was helped on bond markets at least by nominations to the ECB and Fed, with Christine Lagarde to become the next ECB president. Treasury yields dropped even further as the US trade balance cratered again despite Trump’s trade war strategy of throwing tariffs at everything to shore up the hole.

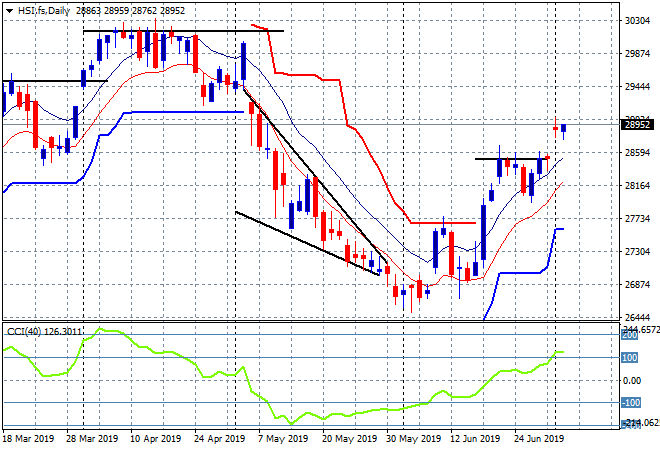

Looking at the action in Asia yesterday where the Shanghai Composite fell over 1% to close just above the 3000 point barrier, barely holding on to its previous bounce-back. The Hang Seng Index slipped slightly to 28855 points, unable to make good on the previous daily high as expected, but still holding on above the breakout area at 28500 or so. Momentum remains positive and with a good lead overnight we should see a better advance today: