Trump is putting his foot into the trade war mouth with more rhetoric overnight that has startled markets again with most Asian equities stumbling today. Luckily, higher than expected Apple earnings are seeing US futures rise instead, but tonight’s July Federal Reserve meeting will be keenly watched by all, especially after the better than expected consumer confidence figures recently.

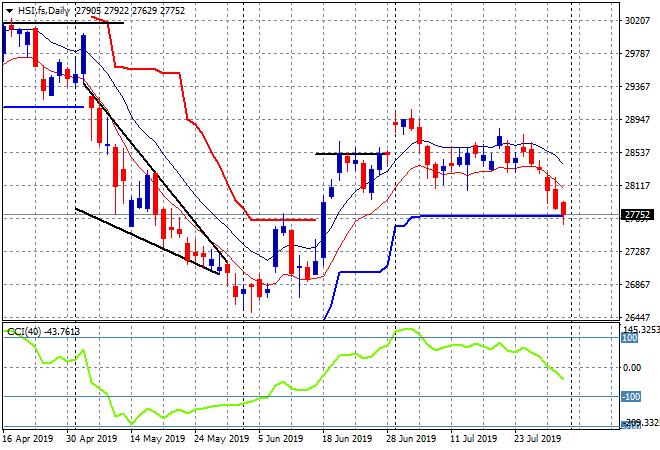

Chinese stocks are off the worst, with the Shanghai Composite falling 0.7% to be at 2932 points while the Hang Seng Index is buckling under internal pressure with another new daily low, losing 1.3% to finish at 27777 points. This puts it right on ATR daily support and ready to breakdown to a new monthly low:

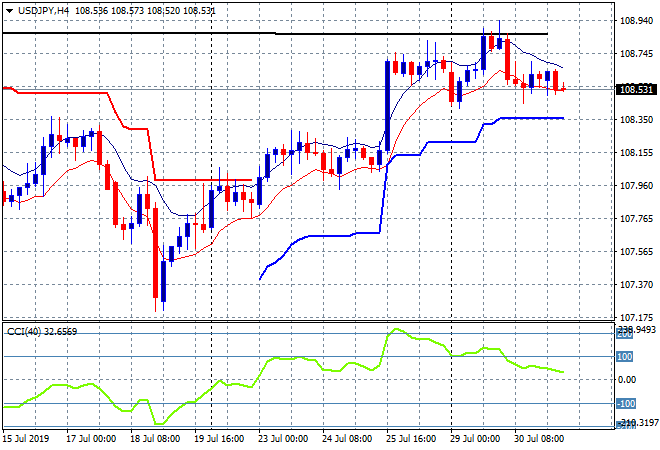

Japanese share markets are also under pressure with the Nikkei 225 closing 0.8% lower to 21521 points despite a steady Yen. The USDJPY pair remains stuck at the mid 108’s before tonights FOMC meeting and remains well below the weekly resistance level above at the 108.90 level:

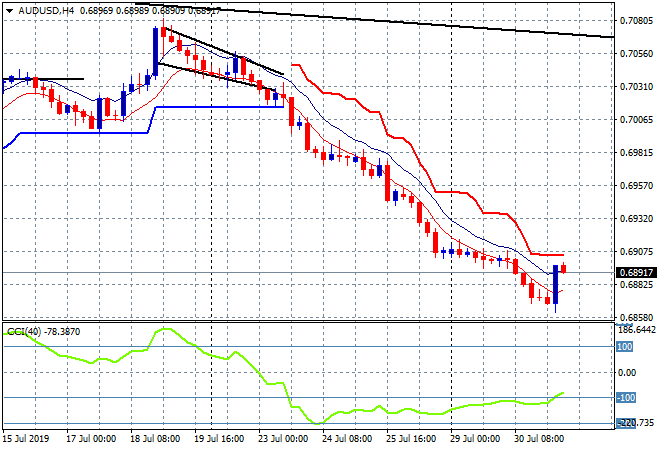

The ASX200 has come back from its recent record high, absorbing today’s CPI print with a 0.4% loss, closing at 6812 points. The Australian dollar lifted on the CPI print but it wasn’t much in the scheme of things, hovering just below the 69 handle before going into the City open and still looking set to return to its 68.50 recent low:

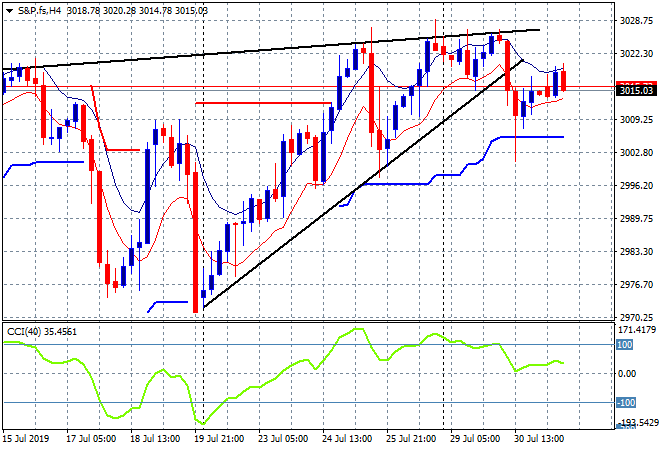

S&P and Eurostoxx futures are up 0.2% going into the European session with the S&P500 four hourly chart still displaying a possible bearish rising wedge pattern as price hovers just above the previous high near 3020 points:

The economic calendar is packed tonight, but will focus squarely on the FOMC meeting after absorbing German unemployment, European CPI and the latest DOE oil inventory numbers. Got to stay up late!