Following China GDP’s dramatic slowing to just 6.2% YoY – the slowest since record began – there was a delightful surprise to appease those who are wondering whether record credit injections and more easing measures than during the financial crisis had any effect at al

China retail sales and industrial production rebounded handsomely with the former spiking 9.8% YoY – the most since March 2018.

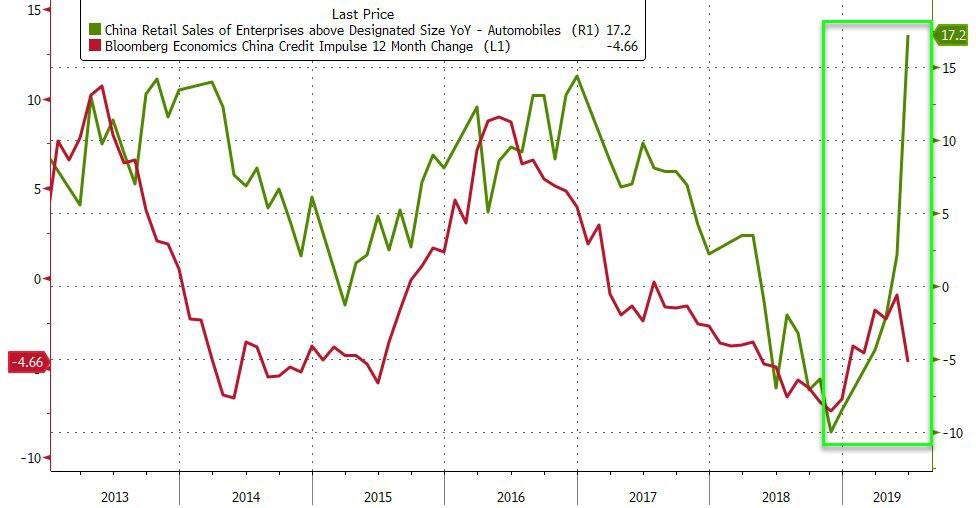

There’s just one thing though – the entire surge in retail sales (and industrial production) seems to have been triggered by an almost unprecedented sudden surge in auto sales to large (state-owned) enterprises…

A 17.2% YoY explosion in sales to SEOs (up from just 2.1% in May) – the most since August 2011 – is almost too good to be believed (ok forget almost, it is too good to believe and seems like pure top-down manipulation of the data – whether sales were effectuated or not), echoing the kind of forced buying rush that occurred in 2009.

And that did not end well.

However, absent considerably more liquidity, forced credit injections, or a miracle, Auto sales are about to hit a wall as China’s credit impulse begins to slow…

Finally, no matter what China does to ‘flatter’ its data and project economic might in the face of Trump tariffs and a collapsing ponzi scheme, the single stat that is hardest to fake (and easiest to see reality) is the dramatic decline in the marginal productivity of debt.As John Rubino recently noted, China, like the US, is getting progressively less bang for each newly-borrowed buck. There’s a point at which new borrowing doesn’t just product less wealth but actually destroys it. The US and China are heading that way fast, while Europe might be there already.

As Evans-Pritchard, notes, the result is “maximum vulnerability.”

I told you not believe yesterday’s data. There’s more from Westpac on where the growth is really coming from. As noted yesterday, total social financing is grinding higher:

Advertisement

And it is all going into empty apartments not infrastructure:

But not via traditional private sector channels of shadow banking:

Prof. Gan’s striking estimate that 65 million urban residences — or 21.4% of housing — stand unoccupied was published in a report in December. The proportion is up from 18.4% in 2011, driven by a rise of vacancies in second- and third-tier cities, where demand is relatively weaker and speculative activities are more prevalent than in Shanghai, Shenzhen, Guangzhou and Beijing.

Prof. Gan warns of potential financial risk from the rising number of vacant houses. Of the 22.9 trillion yuan ($3.4 trillion) of outstanding mortgage debt held by Chinese people as of the end of 2017, 47.1% of that is tied up in residences that now stand empty.

In other words, almost half the bank loans are tied to housing assets that are neither being lived in nor churning out rental income. According to the stress test conducted by the professor, a 5% fall in housing prices would take away 7.8% of the actual asset value of occupied houses, but 12.2% for unoccupied houses. “If housing prices keep on falling, the damage to unoccupied residences accelerates even more than the occupied [ones],” Prof. Gan said in the report.

In other words, China is doing the exact opposite of what it needs to do to lift itself beyond the middle income trap. You know, “rebalancing” and all of that. It is instead quadrupling down on building apartments to nowhere driven by centrally planned state owned enterprises that are, over time, bogging its economy’s productive capacity into a debt quagmire from which it will never emerge.

Advertisement

Indeed, the capital misallocation and income destruction at the heart of China’s empty apartments boom is analogous to the military spending waste that destroyed the centrally planned Soviet economy in the 1980s. It is therefore amusing to read the following from the CPC foghorn today:

By exaggerating China’s GDP growth slow-down, the US has sent a message, signaling that Washington is anxious about the ongoing trade war. They have paid close attention to each and every single change China has experienced, hoping to find long-awaited signs of crippling behavior.

Driven by such anxieties while strategizing Trump’s 2020 re-election campaign, the White House administration has repeatedly overblown China’s trade war losses, fabricating evidence and “facts” to sway public opinion.

In recent years, China’s economy has experienced soft fluctuations and reduced double-digit growth, characteristics that were already in place before the US-launched trade war. The changes today are a natural reaction to national economic restructuring and continued upgrades. The trade war is merely an extra variable among normal circumstances. Even though the trade conflict has stretched for over one year, China’s GDP growth has remained above 6 percent, a figure most major world economies crave. The country’s economic performance has continued on within a reasonable range.

Such facts demonstrate that China’s economy will remain firm and resilient during attrition warfare.

The CPC may be able to force grow empty apartments for a while yet but by doing so it sure ain’t winning any economic war in the long run.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.