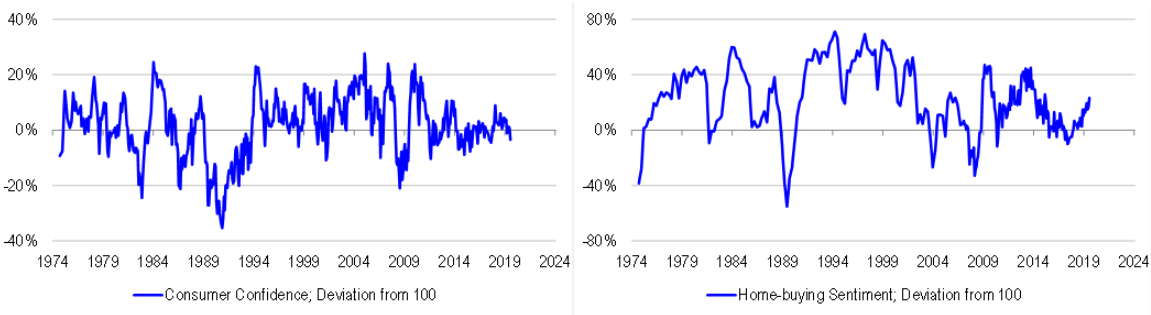

Consumer confidence came in well below expectations, falling to a 2-year low of 96.5 in early July from 100.7. Historically, levels below 100 are supposed to be consistent with weakness in per capita spending. Confidence has not bounced after the election or multiple rate cuts. Quite the opposite in fact.

Why might consumers be so downbeat? We can think of a few reasons:

Tax cuts are not all they are cracked up to be. On paper, LNP tax cuts are supposed to total $7.1 billion. But not all of the tax cuts are new. Indeed, only half of the $7.1 billion is new. And then there is bracket creep to consider over the past year, which could be worth $2-3 billion. The net stimulus is arguably quite small.

Job losses. Our proprietary labour market indicator has been pointing to rising unemployment for some time. Perhaps we are now starting to see weak demand filter through to the broader labour market. Job losses do not have to be particularly large in magnitude to cause over-leveraged households to worry about their financial security and restrain spending.

Payment shocks from interest-only mortgages resetting to principal plus interest terms. We doubt that the incremental effect of resets is that large in isolation – but payment shocks are another straw that could break the camel’s back.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.