Terrific stuff today from Zero Hedge on China’s little Minsky moment:

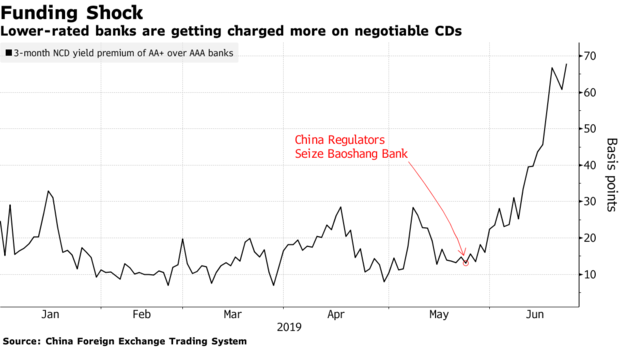

Ever since the unexpected failure of China’s Baoshang Bank in late May, which caused a freeze in the interbank market among smaller, less credible (and government backstopped) banks, and which sent rates on Negotiable Certificates of Deposit (NCDs), various bank bonds and assorted report rates sharply higher…

… investors have fretted that China appears on the verge of a “Lehman moment”, where wholesale interbank liquidity and overnight funding markets suddenly lock up. The reason for this, as we explained last month, is that China’s short-term lending market for banks and other financial institutions has for years operated under the assumption that Beijing wouldn’t allow big losses in the event of defaults or insolvencies (hence the reason why Baoshang’s failure was a shock). That confidence has been shaken by regulators’ unusual public takeover of the troubled Chinese bank near Mongolia last month, and the even more stunning public admission by the central bank that “not all of Baoshang Bank’s liabilities would necessarily be guaranteed.”

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.