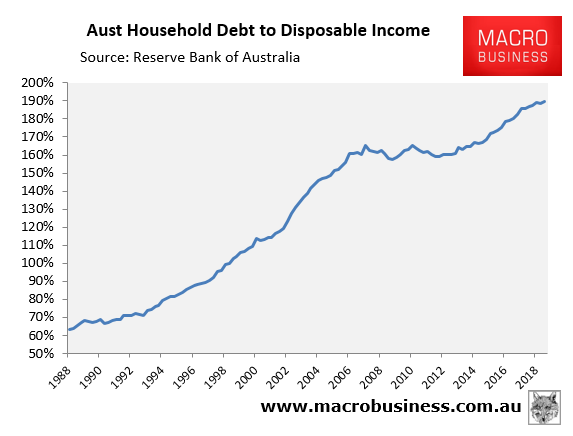

One of the ramifications of Australia having one of the world’s largest household debt loads, which is running at 190% of disposable income:

Is that when wage growth is anaemic and an economic downturn hits, it leaves highly indebted households exposed to bankruptcy.

With this background in mind, a new report from industry research firm IBISWorld predicts that debt collection will be the next boom sector for Australia as the economy slides:

IBISWorld senior analyst Jason Aravanis told news.com.au this industry will perform strongly when, well, there’s debt to collect.

“When the economy starts to slow down you’re likely to see more households defaulting on their debt and businesses hire more debt collectors,” he said.

“It’s certainly not a good sign.

“Australia might be particularly exposed to this trend because our household debt is very high compared to disposable income — it’s at a record high of about 190 per cent right now.

“The problem with having really high household debt is it becomes very difficult when you’ve got low wage growth like we do right now.”

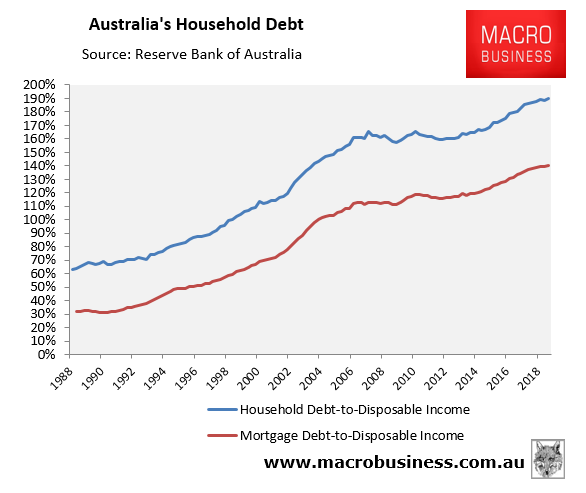

By far the largest component of Australia’s household debt is mortgages, whose outstanding debt was a record high 140% of income as at March 2019:

According to Martin North, Mortgage Stress hit record highs in June, translating into more than 1,063,000 households across Australia, and nearly 71,000 at risk of default in the year ahead:

Record high debt, real wage falls, and a weakening economy are a toxic combination.