The Australian dollar is in free fall across the board:

Advertisement

Gold was strong approaching the FOMC:

Oil too:

But not metals:

Advertisement

Miners were mixed:

EM stocks sank:

But junk was OK:

Advertisement

Treasuries were bid:

The bund curve flattened:

Aussie bonds were strong:

Advertisement

But European stocks were belted and US wilted:

US data was rock solid. Leading us off, Conference Board consumer confidence surged:

The Conference Board Consumer Confidence Index® rebounded in July, following a decrease in June. The Index now stands at 135.7 (1985=100), up from 124.3 in June. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – increased from 164.3 to 170.9. The Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – increased from 97.6 last month to 112.2 this month.

“After a sharp decline in June, driven by an escalation in trade and tariff tensions, Consumer Confidence rebounded in July to its highest level this year,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers are once again optimistic about current and prospective business and labor market conditions. In addition, their expectations regarding their financial outlook also improved. These high levels of confidence should continue to support robust spending in the near-term despite slower growth in GDP.”

Advertisement

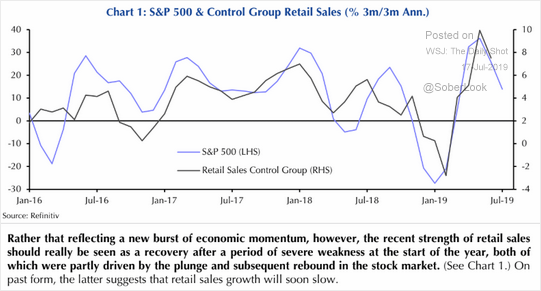

And why not? The US consumer loves a booming stock market:

Housing markets are still solid with rate cuts flowing anyway:

Advertisement

Pending home sales continued to ascend in June, marking two consecutive months of growth, according to the National Association of Realtors®. Each of the four major regions recorded a rise in contract activity, with the West experiencing the highest surge.

The Pending Home Sales Index, a forward-looking indicator based on contract signings, moved up 2.8% to 108.3 in June, up from 105.4 in May. Year-over-year contract signings jumped 1.6%, snapping a 17-month streak of annual decreases.

…All regional indices are up from May and from one year ago. The PHSI in the Northeast rose 2.7% to 94.5 in June and is now 0.9% higher than a year ago. In the Midwest, the index grew 3.3% to 103.6 in June, 1.7% greater than June 2018.

Pending home sales in the South increased 1.3% to an index of 125.7 in June, which is 1.4% higher than last June. The index in the West soared 5.4% in June to 96.8 and increased 2.5% above a year ago.

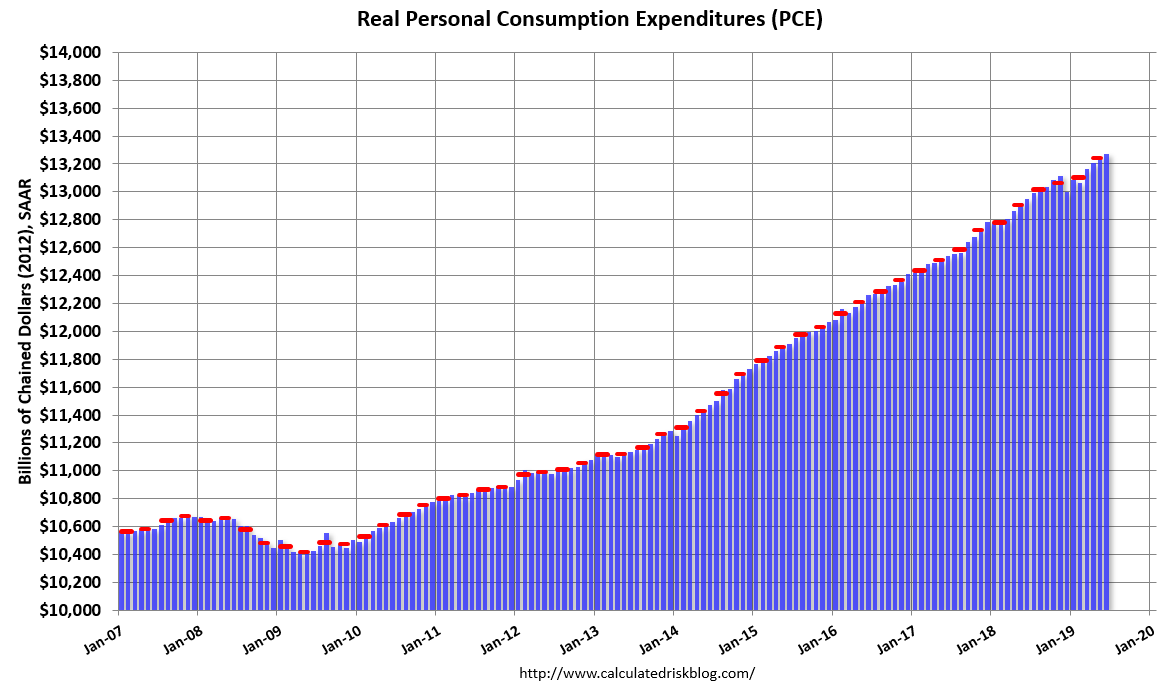

Wage growth is good and living standards rising with real income growth:

Personal income increased $83.6 billion (0.4 percent) in June according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $69.7 billion (0.4 percent) and personal consumption expenditures (PCE) increased $41.0 billion (0.3 percent).

Real DPI increased 0.3 percent in June and Real PCE increased 0.2 percent. The PCE price index increased 0.1 percent. Excluding food and energy, the PCE price index increased 0.2 percent.

It’s all pretty much the opposite of Australia and its beleaguered dollar.

Advertisement

Adding downside for the AUD was Trump trade tweets as talks resume, at Bloomie:

President Donald Trump lashed out at China for what he said is its unwillingness to buy American agricultural products and said it continues to “rip off” the U.S., just as the two nations resumed negotiations in Shanghai following a three-month breakup.

“China is doing very badly, worst year in 27 — was supposed to start buying our agricultural product now — no signs that they are doing so,” Trump said Tuesday on Twitter. “That is the problem with China, they just don’t come through.”

Departing the White House later for Jamestown, Virginia, Trump told reporters “we’re either going to make a great deal or we’re not going to make a deal at all.”

There’s just no upside and plenty of down for the AUD given:

US outperformance and a slow moving Fed;

European recession and aggressive ECB by necessity;

troubled China on trade war and Hong Kong plus falling bulk commodities ahead;

weak Australia on the construction bust leading to more RBA cuts and unconventional policy that has already begun.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.