DXY was up last night but so was EUR and CNY:

The Australian dollar was slammed again versus DMs:

And EMs:

Gold took a hit:

Oil was stable:

Metals are all over the joint:

Miner were hit again:

EM stocks broke:

Junk was fine:

Treasuries were belted:

Bunds sold:

Aussie bonds boomed:

Stocks wilted:

Westpac has the wrap:

Event Wrap

US durable goods orders and shipments topped estimates after several disappointing months. Headline durable goods orders rose 2.0% (est 0.7%), the detail was encouraging too; non-defence capital goods shipments ex-aircraft rose 1.9% (est 0.2%) while shipments advanced 0.6%. The durable goods data are notoriously volatile but this month’s update is reassuring given the downturn in global manufacturing and ongoing trade risks.

The advance US goods trade deficit narrowed less than expected in June to $74.2bn from $75bn while wholesale and retail inventories rose less than expected, prompting downward revisions to Q2 GDP expectations (due Friday) despite the strong durable goods orders. The popular Atlanta Fed GDP Nowcast for Q2 fell to 1.3% annualised from 1.6%. US jobless claims held in the low-200ks for yet another week (216k) signaling ongoing robust labour market conditions.

Germany’s IFO survey for July reflected the downside misses seen in both ZEW and Flash PMI’s. The headline Business Climate figure fell to 95.7 (est. 97.2, prior 97.5) and the expectations component fell to 92.2 (est. 94.0. prior 94.0), the latter being the lowest level since 2009.

Event Outlook

US: We expect GDP growth to slow from 3.1% in Q1 to 1.6% in Q2 (Market forecast average: 1.8%). The Q1 result was boosted by a buildup of inventories. Come Q2, this situation looks set to reverse. Outside of inventories, domestic demand is set to strengthen, thanks to a near doubling of consumption growth, and as government spending continues to provide support. Business investment should also grow, but likely at a softer pace than in Q1.

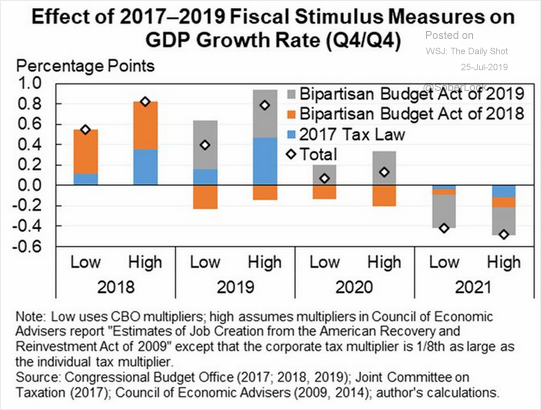

US data was OK and signals an ongoing if fading expansion. The key is it still has fiscal support:

You can expect another bipartisan Budget Act before we hit that 2021 cliff.

That said, it needs it. the global manufacturing recession is blowing in, via the ECRI:

The manufacturing PMIs have become the holy grail of indicators for many market participants. ECRI’s U.S. Leading Index of Manufacturing PMIs (USLIMPMI) anticipates cyclical shifts in the ISM and Markit manufacturing PMIs for the U.S.

The USLIMPMI, which typically leads cyclical turns in both PMIs by a couple quarters, turned down in early 2017 (chart, upper panel), and the PMIs followed suit in 2018 (lower panel). With the USLIMPMI falling back towards February’s decade low in May, it was clear that PMIs would remain in cyclical downturns, which has held true, as the ISM PMI slipped to a 2 2/3-year low in June and the Markit PMI fell to a nearly-ten-year low in July.

The USLIMPMI is one of a few ECRI leading indexes that anticipate cyclical turns in PMIs. Indeed, as we highlighted in early 2018, “ECRI’s long leading indexes have statistically significant leads over composite PMIs for the G7 economies.” Meanwhile, the early-2017 downturn in ECRI’s Global Leading Manufacturing Index growth anticipated the late-2017 cyclical downturns in both global industrial growth and the global PMI, even though the global PMI failed to predict the downturn in global industrial growth.Looking ahead, the USLIMPMI is an important tool for anticipating directional changes in the PMIs, which will continue to shape market perceptions about the economy. The latest USLIMPMI update, released to our clients last month, already clarifies the PMI outlook.

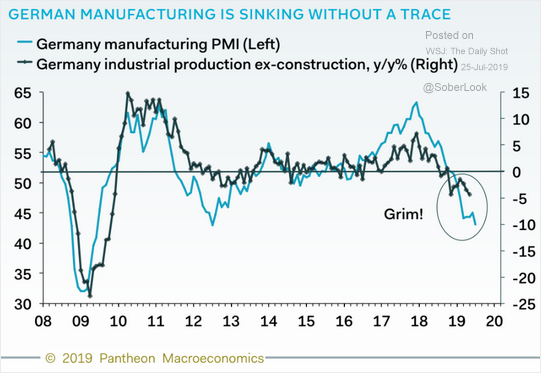

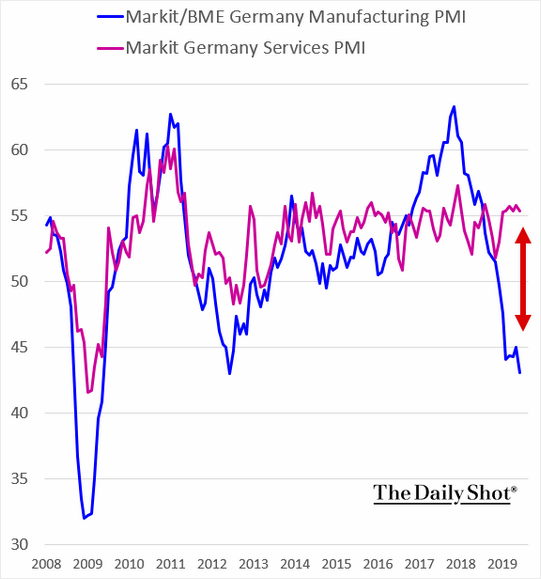

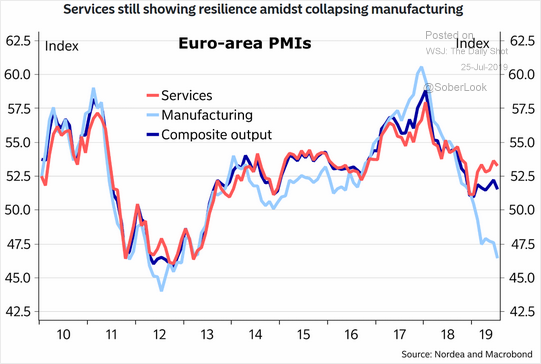

The issue for forex, though, remains that China and Europe are worse. The latter is crashing into recession:

Led by China:

Services have held up:

But not for much longer:

Especially as Brexit headwinds intensify. I expected the ECB to dovish and it was:

At today’s meeting the Governing Council of the European Central Bank (ECB) decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to its aim over the medium term.

The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The Governing Council also underlined the need for a highly accommodative stance of monetary policy for a prolonged period of time, as inflation rates, both realised and projected, have been persistently below levels that are in line with its aim. Accordingly, if the medium-term inflation outlook continues to fall short of its aim, the Governing Council is determined to act, in line with its commitment to symmetry in the inflation aim. It therefore stands ready to adjust all of its instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner.

In this context, the Governing Council has tasked the relevant Eurosystem Committees with examining options, including ways to reinforce its forward guidance on policy rates, mitigating measures, such as the design of a tiered system for reserve remuneration, and options for the size and composition of potential new net asset purchases.

Mario Draghi set up Christine Lagard’s bazooka:

“This outlook is getting worse and worse,” Draghi said in Frankfurt on Thursday after a meeting of the ECB’s Governing Council. “It’s getting worse and worse in manufacturing, especially, and it’s getting worse and worse in those countries where manufacturing is very important.”

“Markets will keep speculating about the composition of the stimuli, and were somewhat disappointed with the lack of details,” said Piet Christiansen, an economist at Danske Bank, which is expecting 20 basis points of rate cuts and more QE. “Still, it’s a matter of when and how ECB will act, no longer if.”

That doubt meant that the EUR ended up flat on the night despite the very dovish rhetoric.

Yet that was still not enough to save the Australian dollar which ended the night close to the lows. We can see this as, in part, the result of fading growth prospects and falling equities. But the weakness was so pointed that I wonder as well if the RBA has not finally started to have an impact with its increasingly dovish shift. It did move towards unconventional policy yesterday with something of a “whatever it takes” moment when it adopted forward guidance rhetoric around rates being low for a long time to come.

The fact is, the downdraft for the Aussie is pretty good again: Chinese growth weak, bulk commodities rolling over, ECB easing, RBA still cutting as Recessionberg refuses fiscal, global growth fading and US relative out-performance.