The Australian dollar piled it on across the board after decent Chinese credit:

Gold lifted:

Advertisement

Oil eased:

Metals were firm:

Big miners were soft:

Advertisement

EM stocks are struggling:

The junk rally is under pressure:

As Treasury yields shunt higher:

Advertisement

Bunds too:

And Aussie bonds:

Yet stocks flew anyway!

Advertisement

Apparently all news is good news now for equities, including rising bond yields!

The big question now for the Australian dollar is what kind of bond curve steepening are we seeing? Is a bull steepener in which reflation takes hold and profits rise, driving up risk assets like the Australian dollar? Or is it a bear steepener in which inflation arrives with stagflation to destroy profits in which case the Australian dollar will struggle? Or is it a head fake which returns to a flattening curve forthwith, hurting the Australian dollar? Let’s refer to Damien Boey at Credit Suisse:

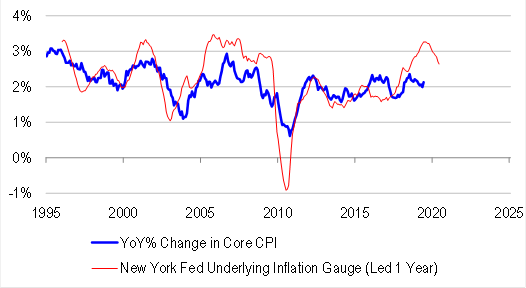

US core CPI came in above expectations, rising by 0.3% in June. This took year-ended core inflation higher to 2.1% from 2%. Compositionally, there were a number of factors boosting core CPI inflation, with rental inflation printing quite robustly despite deterioration in several housing indicators.

The acceleration in core CPI inflation, and the bond market sell off underscore the fact that the inflation debate, especially when it comes to the fallout from trade disputes, is very much alive. Never mind whether one is an “inflationista” or “deflationista” – the point is that there is uncertainty and debate at present. In contrast, the bond market is pricing in inflation as if there is no debate, and that disinflationary, or even deflationary scenarios are worth paying up for.

The New York Fed underlying inflation gauge has historically been a powerful leading indicator of the cycle in core CPI inflation, and has been pointing to higher, rather than lower inflation in 2020. To be sure, the gauge has come off its highs – but it is still at levels consistent with accelerating inflation. We note that some of the components of the New York Fed gauge, such as wage inflation are still printing quite robustly, reflecting diminished spare capacity in the economy. And then there is the dramatic trend slowdown in productivity growth to consider … Paying people more to do not much more is not a great recipe for low inflation.

When it comes to trade disputes, the familiar debate surrounds the deflationary effects of reduced USD supply (from trade) on emerging markets dependent on USD funding, versus the inflationary effects of supply chain disruption. Of late, it seems that investors have injected a third factor into the equation – reduced corporate pricing power from slowing demand growth. Therefore, the market has come to the view that even in the presence of supply chain disruption, multi-national corporates will be unable to pass on higher costs to end consumers, and that trade disruption will be bad for both inflation and profit margins. The trouble with this view is that it involves some extremely negative assumptions building upon each other, and probably understates the degree of inflation risk coming from supply chain disruption. Indeed, the deflationary effects of reduced USD liquidity were the predominant concern for asset allocators in 2018, and from the lower starting point, it is not surprising to see focus return to inflationary scenarios.

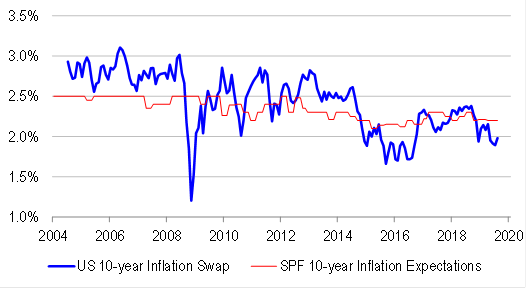

Over a 10-year horizon (a very long period of time allowing us to abstract from cyclical factors like demand and pricing power), economists forecast US CPI inflation of 2.25%. They have pretty much stuck to a 2-2.5% forecasting range since the beginning of interest rate and inflation targeting by the Fed in the early 1990s. But the bond market is only discounting less than 2% inflation over the same horizon. In other words, unless we expect economists to revise down their numbers to meet the market (which they have never done since 1990), the inflation risk premium in bonds is negative. In other words, investors are saying that there is negative compensation for getting their long-term inflation forecast wrong. Yet there is debate about the inflation outlook. Therefore, it is reasonable to infer that inflation risk is not properly priced. And it is possible to position for this using relatively cheap inflation hedges such as commodities.

In response to the upside surprise in the June CPI data, as well as a poor 30-year auction, US 10-year bond yields spiked higher by around 8bps. Australian 10-year bond yields are up around 11bps on the day at time of writing. Yield curves everywhere are starting to steepen, even before we have seen rate cuts from the Fed or ECB. Indeed, the US 3-month/10-year yield curve is on the precipice of entering into positive territory. This sort of curve steepening, if sustained, should support value investing within the equity market, as reflation starts to get priced in, and investors stop worrying about hard landing, de-leveraging risks which traditionally undermine confidence in mean reversion. It should also be marginally negative for quality and bond proxy exposures. Yet in the past few days of curve steepening, we have not seen value bounce back materially, even as defensives have given up some alpha relative to cyclicals.

Advertisement

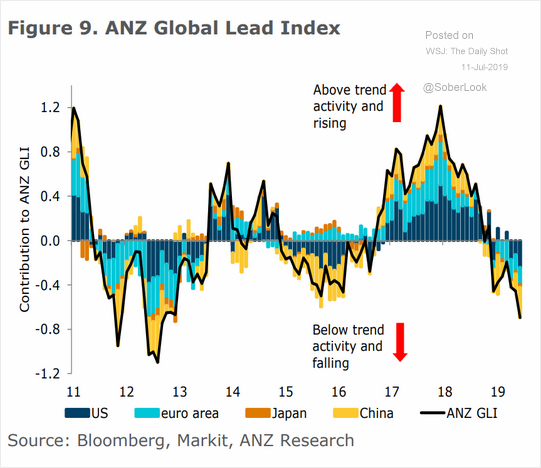

For mine that is because the market still knows in its bones that this is a head fake. The blip in US inflation will pass. If it is trade war related then it is a pig in the python and can be looked through. If it is more fundamental than it is a late cycle outlier. Wage inflation is already easing as US growth slows via the fiscal cliff, stalling oil patch and trade blow back. Global growth is slowing even faster. Chinese stimulus is moderate at best and no more than an offset for trade weakness. European stimulus is modest and likewise offset by trade impacts. Check out the global leading indicators from ANZ:

The main factor thing that can turn this around is Trump taking his boot off China’s throat. That still seems unlikely, not least because leaving it in place will aid his 2020 re-election, notwithstanding pain in certain rust belt seats.

Until then, the Aussie dollar cannot get far to the upside and remains at risk to the downside.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.