Major forex was stable last night with Wall St closed for July 4:

The Australian dollar was generally soft:

Gold fell:

Oil too:

And metals:

Miners were weak in London:

EM stocks too:

Junk is still strong:

Bunds too:

And Aussie bonds:

European stocks lifted:

Westpac has the wrap:

Event Wrap

Eurozone May retail sales disappointed (-0.3%m/m, est. +0.3%m/m but prior revised to -0.1%m/m from -0.4%m/m). The weak points were in clothing/apparel, good and notably fuel (-1.3%m/m). Although weak and concerning over the state of regional consumers, the weather in May was poor and might have weighed especially on clothing.

Event Outlook

Germany: May factory orders are expected to edge down 0.2% in the month with the annual pace of decline hitting 6.2%yr.

US: Jun nonfarm payrolls are anticipated to bounce back after a soft read in May (+75k in the month and the previous level revised down by 75k). Consensus for Jun is for a 160k increase in employment with the unemployment rate holding at 3.6%. The trend lower in average hourly earnings is seen to stabilise, edging up to 3.2%yr from 3.1%yr in May.

Here are some fun facts on global yields via Bloomie:

- Year-to-date EGBs returns led by Greece (23%), Spain (10%), Portugal (9.8%) and Belgium (8.8%)

- Around 25% of global debt now has a negative yield, amounting to a record high of $13.4 trillion

- The entire core and semi-core European government bond spectrum out to 10-year is trading in negative yielding territory

- Around 85% of the German government curve trades below 0%

- Around 55% of Spanish government debt has a negative yield (with selective carry the place to be this year, see more here and here)

- Italian front-end goes negative as BTPs turbo-charged sending 10Y lower by ~50bps in the five days through Wednesday, the largest such move since June 2018

- Around 75% of Japanese government debt trades below 0%, highlighting the importance of yield-thirsty flow from Japan into the global bond markets (see examples of analysis here and here on this theme)

- Around 80% of the active covered bonds of Germany and France, 83% of Spain and 57% of Denmark have negative yields

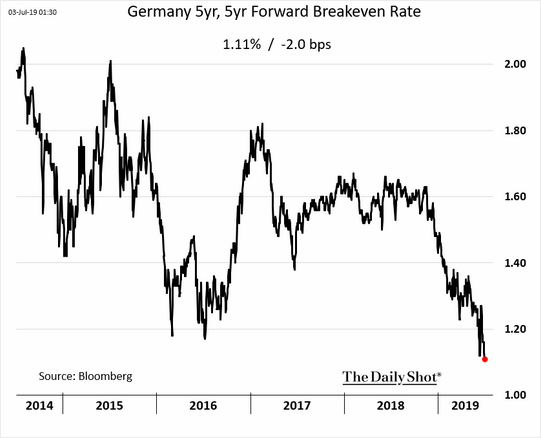

- EUR 5y5y inflation swap has given back nearly all of the post-Sintra spike; the ECB needs to restore some inflation credibility, which should be the trigger for 10Y Bund yield to move back toward 0%, helped by positioning being built at yield lows

Here is the collapse in European inflation expectations:

Michael Every at Rabobank sums it all up nicely:

It’s 4 July – and, yes, there are fireworks.

Firstly, US equity markets are at a new record high. Up, up, and up they go into the firmament. At the same time, US bond yields go down, down, and down. In fact, the entire US curve is now inverted, standing below the level of Fed Funds. As such, the Fed MUST act this month, surely. In which case, hooray, stocks can keep going up, up, and up! Indeed, “We’ll get to 30,000 on the Dow if we pass USMCA, we cut interest rates and we move forward with the Trump-growth agenda,” said Trump economic advisor and China hawk Navarro in an interview with Bloomberg Television.

But Houston, we have a problem. Not only is there no point in spending good money on “Dow 27,000!”, “Dow 28,000!”, and “Dow 29,000!” baseball caps if so, missing out on lots of potential production, but WHY are the Fed cutting rates? Does that reason presage something good for corporate earnings vs. multiple extensions and cheaper buybacks? How many times in recent decades have we seen the bond market and the stock market sending these duelling signals? And how many times have stocks been right relative to bonds, with a lag?

But we had more coloured gunpowder to gaze up at in awe. US President Trump warmed up for the big party today by tweeting: “China and Europe playing big currency manipulation game and pumping money into their system in order to compete with USA. We should MATCH, or continue being the dummies who sit back and politely watch as other countries continue to play their games – as they have for many years!”

That’s as open an attempt to jaw-bone the USD lower as one will ever see – and perhaps a threat to do more than jawbone. Yet Houston, we have a dollar problem. The Fed is about to cut rates, showing they don’t know what they are doing. The US fiscal deficit is enormous and growing. The US is insulting trade partners around the world, apparently threatening a boycott of US Treasuries. The president is both publicly belittling the Fed more than I do, openly introducing doves to its board, and speaks of open currency manipulation. There is open chatter of de-dollarization even the mainstream financial media.

AND YET THE DOLLAR IS NOT SLUMPING

Yes, it is off its recent highs vs. AUD, CNH, etc.; yes, some EM have seen some recovery too; and, yes, JPY continues to grind higher. But when you look at the staggering blows the USD is taking, and see that it only takes a half-step back, stop and think what the potential surprise upside movement is should the next phase of the global fireworks kick in.

For example, now that Iran has officially announced that from Sunday it will begin enriching uranium to any level it sees fit above the agreed limits set in the 2015 nuclear deal: in response Trump has replied: “Be careful with the threats, Iran. They can come back to bite you like nobody has been bitten before.” The only way to interpret that as ‘risk on’: is to (1) believe Trump is bluffing again; (2) believe the Iranians are bluffing; or (3) believe that central banks will just cut rates more anyway so regardless of what happens it’s all good.

Actually, rumours are flying round that there are more biting US sanctions in the work targeting the Iranian Supreme Leader’s own businesses. If so, we continue to raise the stakes in this dangerous poker game without either side calling. However, while that game is being played, global observers won’t want to be leaving too many USD on the table…which is one of the reasons the greenback just won’t go down.

Of course, it’s more than Houston who has a problem. Europe is seeing the equivalent of a box of cheap indoor fireworks unleashed to celebrate the arrival of a new ECB president. Markets are so enthusiastic about the growth outlook under Lagarde that they are happy to lose 78bp to lend money to Germany for 2 years and nearly 40bp to lend to it for 10 years. Then again, they will also now lend to Italy–who does not control its own currency and is run by increasingly-popular populists–for 10 years at 1.58%, nearly 40bp lower than they will lend to the US. You don’t like that deal? How about lending to Austria for 100 years at around 1%? The same Austria who 100 years ago was just emerging from the wreckage of the Austro-Hungarian Empire and WW1, underlining how much can happen in a century. And against that backdrop European stocks still aren’t at record highs yet. Is that an opportunity or a threat?

Meanwhile in China overnight SHIBOR is now down to 0.88%, lower than during what was a kind-of-but-officially-not Chinese recession in 2015. So no shortage of liquidity at big banks – but not so much for smaller banks or the private firms and SMEs who continue to struggle for credit. That’s as both official and Caixin PMIs sit below 50 for manufacturing, indicating the pressures being felt across the economy above and beyond the trade war.

Sorry, but when one looks at what looks like a fresh global easing cycle from already ridiculously low levels of rates, and trade wars underway, and open calls to FX wars too, and fears of hot wars in several places, one really has to rain on this particular 4 July parade.

How far can DXY fall when European inflation is so much lower and falling? This is an insurance policy against any large gains in the AUD even as the Fed cuts.