The return of the bond boom is an interesting phenomenon for forex. Normally, as rate cuts begin, we would see a sharp steepening in the yield curve as the short end falls with the cash rate and long end rises with better inflation prospects. A reflation rotation in other words.

Advertisement

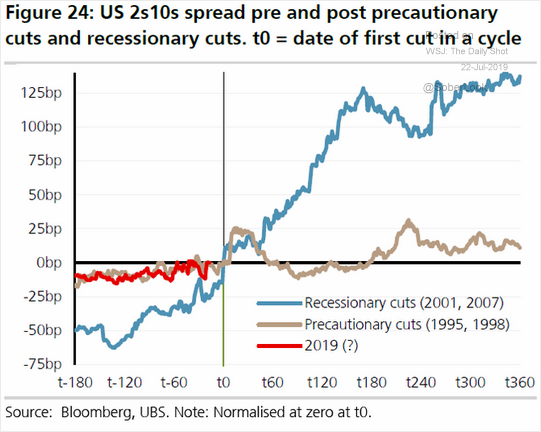

Yet that is not always the case. There are times when the curve steepening is muted or does not happen at all. One of those is insurance rate cuts, such as those currently underway in the US:

That may mean that until we get some more potent shock to knock US growth lower, Europe will continue to lead global yields lower and spreads to the US will govern the USD/EUR as the ECB moves aggressively:

Advertisement

Moreover, in Australia’s case, we are entering secular stagnation proper for the first time as household debt hits unsustainable highs and the mass immigration economy imports a deflation tsunami into the labour market. Even as the central bank sets itself the impossible task of reflating it. Westpac has more:

Advertisement

In his weekly missive, Westpac Chief Economist Bill Evans noted that while the July RBA Board Minutes imply a pause in its easing cycle at its August meeting, the vulnerability of the RBA’s unemployment forecast for 2020 (to be updated in the August SoMP) implies that every meeting after August will be “live” and the RBA may not wait until November (Westpac’s forecast) to deliver another 25bp cut.

While we see 0.75% as the low in the cash rate, the risks are to the downside. So the issue remains one of what is the realistic lower bound for the cash rate? That question has been at the forefront of market thinking for some time and can be seen in the response to the two rate cuts delivered so far. That is, there has been little re-pricing of the terminal rate or the timing of the final cut, the dialogue around possible QE approaches has not diminished and scepticism around the ability of monetary policy to reach its goals has remained high.

The RBA sees the two major channels of stimulus coming through a lift in disposable income for borrowers and the currency. There has yet to be a clear response on those fronts, and while the first two cuts in this cycle have been quite effective with an average of 45 basis points of pass through, the effectiveness of the next cut will be an important indicator of likely future moves. Until then we would not expect a significant shift in valuations across the term structure.

Near term, however, the RBA Governor is delivering a speech on Thursday entitled “Inflation Targeting and Economic Welfare”. That should provide some timely nuance to current pricing and understanding of the RBA’s tactics and triggers.

Given current RBA pricing, UST price action will be key to domestic directional impetus. The two charts at right show the 2019 price action in 3yr and 10yr bond futures prices. After the significant rally over the first half of the year, the upside momentum appears to have slowed, with prices having moved largely sideways over the past month. That is not particularly surprising given that the initial rally was sustained by a re-pricing of the RBA outlook which has now been largely delivered and short end pricing is now relatively stable at one more rate cut factored-into the forward profile. With that as an anchor, it suggests that near term price action will largely depend on US 10yr bond yield directionality, especially considering the near record correlation between the two that we explored last week. While our front page essay focused on the possible response to Fed policy actions, the chart at left shows the relationship between 10yr yields and 10yr BEI in the US. As can be seen, in recent days the inflation expectations component of the nominal yield has turned up slightly. Should that sustain then US 10yr yields will test the upper end of their recent range. That implies some downside for AU bonds, however we remain better buyers on dips to the bottom of the recent bond futures ranges (3s 99.00; 10s 98.55).

As mentioned on the previous page, the US 10yr BEI has recently turned higher, from the lowest levels since 2016. However, as the chart at left indicates, AU 10yr BEIs are at their lowest levels in more than 10 years, indeed ever. In addition, the BEI term structure (not shown) has been flattening, as short end BEIs have remained unchanged since the Q1 CPI release in April. An environment of a flattening BEI term structure as inflation expectations fall is historically very unusual. It is far more normal for the front end BEIs to drive the term structure, leading it to flatten in times of recovery and steepen in periods of low inflation. Given that we have already had 2 RBA rate cuts, that is even more unusual. So what is driving this? Clearly there has been a change in perceptions regarding the RBA’s ability to get inflation back into its 2-3% target band. The long end has effectively repriced long term average inflation structurally lower. So it is timely, ahead of next week’s Q2 CPI release that RBA Governor Lowe is focusing on the inflation targeting regime in his speech on Thursday. This reduction in medium term inflation expectations goes some way to explaining why the AU 3-10yr curve flattened while rate cuts were being factored-in (chart at right) and unless the CPI surprises significantly to the upside next week, it suggest little risk of a sustained curve steepening anytime soon.

In short, deeply atypical and ahistorical deflationary trends are keeping pressure on the Australian dollar and it likely won’t change until something very large, somewhere, breaks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.