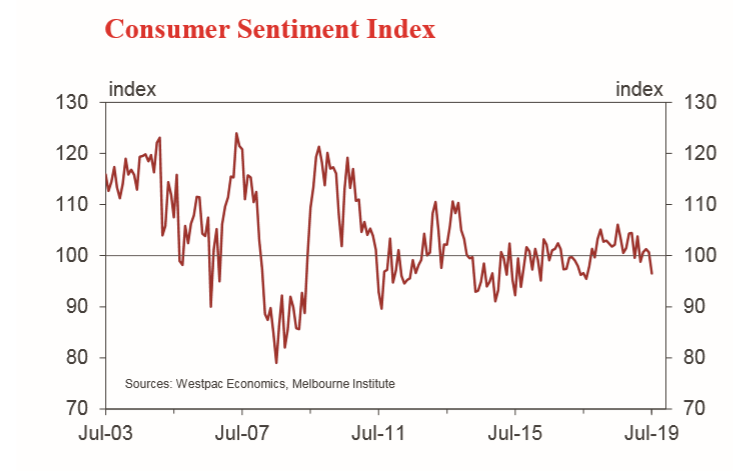

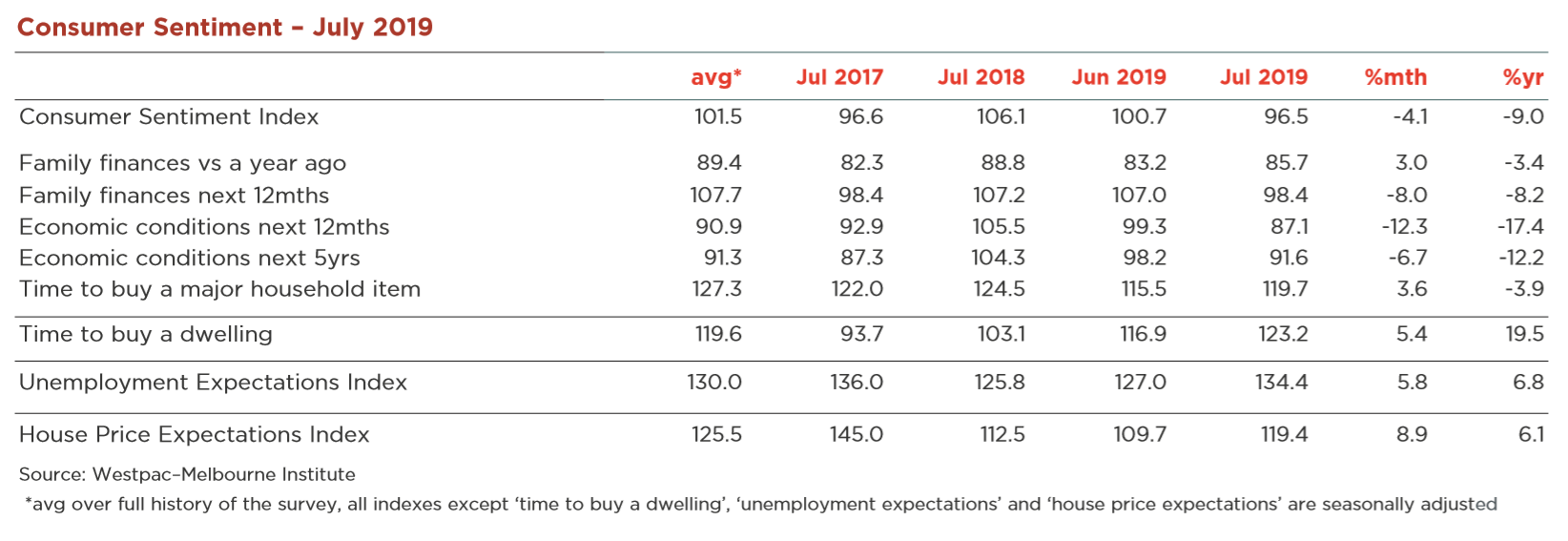

The Westpac-Melbourne Institute Index of Consumer Sentiment fell 4.1% to 96.5 in July from 100.7 in June.

The fall in sentiment this month is troubling as it comes against what should have been a supportive backdrop for confidence. The last month has seen a further 25bp interest rate cut from the RBA, the Federal government’s tax package pass through Parliament, more signs that the Sydney and Melbourne housing markets are stabilising and even some more improvement in the US-China trade dispute. Despite these positives, Australian consumer confidence has fallen to a two year low.

The main driver continues to be deepening concerns about the outlook for the Australian economy and prospects for family finances. The index components show the biggest decline in the sub-index tracking expectations for the ‘economy, next 12 months’ which slumped 12.3% to be down 16.4% since May to its lowest level in four years. Longer term expectations for the economy were also pared back sharply, the ‘economy, next 5 years’ sub-index falling 6.7%.

Deteriorating expectations for the economy outweighed any near term support from the prospect of lower interest rates and tax relief. The sub-index tracking consumers’ expectations for ‘finances, next 12 months’ also recorded a sharp 8% fall, moving back into net pessimistic territory for the first time since late 2017.

Consumer views around current conditions were better supported. The ‘finances vs a year ago’ sub-index lifted 3% to a five month high, although at 85.7, the sub-index remains at weak levels overall. Consumer attitudes towards spending also improved, the ‘time to buy a major household item’ sub-index rising 3.6% to the highest level since late last year. This will be of some relief given that consumer views around current conditions tend to be a better guide to current spending activity. However, that support could fade quickly if weaker expectations for near term prospects are realised.

Responses over the survey week show the Reserve Bank’s rate cut on July 2 had little or no impact on sentiment. Note that the bulk of the survey was completed prior to the government’s tax package passing into legislation on July 4, although this had been widely foreshadowed by media coverage earlier in the week. Indeed, the muted sentiment response to both interest rate cuts and tax relief may stem from the fact that both developments were widely anticipated. Notably, the sub-group detail showed no boost to sentiment amongst groups that stand to benefit most from policy easing: sentiment amongst mortgage holders declined 3.3% in the month and sentiment amongst middle income earners was down 5.5%.

Other aspects of the sub-group detail point to some notable ‘sub-plots’. The initial impact of the surprise Federal election result in May looks to be fading with sentiment amongst “Coalition voters retracing over three quarters of the 7.5% jump in June. Sentiment also recorded a big 14% drop in regional NSW where drought conditions have intensified markedly in recent months. Sentiment amongst those with a trade qualification was also down a sharper 7.6% suggesting the residential construction downturn may be starting to weigh more heavily on some households.

Increasing concern about the economy is undermining consumers’ sense of job security. Confidence in the labour market continued to deteriorate sharply in July. The Westpac-Melbourne Institute Unemployment Expectations Index recorded a 5.8% rise, following on from a similar rise last month and taking the index materially above its long run average for the first time since mid-2017 (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). Expectations have shown a more marked deterioration in NSW, Vic and WA.

Housing-related sentiment continues to show a clearer positive response to lower interest rates with assessments of both ‘time to buy’ and house price expectations recording strong increases in July.

The ‘time to buy a dwelling’ index rose 5.4% 123.2, the first above trend reading in four and a half years. The index is up 19.5% on the same time last year. The biggest turnaround continues to come in Sydney and Melbourne where substantial price corrections have also improved affordability over the last two years.

The Westpac-Melbourne Institute Index of House Price Expectations Index posted another robust 8.9% increase following last month’s spectacular 22.7% gain. At 119.4, the Index is now at its highest level since May last year but still below the long run average read of 125. All states have recorded sharp rises over the last two months and net positive reads comfortably over the 100 mark. Just over 40% of consumers expect prices to be higher in a year’s time – that compares to less than 20% back in March.

The Reserve Bank Board next meets on August 6. We expect the Bank to leave the cash rate on hold at this particular meeting but see further easing coming later in the year. Having delivered back to back 25bp cuts in June and July, the Reserve Bank has signalled that it is prepared to ease further “if needed”. Updated forecasts released in the August Statement on Monetary Policy, due August 8, will give the best guide to how the RBA sees the case for further policy action. At this stage it seems likely that the Bank will make only minor changes to its growth and inflation forecasts, suggesting policy will be unchanged at the August meeting.

However, policy is set to be in play at every Board meeting between now and the end of the year. Westpac continues to expect a further 25bp rate cut, most likely coinciding with a downgrade to the Bank’s growth and inflation forecasts in November. The specific timing of this next move remains highly uncertain – labour market developments could easily shift it around and there are other factors at play, both overseas and domestically. The Bank will also be monitoring policy sensitive sectors such as housing and the consumer closely to gauge the impact of its easing to date. On that count, updates on consumer sentiment clearly show interest rate moves have shored up confidence in the housing market but have not prevented a wider deterioration in sentiment.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.