The ABC’s David Chau has penned a good summary of the likely impacts from APRA’s reduction in its interest rate buffer to 2.5%, which was announced on Friday:

Effective immediately, banks no longer need to apply a “stress test” to see whether their customers can afford, at least, a 7 per cent interest rate on their residential home loan repayments…

The only restriction is that the banks ensure borrowers can repay their loans if interest rates were at least 2.5 percentage points higher than they are currently.

With many banks now offering variable mortgage rates in the low-3s, that means many borrowers are likely to be tested at a rate below 6 per cent per annum as banks decide whether they can afford to repay their loan…

These record low rates mean APRA’s rule changes will allow people to borrow a lot more.

A family, earning an household income of $109,688, would be able to borrow up to $60,000 more, if their loan was assessed at 6.25 per cent instead of 7.25 per cent, according to financial comparison website RateCity.

Its analysis suggested that a single person, in the same scenario, may be able to borrow an extra $50,000.

“Many Australians may suddenly find they can get their home loan approved,” RateCity research director Sally Tindall said…

“APRA has eased off the brakes slightly, but that doesn’t mean it will be a complete field day for borrowers.

“There are still a number of checks and balances in place to make sure people aren’t jumping into home loans they can’t afford to repay”…

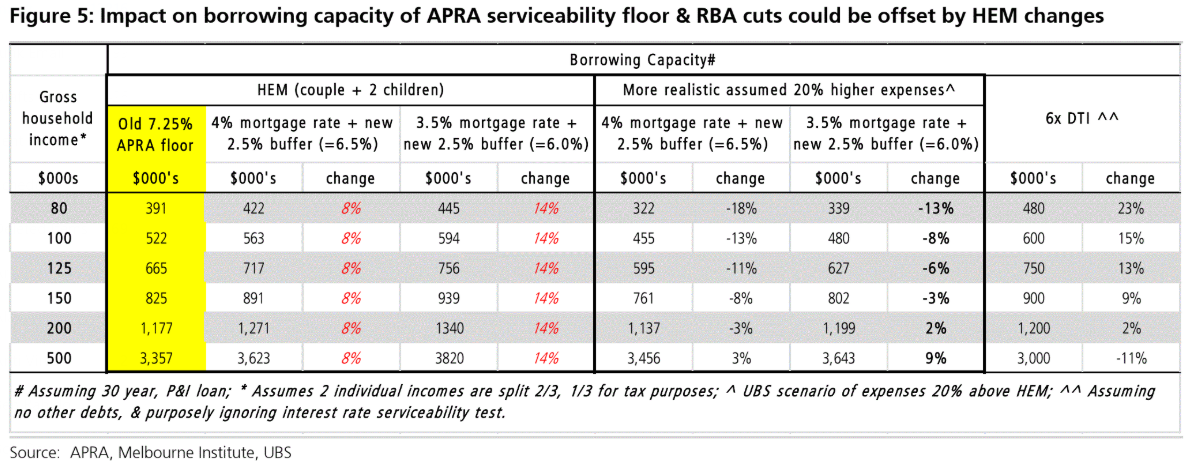

Investment bank UBS forecast that prospective buyers might be able to borrow up to 14 per cent more due to the RBA rate cuts and APRA’s loosening of lending restrictions.

“However, these changes need to be considered in the context of ongoing tightening, in particular a new HEM [Household Expenditure Measure] methodology, the rollout of comprehensive credit reporting and open banking,” UBS banking analyst Jonathan Mott wrote in a note last month.

That’s right. While the changes to APRA’s interest rate buffer are unambiguously bullish for both mortgages and house prices, they are likely to be somewhat offset by tightening of the Household Expenditure Measure (HEM) – a relative poverty measure – in the wake of the banking royal commission.

According to Endeavour Equities, using the HEM to measure borrower expenses “upwardly biased Debt Service to Income ratios by 10-15%”, and “the size of the credit crunch is directly proportional to the unreasonableness of the HEM expenses benchmark”.

A modified HEM will soon come into effect that will more accurately match expenditure benchmarks with income. According to UBS, this will constrain credit availability going forward and could offset much of the stimulus coming down the pipe:

Looking further ahead, the outcome of Westpac versus ASIC case is going to have a direct bearing on the legality of the benchmarks. So too will the outcome of private class actions, such as Maurice Blackburn alleging that Westpac was overly-reliant on the HEM benchmark when assessing mortgage loan applicants.

If Westpac loses these cases, then ADIs may be forced to abandon the HEM altogether and rigorously scrutinise a borrowers’ capacity, with the end result being even tighter credit availability.

While the outcome of these cases is up in the air, it is unlikely there will be a new credit explosion. Rather, we are likely to see a gentler expansion of mortgage lending and moderate house price growth.

unconventionaleconomist@hotmail.com