Advertisement

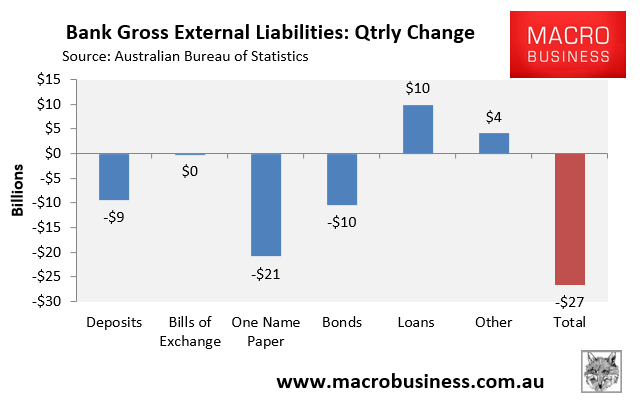

The Australian Bureau of Statistics (ABS) yesterday released its National Financial Accounts for the March quarter, which revealed a 2.9% quarterly decline in Australian banks’ gross external liabilities (offshore borrowings), and a 0.2% decrease over the year.

One Name Paper (-$21 billion), Bonds (-$10 billion) and Deposits (-$9 billion) drove the quarterly decline in offshore borrowings by the banks over the March quarter, partly offset by a $10 billion rise in loans and a $4 billion increase in Other:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement