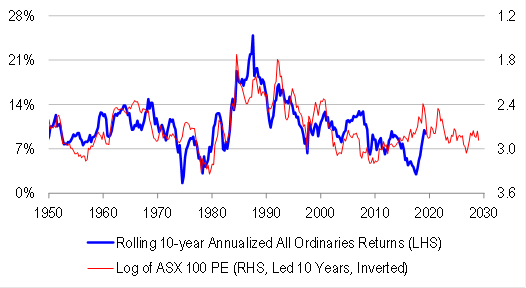

Via Damien Boey at Credit Suisse:

The RBA has just released a paper about the history of the Australian equities. It contains some very useful and unique historical data on the Australian market. For context, earnings, dividends and total returns data for the Australian market has been quite sparse, and of questionable quality going back in time. Many use the Macquarie/AGSM 50-leaders data as a benchmark prior to 1974. But of course, these data are limited by naïve weighting and narrow sample size. The new RBA database has been constructed by the analyst (Matthews) sifting through decades of newspaper data going back to the early 1900s, covering as many index constituents as possible for the ASX 100, and properly cap-weighting their metrics. It fills in much of the missing data (quality) we have for the Australian market.