By Chris Becker

Wall Street rebounded fiercely overnight on the back of the Powell Put with lower rates definitely on the agenda for the Fed in 2019. EZ inflation pulled back in May while commodity prices remained under pressure despite a much lower USD. It should be a solid risk on day here in Asia with the latest GDP print locally perhaps unsettling the rise in Aussie dollar.

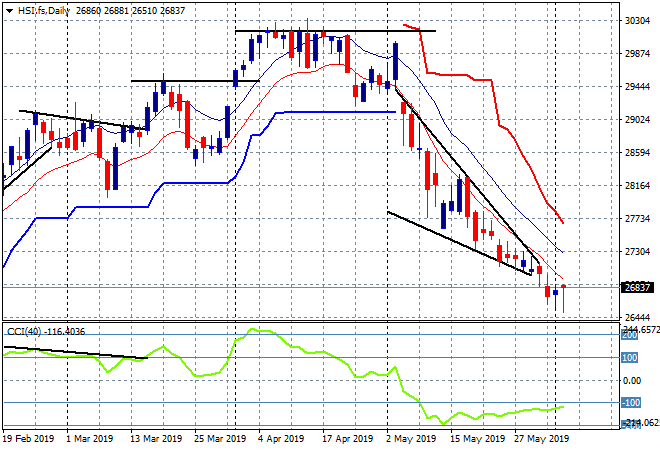

Yesterday saw Asian stock markets continue in a mixed mood with the Shanghai Composite again closing below the critical 2900 point support level, falling nearly 1% to 2862, while the Hang Seng Index was down nearly 0.5% to 26761 points, making another daily low. The daily chart had been showing a deceleration pattern with a target at the 27000 point level and despite the lower lows, price does seem anchored around here. I’m watching the daily lows here for signs of an inversion, with a growing probability of a swing higher on better sentiment: