By Chris Becker

Wall Street was all over the place last night after European markets improved following a dour start to the week here in Asia. Tech stocks dragged the NASDAQ down significantly as regulatory issues surrounded the sector, while most industrials slipped on ongoing trade concerns as Tariff Trump had tea with the Queen. The real moves were in currency markets with St Louis Federal Reserve President Bullard indicating a rate cut in 2019 was on the cards, sending the USD plummeting against the majors and gold alike. This overshadowed the slowdown in the important US ISM print with 10 year Treasuries hitting a new low for the year.

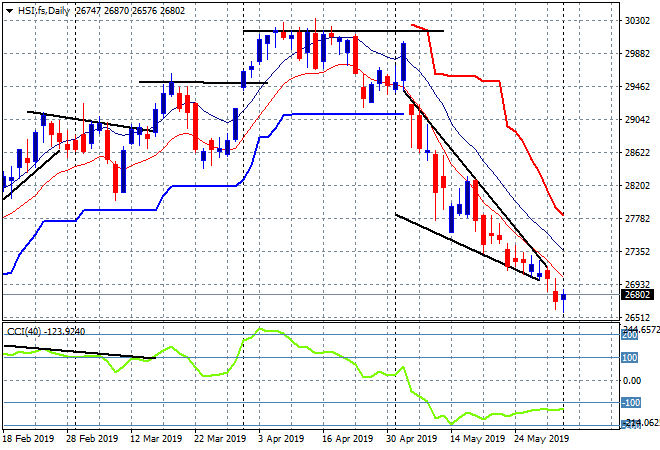

Yesterday saw Asian stock markets start the week with a decline, although the Shanghai Composite was a standout by only falling 0.3% but still closed below the critical 2900 point level. The Hang Seng Index was down by over 0.5% at one stage, but managed to close with a scratch session at 26893 points. The daily chart had been showing a deceleration pattern with a target at the 27000 point level but poor sentiment continues to weigh, slowly pushing the market below this level. I’m watching the daily lows here for signs of an inversion, with a small probability of a swing higher: