While all local eyes were on the RBA, which made its first move in interest rates in three years, the region was focused on macro issues particularly trade with all the action in bond markets as traders remain jittery. The USD is still weak after the recent reversal with the Yuan fix remaining steady, the Euro will come under pressure this evening with the latest CPI print.

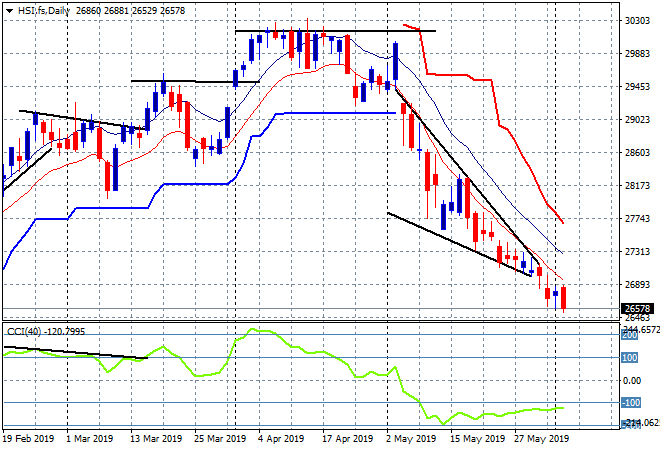

The Shanghai Composite is set to again close below the critical 2900 point support level, falling nearly 1% to 2860, while the Hang Seng Index is down nearly 0.6% to 26729 points, still unable to arrest the recent decline, making another daily low. The daily chart had been showing a deceleration pattern with a target at the 27000 point level but poor sentiment is weighing too much on this market:

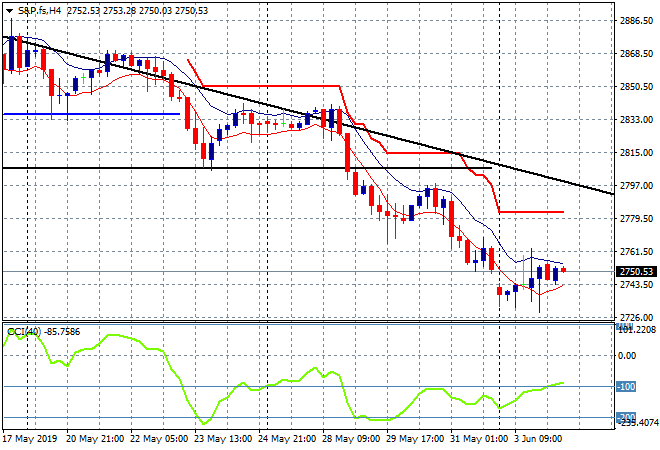

S&P and Eurostoxx futures are down 0.4% or so going into the European session with the four hourly chart of the S&P500 chart suggesting a possible short term bottom here at the 2750 point level, but still remaining well below key terminal support at 2800 points. This level continues to signal a major correction as the completion of a very bearish head and shoulders pattern on the longer term charts and would require a rally well above the downtrend line:

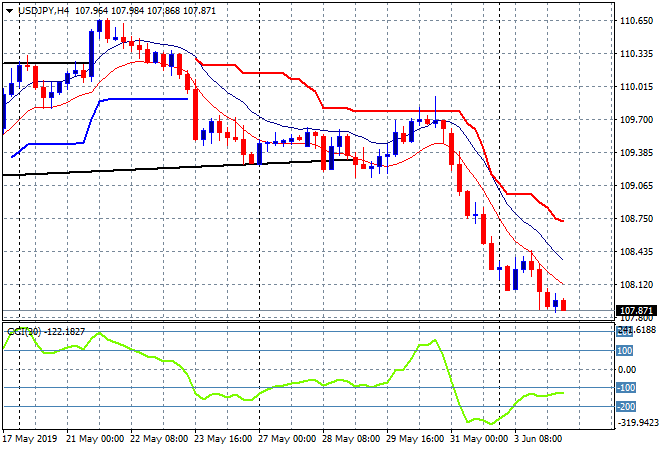

Japanese share markets are holding on the best, with the Nikkei 225 putting in a scratch session to finish at 20408 points, almost ready to tackle the key terminal and psychological support level at 20000. There seems to be no bottom in the USJDPY pair with a fall below the 108 handle during today’s session, as risk-off avoidance and the shifting of USD strength is sending Mrs Watanabe to the domestic safe haven currency:

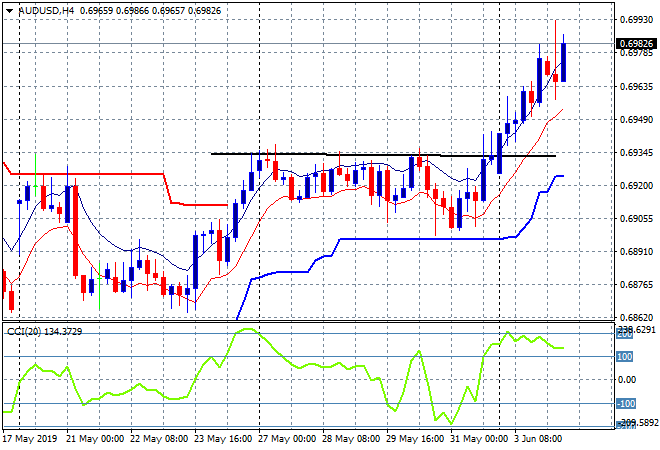

Australian stocks did the best in the region by advancing slightly, helped along by bank stocks that rallied in the wake of the RBA cut. The ASX200 eventually closed nearly 0.2% higher at 6332 points, still below previous support at 6400 points but holding on in this small dip. The Australian dollar reacted somewhat to the upside on the cut news, almost pushing through the 70 handle before retracing, but has again lifted going into the London session where momentum remains overbought:

The economic calendar ramps up again tonight with two events to keep an eye on, first its the EZ wide CPI print for May, then Fed chief Powell will be talking at a conference and may respond to Bullard’s comments from last night.