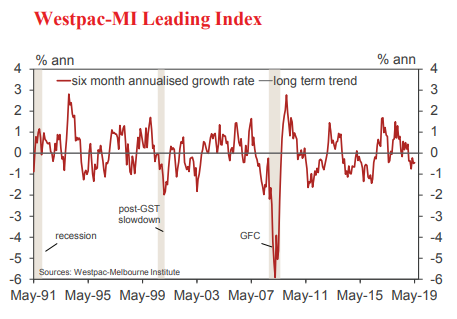

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose slightly from –0.49% in April to –0.45% in May. Expectations index (–0.15ppts).

The Index growth rate has been consistently negative over the last six months, a clear signal that economic growth is likely to be remain below trend through the rest of 2019. Figures released earlier this month showed the slowdown over the second half of 2018 extended into the first quarter of 2019 with annual GDP growth slipping to 1.8%yr, well below ‘trend’ of 2.75%yr and the slowest pace since the GFC a decade ago.

The Leading Index picked the slowdown well with a sharp deceleration in the Index growth rate beginning in the second quarter of last year, then swinging into negative late in the year, a reading consistent with the sub-trend annual growth now being reported. The May reading shows little change since then and points to this sub-trend pace continuing well into the second half of 2019. Westpac expects GDP growth to remain subdued at 2.2%yr for the full calendar year.

The Index growth rate has seen a marginal deterioration over the year to date, from –0.37% in December to –0.45% in May. Worsening global conditions have been a key driver of that shift. In particular, a sharp turnaround in the contribution from the US industrial production component has taken 0.57ppts off the headline growth rate. Falling long term bond rates – a reflection of this worsening outlook – have taken a further 0.21ppts off the growth rate via a narrowing in the yield spread component.

Against this, there have been some offsetting positives on the domestic front. In particular the sharemarket component has added 0.66ppts to the Index growth rate with the ASX surging 13% over the year to date, solid gains over the last two months coming despite a significant sell-off in global equity markets. The contributions from other components have been more mixed with some lift from less negative consumer expectations (+0.09ppts) and further gains in commodity prices (+0.08ppts) but a bigger drag from the Westpac-MI Unemployment 19 June 2019 The negative contribution from dwelling approvals is largely unchanged and the contribution from hours worked has remained about neutral.

Stepping back from these more recent shifts, the subtrend reading on growth is being driven by three main components: dwelling approvals, US industrial production and the yield spread with an additional drag coming from consumer sentiment and consumer unemployment expectations. This is being partially offset by the strength in the ASX and Australia’s commodity prices.

The Reserve Bank Board next meets on July 2. The case for further policy easing remains clear, this update showing the economy continues to carry sluggish below trend growth momentum. We continue to expect a further 25bp cut to be delivered in August, the timing allowing the Bank to make a fuller assessment of the impact of its initial move and to provide a complete set of updated forecasts with its August Statement on Monetary Policy.

The labour market will remain a key focus for the policy profile. Westpac’s more downbeat view on this front points to a further 25bp cut in November taking the cash rate to 0.75%.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.