ANZ in conjunction with CoreLogic have released a new housing affordability report, which shows that Australian housing affordability remains stretched despite the recent decline in dwelling values:

VALUE TO INCOME RATIO

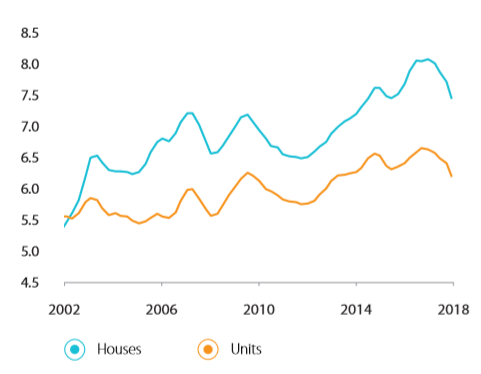

In December 2018, the dwelling price to income ratio across the combined capital cities was recorded at 7.0 times, the lowest reading since June 2016. The improved affordability position is the result of lower housing values against a subtle rise in household incomes. For houses the ratio was 7.5 times, down from 7.7 times the previous quarter and 8.1 times the previous year. For units, the ratio was recorded at 6.2 times which is down from 6.4 times the previous quarter and 6.6 times the previous year.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.