DXY was soft again last night. EUR up and CNY down:

The Australian dollar lifted against all DMs:

And EMs:

Advertisement

Gold broke out of its giant, bullish ascending triangle:

Oil fell:

Big miners rose:

Advertisement

With metals:

EM stocks were stalled:

Junk stable:

Advertisement

Treasuries were bid:

And bunds:

And local bonds:

Advertisement

Stocks held on:

Westpac has the wrap:

Event Wrap

The Dallas Fed regional factory survey fell to a three year low in June of 12.1 from -5.3, below expectations and yet another sign that the global manufacturing slump is spreading to the US. New orders and production firmed slightly but outlook indicators and CAPEX plans tumbled.

Germany’s IFO survey for June slipped to 97.4, as expected, from 97.9 in May. Current conditions actually lifted to 100.8 (prior 100.7. est. 100.3) but the slip in the more market sensitive expectations to 94.2 (prior 95.2, est. 94.6) weighed on sentiment, even if the IFO survey avoided the slump in expectations seen in the ZEW surveys

Event Outlook

NZ: The trade balance for May is expected to be a surplus os $250m.

Australia: RBA Assistant Governor Bullock speaks on the Australian payments system in Berlin (5:00 pm AEST).

US: Apr FHFA house prices and Apr S&P/CS home price index are expected to show a continued gradual slowing in dwelling price growth while May new home sales are seen to bounce 1.8% following a 6.9% decline in Apr. Jun Conference Board consumer confidence is anticipated to remain upbeat at 131.0. Fed Chair Powell speaks on the “Economic Outlook and Monetary Policy Review”. Other Fedspeak includes Williams at the OPEN Finance Forum, Bostic on housing, and Barkin in Ottawa.

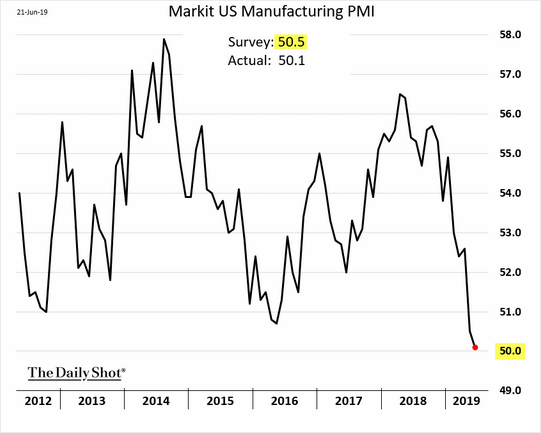

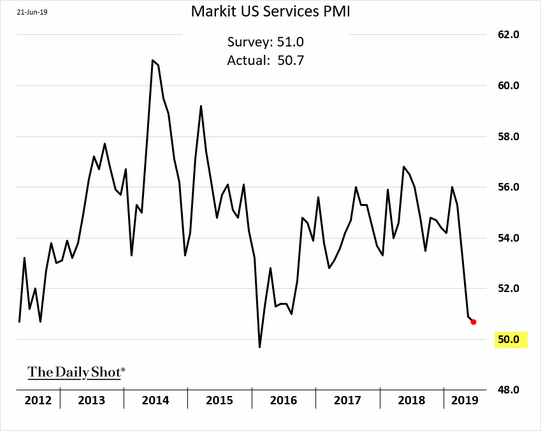

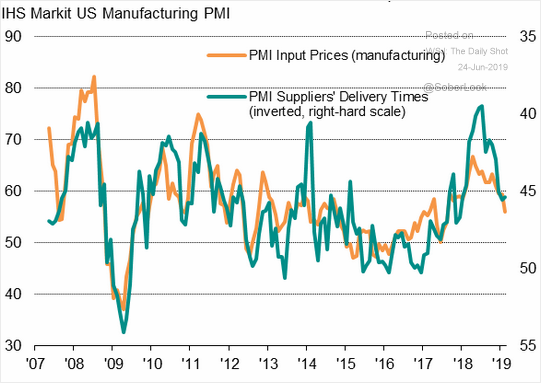

Yesterday’s US PMIs showed the weakness that has spooked the Fed and overjoyed markets:

Advertisement

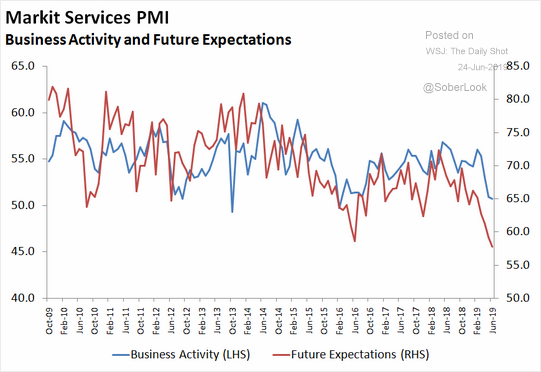

An industrial recession is pretty much baked in. What matters more is a services version:

Advertisement

If that comes to pass it will not be bad news is good news. It will be bad news.

Price pressures are collapsing:

Advertisement

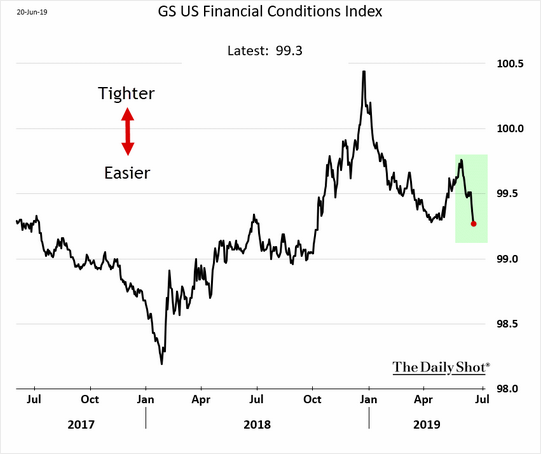

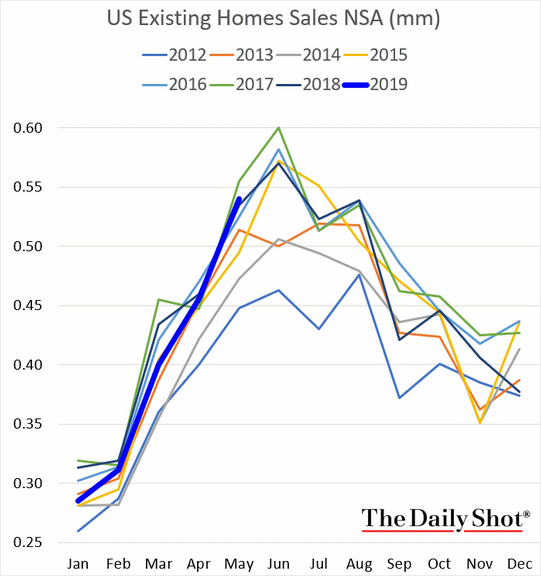

But so are financial conditions:

Which has already aided housing:

Things can only get so bad in the US so long as its housing market holds up so my base is still no US recession. But charts such as these certainly raise risks and that is enough to worry the USD lower, pressuring the AUD higher.

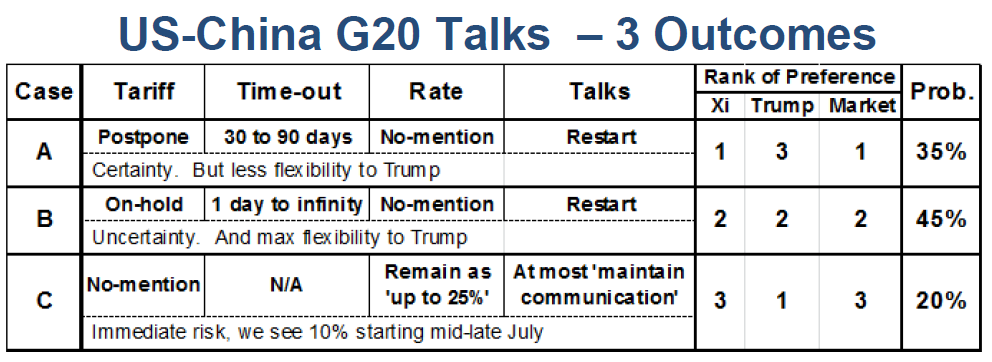

Scenario 1: US holds off on additional China tariffs indefinitely, talks restart (45% probability)

The most likely scenario from the Trump-Xi meeting in Japan is that the U.S. agrees not to impose tariffs on the additional $300 billion in Chinese imports without a concrete timeframe, Straszheim said.

Straszheim says this outcome has a 45% probability of taking place and ranks as the second-most favorable for Trump, Xi and the market.

“This is a jointly recognized time-out. Higher tariffs by the US are not implemented for maybe a short time, maybe a long time,” Straszheim said in a note. “Real negotiations would presumably be re-launched. This is maximum uncertainty on tariffs, and to the Markets and others (in China, the US and Rest of World), but provides maximum flexibility to Trump.”

Scenario 2: US holds off on additional China tariffs for a fixed number of days, talks restart (35% probability)

The second-most likely scenario is the two sides agree to restart trade talks with the U.S. holding off on additional tariffs for a fixed amount of time, Straszheim said.

There is a 35% chance of this outcome taking place and it would be the most favorable to Xi and the stock market as it would give them time to “breathe.” It would also give the market “certainty for more negotiation (and assessment) time.” But what makes this scenario unlikely is it would hamstring Trump in future negotiations.

“Trump has no flexibility during this period,” Straszheim said.

This scenario — along with the first one — would likely benefit trade-sensitive names like Caterpillar and chipmaker stocks. These stocks have underperformed the broader market recently amid the lingering trade fears.

Scenario 3: US and China make no mention of additional tariffs, suggesting they will be implemented soon (20% probability)

This is the worst-case scenario for both Xi and the market as it deals another body blow to the Chinese economy and increases fear among investors that the trade conflict will drag for longer.

“This would be bad news, suggesting a near breakdown on remaining differences,” Straszheim said. “At best the two sides would ‘maintain communications.’”

“In this outcome, no mention of new US tariffs is included in the statements, suggesting the US will proceed with tariffing $300 bln,” he added. Straszheim expects Trump to slap a 10% tariff on those additional Chinese imports in this scenario.

Any scenario is which trade war talks resume will be AUD bullish even if there is little prospect of an outcome.

A combined cutting Fed and trade war pause is an obvious recipe for a higher Australian dollar in the short term. But, asks Morgan Stanley, aren’t lower markets needed to push Trump to a deal?

It’s now confirmed that Presidents Trump and Xi are set to meet at the G20 later this week. And while US administration officials have said we shouldn’t expect a deal but rather a path forward for negotiations, this is still welcome news to anyone looking for relief from the tit-for-tat tariff escalation between the US and China. Communication may not be sufficient to break the escalatory cycle, but it’s a necessary condition. And it’s timely, too, as the US authorization to levy tariffs on a further ~US$300 billion of imports from China takes effect in early July. So as we enter this week, there seems good reason to expect that the G20 will result in a tariff ‘pause’, affording both sides a defined period of time to get negotiations back on track before resorting to further tariff escalation.

But investors beware: while a pause is better than escalation, it won’t refresh the economy enough to forestall a challenging path for risk assets. A pause, particularly one that comes without preconditions and follows a period of heated rhetoric, would be positive, signalling that both sides want to avoid further economic damage. If it coincides with Fed dovishness, a pause could boost investor sentiment and risk asset prices in the short term. However, we’d view this more as a set-up to sell risk than a catalyst to turn more bullish. Consider the following:

Market or economic weakness might be needed to avoid further tariffs and make the pause permanent: Just because the US and China may agree to put more negotiating time on the clock doesn’t mean they’ve made any progress on the points that divide them: codifying IP protections, when to remove existing tariffs, and how much to reduce the trade deficit via asset purchases. These gaps will be difficult to bridge, in our view. As we’ve argued previously in the Sunday Start, we think that game theory is a useful framework to gauge how this could play out. These differences are incentives for each side to escalate. We expect that market or economic weakness would clarify the benefits of de-escalation and lead to a deal, but this may not give investors much comfort.

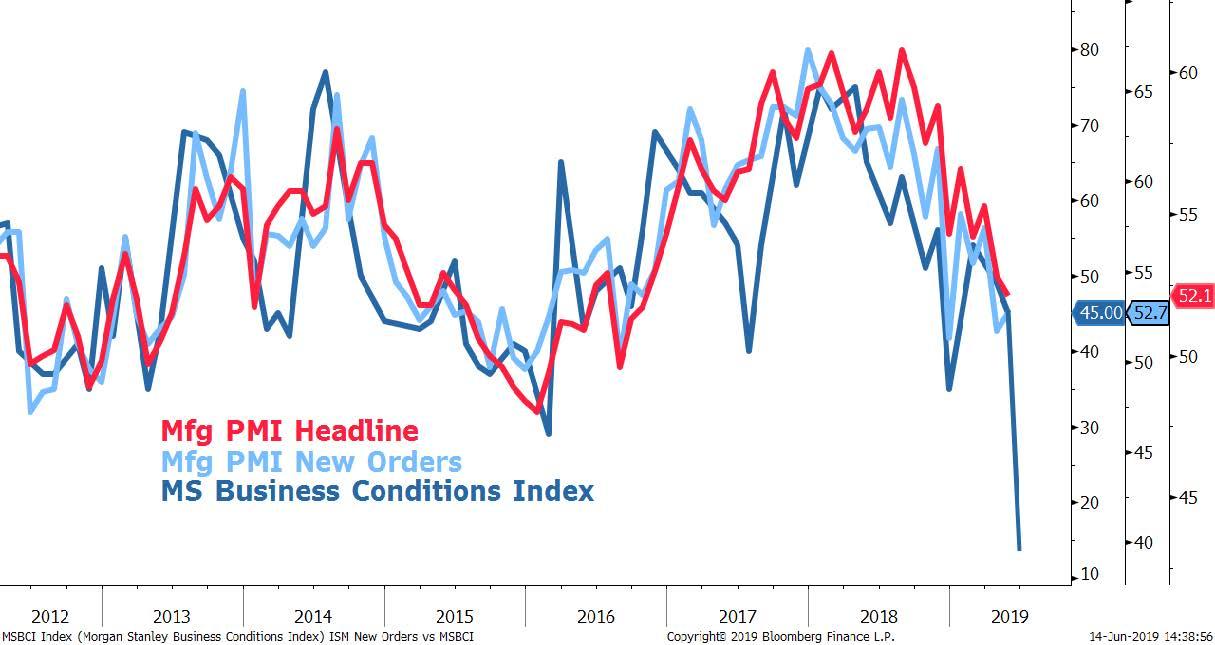

A pause doesn’t fix the ongoing pressure from the ‘downside of fiscal stimulus’: Tariffs are not the sole policy challenge to markets, but rather an accelerant of the risks created by a US policy choice made in 2017: to apply fiscal stimulus through tax cuts when the economy was already in good shape. Back then, we posed this question: though tax reform could prove beneficial over the long term, what did US$1.5 trillion of tax cuts do for the current economic cycle? To us, it’s been more ‘happy hour in America’ than ‘morning in America’. Stimulus in good economic times generally has a lower multiplier effect, and expiring provisions in the tax cuts are already pushing effective corporate tax rates higher and creating pro-cyclical incentives. Not surprisingly, our latest Morgan Stanley Business Conditions Index registered a precipitous drop, reflecting declines in hiring, hiring plans, and capital spending plans among US companies.

Said more simply, the best impacts of the tax cuts to economic growth and corporate profitability were short-lived, are now likely behind us, and may be putting pressure on profit margins and the economic cycle. Avoiding further tariffs won’t change this dynamic.

Tariffs have already impacted the global economy: PMIs had been moving lower since the beginning of 2018, driven mainly by trade tensions. The latest deterioration in manufacturing PMIs reflects a further hit to corporate confidence, with the declines most pronounced in the US, China and Korea. Trade tensions were frequently cited as a concern.

Taken together, we think that the benefits of a pause lie mainly in its ability to delay, but not resolve, downside risks to economic fundamentals. Hence, a pause would reinforce our current views: a range-bound path for the S&P, with a downward skew from current levels; a wider bias for credit spreads; and a preference for government bonds on our economists’ expectation for further Fed easing.

So long as the trade war continues then the AUD can fight that lower.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.