DXY pulled back last night as EUR and CNY fell:

The Australian dollar was mixed against DMs:

But weak against EMs:

Gold held on:

Oil eased:

Metals climbed:

Big miners too:

And EM stocks:

Junk was OK:

Treasuries sold:

Bunds too:

But Aussie bonds were bought:

Stocks flamed out:

Westpac has the wrap:

Event Wrap

The US National Federation of Independent Business May small business survey jumped to 105 from 103.5 – a seven-month high – defying expectations for a pullback amid volatile financial markets and elevated trade tensions. Expectations for the economy, CAPEX plans and hiring intentions all firmed. US producer prices rose 0.1% in May, the annual pace easing to a non-threatening 1.8% – the slowest pace since early 2017.

UK April/May employment report provided surprise lifts in both employment (+32k, est. +4k) and average wages (+3.4% 3m/y, est. +3.2%). Although headline unemployment remained at 3.8%, the overall report was seen as strong despite the uncertainty of Brexit.

BoE MPC members Saunders and Broad

bent added to comments from fellow MPC member Haldane yesterday in suggesting that rates would be higher under a smooth Brexit, that markets are under-pricing the potential of rate moves and that a hike could even occur prior to any Brexit resolution. However, Broadbent added, in response to Parliamentary Select Committee questioning, that he could not give any clarity over how policy might alter if there is a no-deal Brexit due to the potential volatility it might generate.Event Outlook

NZ: Migration for April is released, as is electronic retail sales for May which is expected to have gained 0.5%.

Australia: Westpac-MI Consumer Sentiment was last at 101.3. This update will provide consumers’ reaction to the Federal election result and June RBA rate cut. RBA Assistant Governor (Financial Markets) Kent gives remarks at the Australian Renminbi Forum, Melbourne 9:25 am. RBA Assistant Governor (Economic) Ellis gives a speech titled “Watching the Invisibles”, Melbourne 7:00 pm.

China: May CPI and PPI are released.

Euro Area: ECB President Draghi speaks at the “Resilience to Global Headwinds” conference in Frankfurt.

US: May CPI is expected to show annual inflation edging down to 1.9% from 2.0% while core inflation holds at 2.1%.

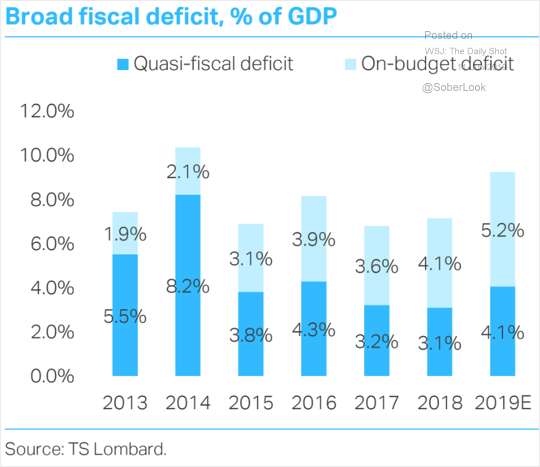

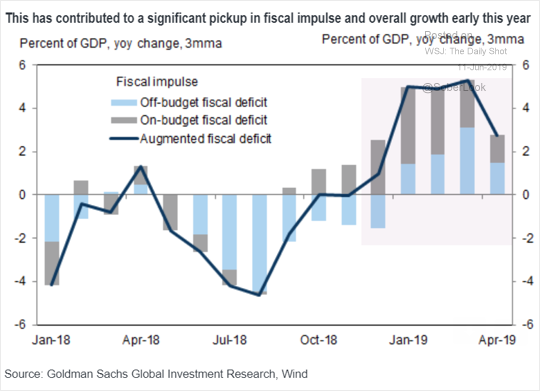

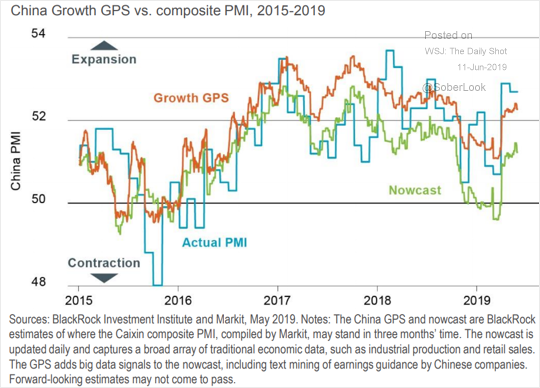

Not much by way of data but there is an interesting short term dynamic emerging in which China is suddenly winning the trade war via better growth than the US. The former has primed the fiscal pump with direct stimulus as we know:

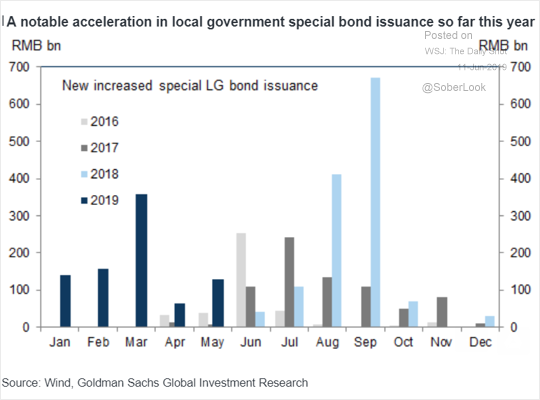

Local governments have been especially active:

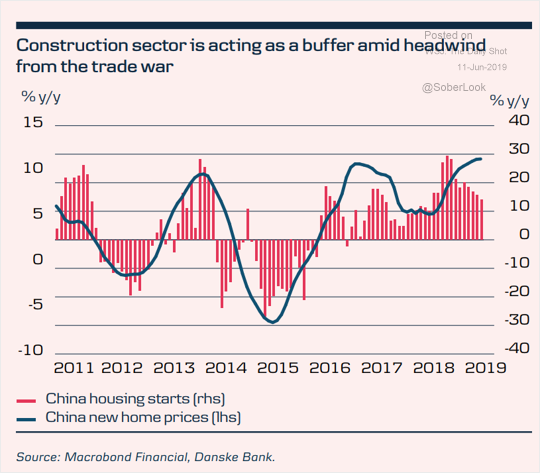

But the real key is ongoing strength in empty apartments:

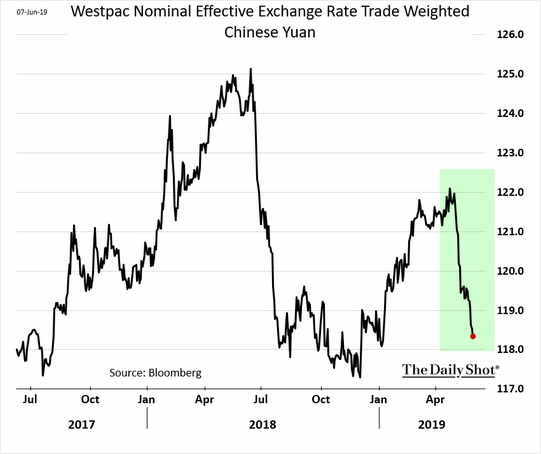

And a falling CNY:

Leading a growth rebound just as US growth comes under intensifying pressure:

The easiest way to represent this for the AUD is to compare it with iron ore prices:

As you can see, the AUD is unusually out of step with bulk commodity prices today. This is largely thanks to the negative yield spread to Australia. As the Fed starts cutting on a slowing US economy, reducing the spread – this gap may close a little in the short term.

That said, I do not expect it to get far because the RBA is also going to cut more than is priced in markets, as well as other central banks which will trail the Fed, including China’s.

As well, medium and longer term this is no victory for China. It is a short term political win at the expense of the longer term as it leads to ever more misallocated credit, ever less productivity growth, and a giant debt overhand that will only serve to bog China down into the middle income trap.