DXY posted a minor recovery last night as EUR fell and CNY was stable:

The Australian dollar fell popped and dropped against DMs:

It was mixed against EMs:

Advertisement

Gold still hinting at further DXY weakness:

Oil is screaming trouble for growth and markets:

Metals were weak:

Advertisement

And minors:

EM stocks fell:

US junk gained again, EM softened:

Advertisement

Treasuries were bid but the curve steepened:

Bunds were bid period:

Aussie bonds too:

Advertisement

Stocks recovered some more:

US data was again the overnight pivot for forex and the Aussie dollar. The Battler broke out when ADP employment posted weak:

Private sector employment increased by 27,000 jobs from April to May according to the May ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…“Following an overly strong April, May marked the smallest gain since the expansion began,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Large companies continue to remain strong as they are better equipped to compete for labor in a tight labor market.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Job growth is moderating. Labor shortages are impeding job growth, particularly at small companies, and layoffs at brick-and-mortar retailers are hurting.”

Advertisement

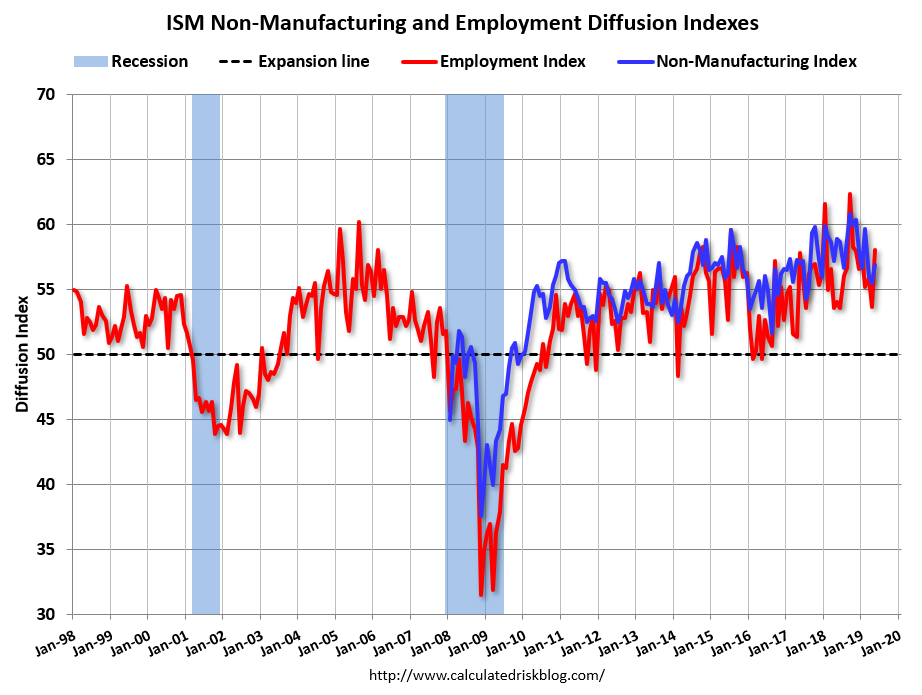

But that lasted just 40 minutes before the Services ISM arrived:

“The NMI® registered 56.9 percent, which is 1.4 percentage points higher than the April reading of 55.5 percent. This represents continued growth in the non-manufacturing sector, at a slightly faster rate. The Non-Manufacturing Business Activity Index increased to 61.2 percent, 1.7 percentage points higher than the April reading of 59.5 percent, reflecting growth for the 118th consecutive month, at a faster rate in May. The New Orders Index registered 58.6 percent; 0.5 percentage point higher than the reading of 58.1 percent in April. The Employment Index increased 4.4 percentage points in May to 58.1 percent from the April reading of 53.7 percent. The Prices Index decreased 0.3 percentage point from the April reading of 55.7 percent to 55.4 percent, indicating that prices increased in May for the 24th consecutive month. According to the NMI®, 16 non-manufacturing industries reported growth. The non-manufacturing sector continues to experience a slight uptick in business activity, but it is still leveling off overall. Respondents are mostly optimistic about overall business conditions, but concerns remain about tariffs and employment resources.”

From thereon it was USD up and AUD down.

Advertisement

Obviously non-farm payrolls this Friday night looms as crucial. A weak print and Fed bets will redouble, putting another thermal under the AUD and vice versa. The signals are mixed, from Calculated Risk:

The ADP employment report was weak this month with just 27,000 jobs added. In general, the ADP report hasn’t been very useful in predicting the BLS report for any one month, but this does suggest some downside risk to the May employment report to be released on Friday.

However, the ISM non-manufacturing report suggested solid employment growth in May. So I thought I’d look back at the three previous years and compare the ADP and ISM reports to the BLS report.

This is a very small sample, but neither the ADP or the ISM non-Mfg employment index correlates well with the BLS report, but the ISM report has probably been a little more useful. For the previous three years, the ADP and the ISM non-Mfg employment index moved somewhat together – but this month the readings were very different.

That’s about as clear as mud. Looking beyond this week, the US economy is still likely to slow further as markets remain pressured, the oil patch stalls, and the fiscal cliff hits. These will be enough to slow employment and wages, and trigger the Fed.

My view that the AUD is headed higher short term remains.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.