The DXY bull returned Friday night as CNY and EUR sank:

The Australian dollar is breaking down to multi-year lows against all three major developed currencies:

Advertisement

It even sank versus EMs:

Markets are still very short Aussie at -63k contracts:

Gold tried and failed to break out as DXY rallied:

Advertisement

Oil firmed on Iran tensions:

Base metals were crushed by DXY:

Advertisement

Big miners flamed out:

EM stocks always hate strong DXY:

So does junk:

Advertisement

Treasuries were soft:

Bunds are madly bid:

Not as mad as AUD bonds!

Advertisement

Stocks softened:

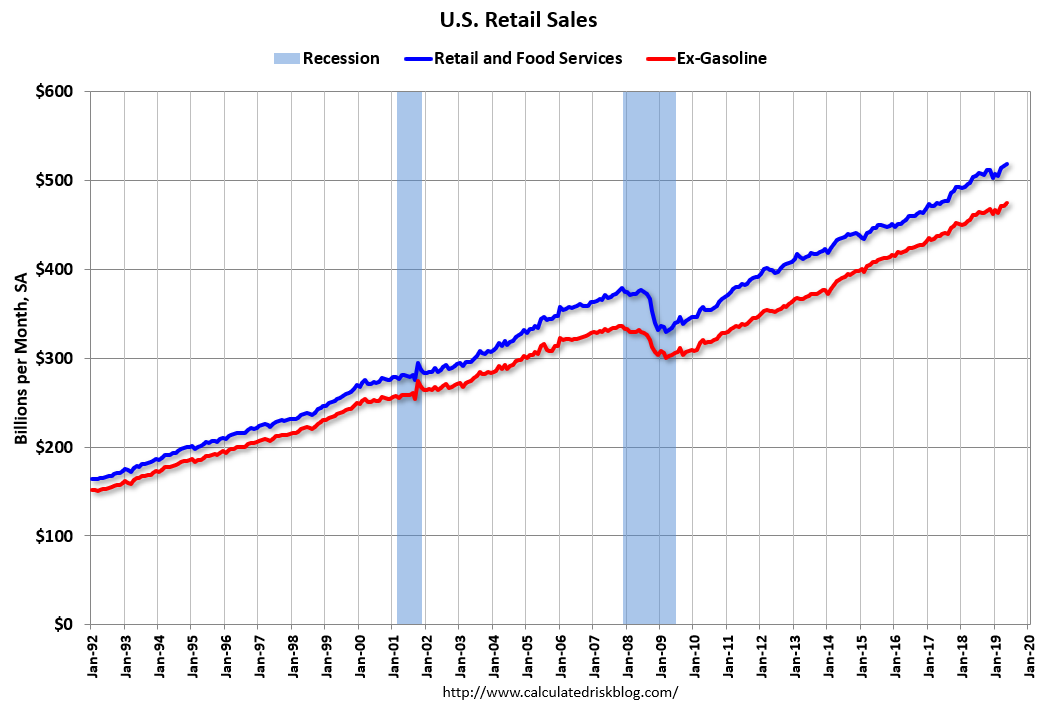

The major data releases were in the US. Retail sales were rock solid:

Advance estimates of U.S. retail and food services sales for May 2019, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $519.0 billion, an increase of 0.5 percent from the previous month, and 3.2 percent above May 2018. … The March 2019 to April 2019 percent change was revised from down 0.2 percent to up 0.3 percent.

Advertisement

Industrial production also rebounded. Both contrasted with weak Chinese data which did not help CNY and DXY took off.

But there is also a safe haven bid into DXY here. From Gavekal:

• Renewed fears of a renminbi devaluation: The May 5 upending of the China-US trade negotiations triggered a mild sell-off in the renminbi. From there, investors started to fear that if China was forced to choose weaker growth or a weaker currency, it would pick the former and sacrifice the latter. Fears thus mounted that the likeliest path for the renminbi was lower, and this would cause a global deflationary shock.

• Credible fears of faltering global growth: Concerns escalated after Trump threatened Mexico with export tariffs unless it changed its immigration policies. This showed Trump’s willingness to use the tariff weapon for matters other than trade disputes. It also showed that no one was safe, as it had been assumed that with the US-Mexico-Canada deal set to reach Congress, Mexico would be a winner of US-China tensions. This raises the specter of confused and frightened business leaders simply sitting on their hands until US policy on trade becomes clearer. The risk is that this triggers a collapse in global capital spending, and employment.

• Fears of a tech bust: The US is fighting China on the tech sector battlefield. And as anyone living in the north east of France during the last two European wars will tell you, having your territory earmarked as the next battlefield is bad news. Placing technology front and center in this conflict ensures that China will intensify its attempt to lessen domestic firms’ reliance on US suppliers. This will be a double-blow for US producers, who face both a shrinking export market, and the long term threat of new government funded rivals. At the same time, the US Justice Department appears to be ramping up its efforts against Big Tech, possibly in time for the next electoral cycle (perhaps to ensure that Big Tech makes more of an effort to be politically neutral?). And all this is happening at a time when recent new equity offerings (Uber, Lyft, Pinterest) have shown that the entire tech funding industry may have gotten ahead of itself.

• Fears of a eurozone banking crisis: The total market value of eurozone banks is roughly that of JP Morgan (around US$350bn). For an economic zone whose size is meant to rival that of the US, and whose growth depends heavily on bank credit, this is embarrassing. Of course, European banks’ long agony does stem from the European Central Bank’s negative interest rate policies. But as their stock values continue to plumb new depths, investors worry that another deflationary shock lies around the corner.

• Belief that the US dollar would take another leg up: Taken together, the rising odds of a “no-deal” Brexit, embattled eurozone banks, a dovish ECB and a weakened China seemed to prepare the ground for the US dollar to break out from its trading range. For as I have argued before, a strong dollar is the angular stone on which the deflationary edifice rests; it typically leads to weaker growth and lower asset prices across emerging markets. It also means weaker growth for US manufacturing and lower commodity prices. Thus, as the US dollar looked set to break out (and as oil prices tanked), market participants naturally bid up US treasuries.

Advertisement

And the note predated Iran attacks. Hong Kong insurrection and BoJo firming his Brexit plans. Developments in the former did not help, via The Guardian:

The US has accused Iran of detaining the crew of one of two oil tankers attacked in the Gulf of Oman this week, as the UK also joined in formally blaming the country, saying no other nation or group “could plausibly be responsible”.

Washington claims Iran is behind a succession of recent shipping attacks in the Gulf. It said grainy video published on the US Central Command’s website provided evidence of Iran’s involvement in Thursday’s attacks. The footage purportedly shows an Iranian boat removing an unexploded mine from one of the vessels.

…On Friday night the UK formally joined the US in attributing the attacks to Iran. After carrying out its own assessment – the product of an internal UK intelligence discussion – the Foreign Office issued a statement saying: “It is almost certain that a branch of the Iranian military – the Islamic Revolutionary Guard Corps – attacked the two tankers on 13 June. No other state or non-state actor could plausibly have been responsible.”

It continued: “There is recent precedent for attacks by Iran against oil tankers. The Emirati-led investigation of the 12 May attack on four oil tankers near the port of Fujairah [in the UAE] concluded that it was conducted by a sophisticated state actor. We are confident that Iran bears responsibility for that attack.”

The foreign secretary, Jeremy Hunt condemned the attacks but called for a diplomatic solution. He said: These latest attacks build on a pattern of destabilising Iranian behaviour and pose a serious danger to the region. It is essential that tankers and crews are able to pass through international waters safely. We call on Iran urgently to cease all forms of destabilising activity. The UK remains in close coordination with international partners to find diplomatic solutions to de-escalate tensions.”

Good luck with that right now. One could see Iranian tensions as, in part, a proxy war with China given it is the only one now siphoning off its oil.

Advertisement

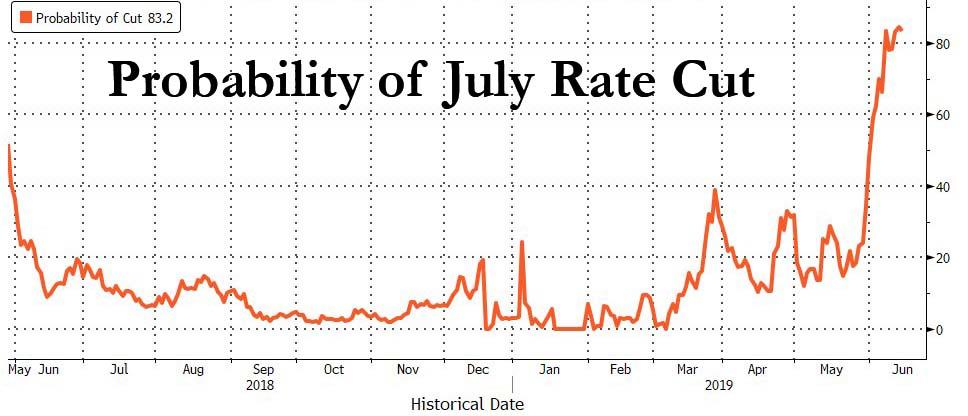

Whatever the case, the risks were such that, despite good data, markets barely budged on pricing for an imminent Fed cut:

I still think markets are a little ahead of the curve for timing the Fed cut. Goldman has more:

Advertisement

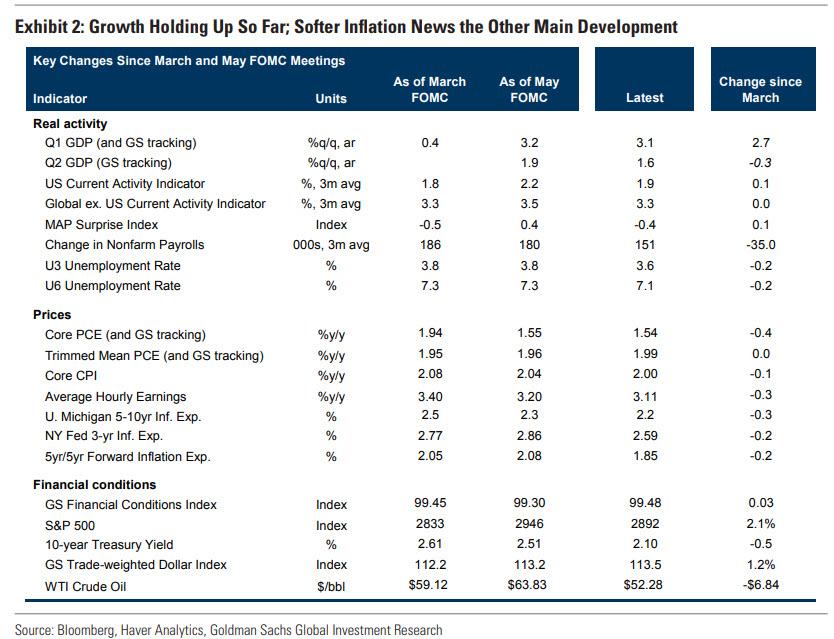

“since the March SEP meeting, stock prices are higher, the unemployment rate fell to a 50-year low, consensus growth forecasts are unchanged, and the very tariffs on Mexico that prompted the latest calls for rate cuts have been taken off the table.” Not only that, but the economy continues to chug along largely as expected: outside of May payrolls, the growth data still look decent: Goldman’s Q2 GDP tracking estimate has rebounded to +1.6%, Atlanta Fed GDPNow is +2.1%, and the bank’s own tracker of private final demand is at an even healthier pace (+2.8%).

“…while markets are aggressively priced for rate cuts, we believe the dovish shift indicated by Fed commentary has been more marginal in nature. For example, we take much less signal than other commentators and market participants from Chair Powell’s promise that “as always, we will act as appropriate to sustain the expansion.” In our view, this was not a strong hint of an upcoming cut but was simply meant to provide reassurance that the FOMC is well aware of the risks

Goldman has been far too hawkish throughout this cycle but I think they are roughly right that the Fed doesn’t need to move imminently. It can set up first. If for no other reason than the paradox that markets have already reflated on said cuts.

So, my dalliance with a short term pop for the Australian dollar has been shot down, run down, reversed over and buried. I saw it as very short term before reversing lower as Australian easing overshoots market expectations. But if the Fed is slower to cut than the RBA, or these multiplying risks keep mounting, then the Australian dollar will keep on keeping on, down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.