DXY was soft last night as EUR firmed. CNY is stable:

The Australian dollar was firm against all but the EUR:

Advertisement

It was mixed against EMs:

Gold bounced some more and is forming a very large bullish ascending triangle pattern though it will have to break above $1400 to confirm it which is some further wood to chop:

Advertisement

Oil rebounded on OPEC hopes:

Metals too:

And big miners:

Advertisement

EM stocks struggled:

Junk tracked oil as usual:

Treasuries sold:

Advertisement

The bund curve flattened:

Stocks enjoyed more Powell “put”:

Westpac has the wrap:

Advertisement

Event Wrap

US trade deficitimproved modestly in April to $50.8bn from $51.9bn; exports and imports both fell a sharp 2.2% in the month across a broad base, tariffs, weaker global growth and softening US domestic demand likely all at play. US jobless claims continue to hover in the low-200k region, 218k last week, consistent with a strong labour market. Dallas Fed President Kaplan repeated his comments from yesterday that downside risks have increased but it’s too early to make a call on the direction of rates. NY Fed President Williams played down the inverted yield curve as recession signal and indicated an open mind on the outlook for policy and the economy.

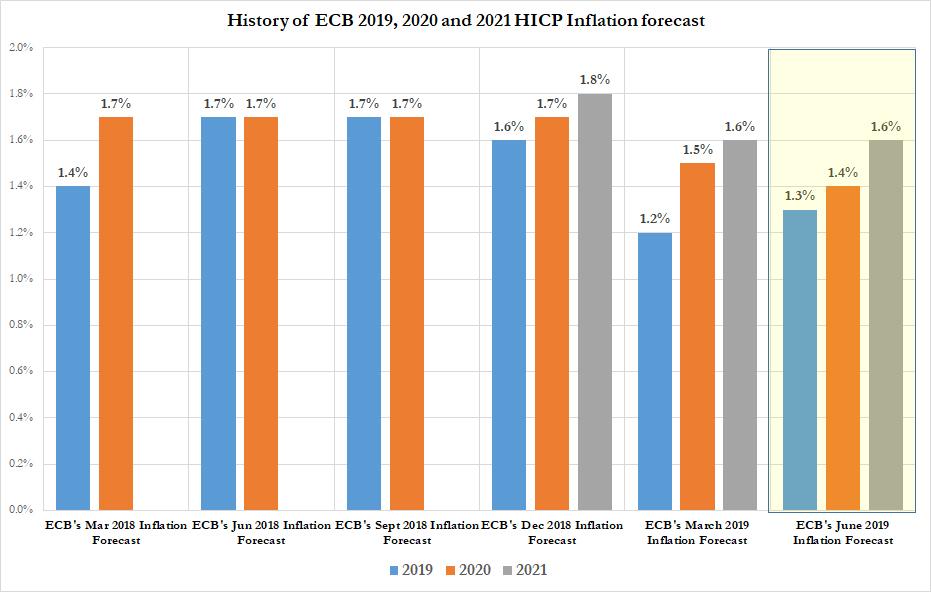

ECB extended yet further its forward guidance “at least through 1H 2020” (previously “end of 2019”) whilst it kept other policy measures unchanged, as expected. The regular update of ECB Staff projections had only mildly lower profiles for growth, but also unemployment, and inflation. The detailing of TLTRO III yields was also well within the range of market expectations.

German April factory orders surprised on the upside with a mild lift of +0.3%m/m (est. flat) and a lift to +0.8%m/m (prior +0.6%m/m) in March. Eurozone final 1Q GDP was unchanged at +0.4%q/q and 1/3%y/y. However, Capex was increased at the expense of a mild pullback in household spending.

Event Outlook

NZ: Q1 building work is expected to rise by 1.1% (Westpac at 0.7%), and will be an input into Q1 GDP estimates.

Australia: Apr housing finance is expected to show the number of owner occupier approvals unchanged in the month.

US: May non-farm payrolls are anticipated to increase by 175k and hold the unemployment rate flat. The annual pace of average hourly earnings is seen to hold at 3.2%, having eased back slightly from Mar’s 3.4% pace. Fedspeak involves Dalyto university students in Singapore.

The key release on the night was the ECB which remains delusional:

Based on our regular economic and monetary analyses, we have conducted a thorough assessment of the economic and inflation outlook, also taking into account the latest staff macroeconomic projections for the euro area. As a result, the Governing Council took the following decisions in the pursuit of its price stability objective.

First, we decided to keep the key ECB interest rates unchanged. We now expect them to remain at their present levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Second, we intend to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, regarding the modalities of the new series of quarterly targeted longer-term refinancing operations (TLTRO III), we decided that the interest rate in each operation will be set at a level that is 10 basis points above the average rate applied in the Eurosystem’s main refinancing operations over the life of the respective TLTRO. For banks whose eligible net lending exceeds a benchmark, the rate applied in TLTRO III will be lower, and can be as low as the average interest rate on the deposit facility prevailing over the life of the operation plus 10 basis points.

The endlessly deferred recovery. Straight from the RBA school of central bank idiocy. Or, rather, the other way around. A slow moving ECB and strong EUR also adds to DXY weakness and AUD strength at the margin.

Advertisement

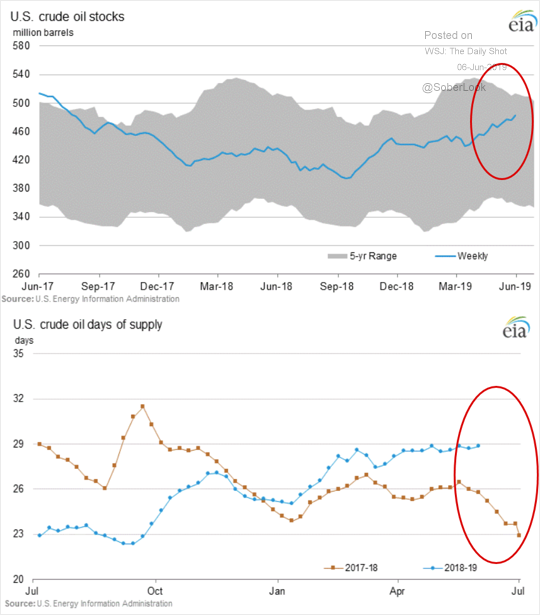

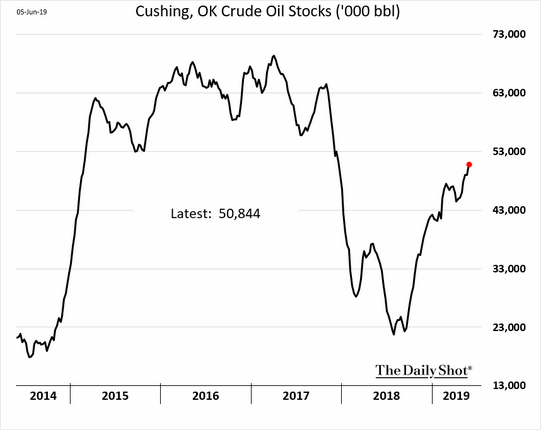

Global growth is still getting worse not better with no end to that in sight. We need only looks at oil to see the process unfolding. MS shows demand is very weak:

Inventories are building fast in the US:

Advertisement

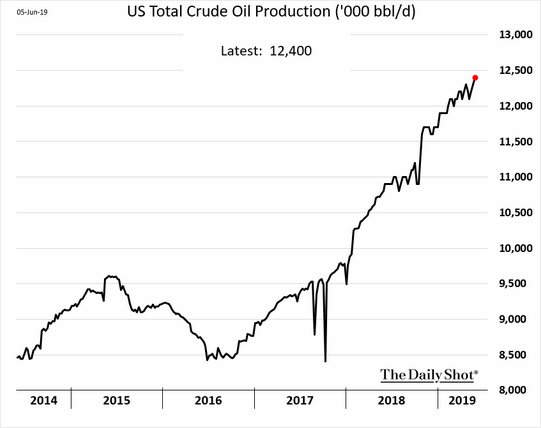

As US production stays strong:

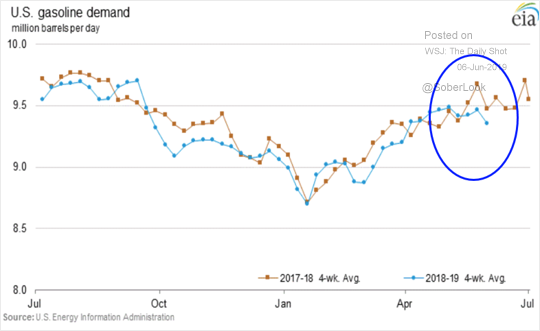

And demand weakens:

Advertisement

This as Iran, Libya and Venezuala pull production. The oil price already has a deflationary shock built in:

And unless OPEC does something really radical, worse is coming.

Advertisement

It is interesting to note that gold and oil have become inversely correlated since 2016:

Basically because for the first time in decades the US is the swing producer and its growth is now oriented around oil production not consumption. DXY has also begun to track oil since 2016.

Advertisement

Bringing this back to the AUD, it also has a history of tracking the oil price but, now, as oil and gold go opposite ways one wonders if that will hold. In the short term, I still think that as DXY falls with oil (and Fed cuts) then AUD will be bid with gold, though perhaps not so strongly. Indeed, if oil falls get the upper hand then AUD will probably reverse downwards as global recession marches in.

Sounds like a good argument for an Australian gold miner, in the short term, at least.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.