DXY firmed a little last night as CNY and EUR fell:

The Australian dollar popped and dropped:

As did gold:

Advertisement

Oil was weak:

Metals firm:

Miners soft:

Advertisement

EM stocks more so:

Junk got bashed:

As the Treasury curve was monstered:

Advertisement

Bunds bid:

Aussie bonds are at new highs:

And stocks melted:

Advertisement

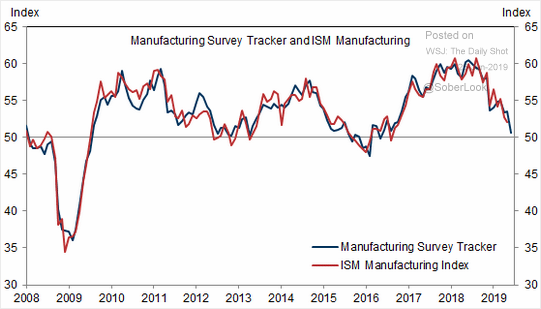

Data was mixed. The Dallas Fed was soft and a manufacturing recession is virtually baked in:

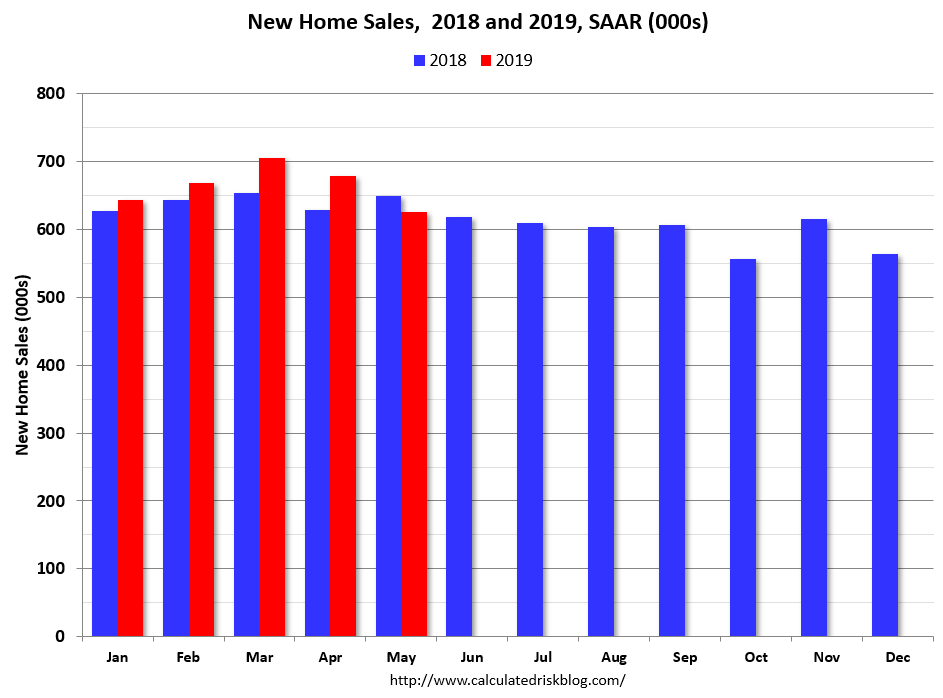

However, new home sales were decent if down for the month:

Advertisement

“Sales of new single‐family houses in May 2019 were at a seasonally adjusted annual rate of 626,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 7.8 percent below the revised April rate of 679,000 and is 3.7 percent below the May 2018 estimate of 650,000.”

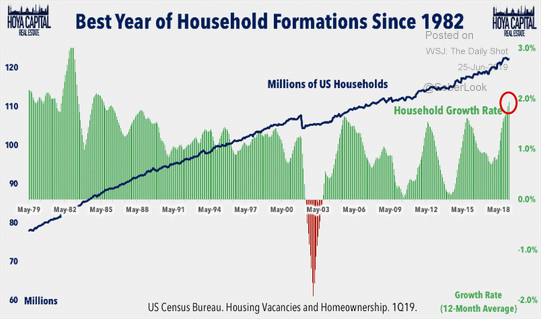

Household formation remains strong:

The US consumer will have to break down before any real recession can take place. For that there will still need to be some kind of further shock.

Advertisement

The stock market is one candidate. The Fed was just not dovish enough for markets as James Bullard ruled out a 50bps cut:

And the Fed chair was calm in another speech:

Advertisement

Let me turn now from the longer-term issues that are the focus of the review to the nearer-term outlook for the economy and for monetary policy. So far this year, the economy has performed reasonably well. Solid fundamentals are supporting continued growth and strong job creation, keeping the unemployment rate near historic lows. Although inflation has been running somewhat below our symmetric 2 percent objective, we have expected it to pick up, supported by solid growth and a strong job market. Along with this favorable picture, we have been mindful of some ongoing crosscurrents, including trade developments and concerns about global growth. When the FOMC met at the start of May, tentative evidence suggested these crosscurrents were moderating, and we saw no strong case for adjusting our policy rate.

Since then, the picture has changed. The crosscurrents have reemerged, with apparent progress on trade turning to greater uncertainty and with incoming data raising renewed concerns about the strength of the global economy. Our contacts in business and agriculture report heightened concerns over trade developments. These concerns may have contributed to the drop in business confidence in some recent surveys and may be starting to show through to incoming data. For example, the limited available evidence we have suggests that investment by businesses has slowed from the pace earlier in the year.

Against the backdrop of heightened uncertainties, the baseline outlook of my FOMC colleagues, like that of many other forecasters, remains favorable, with unemployment remaining near historic lows. Inflation is expected to return to 2 percent over time, but at a somewhat slower pace than we foresaw earlier in the year. However, the risks to this favorable baseline outlook appear to have grown.

But markets want MOAR. Valuations are only so inflated owing to the equity risk premium emanating from crushed bond yields so such talk of steady “insurance” cuts just won’t cut it.

For the time being, the push/pull of Federal Reserve easing is dominant in the value of the Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.