Or, rather, the AFR’s war on rate cuts on behalf of the major banks turns complete nonsense. It’s much better for mortgage hog banks if we use fiscal policy and APRA cuts than it is rate cuts, as Goldman has noted:

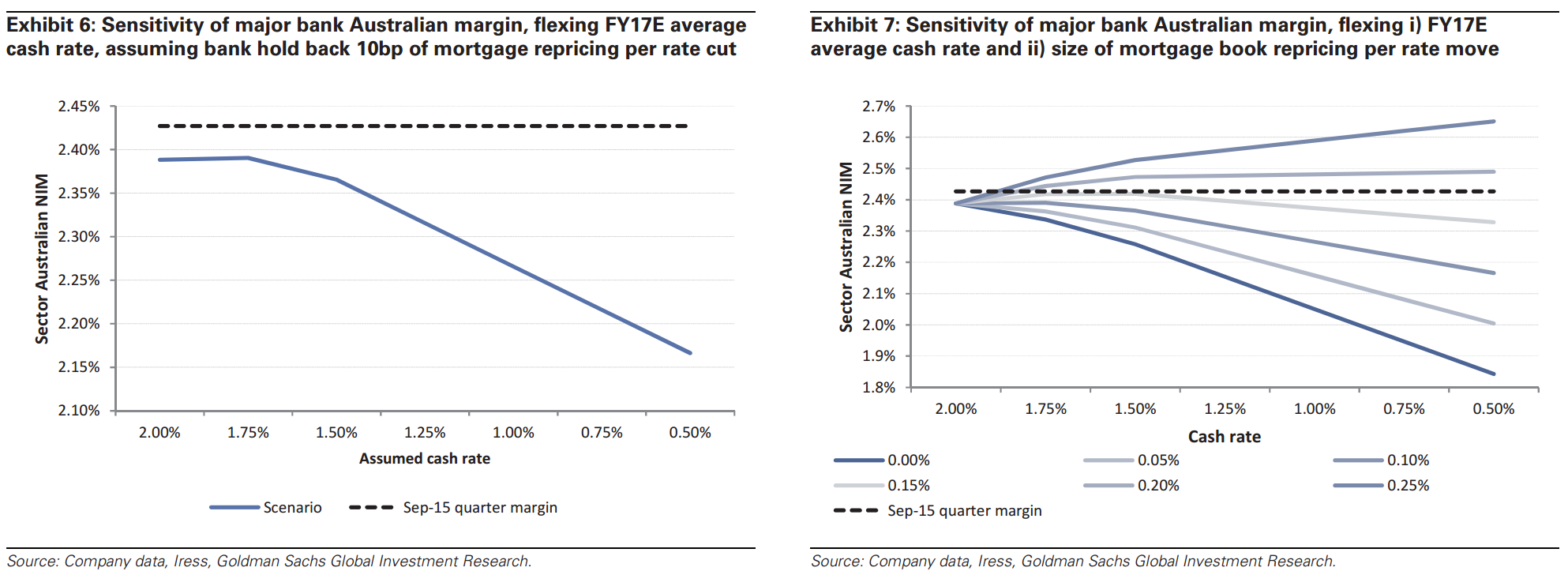

…if the cash rate was to fall below 1.50%, every additional rate cut thereafter would shave about 5 bp off sector margins. The sensitivity of margins to falling rates accelerates once the cash rate falls below 1.50% because the various levers the banks have at their disposal become less flexible as the cash rate approaches zero and we would particularly highlight the following:

Our expectation is that term deposit (and cash management to a lesser degree) pricing will become quite sticky as the cash rate falls below 2.0%, as was the experience in the both the United Kingdom and Canada in 2008/09. This will particularly be the case as the domestic banking regulator, APRA, shifts its focus in 2016 towards the Net Stable Funding Ratio (NSFR), which is likely to place pressure on the banks to both term out and improve the quality of their funding (i.e. preference for deposits over wholesale). Furthermore, we note that the recent move out in funding costs has historically correlated with higher rates being paid by the banks on deposits (Exhibit 2).

We estimate that the replicating portfolio represents about a 5bp p.a. margin headwind for the banks over the next 2-3 years.

We’ve had a whole bunch of group think AFR journos bashing rate cuts for weeks on the major bank’s behalf. Today we can add Chanticleer on the thinnest of excuses:

Once again, he indirectly called on governments to adopt structural policies that “support firms expanding, investing, innovating and employing people”.

It is hard to think of a better person to expand on this topic than Cannon-Brookes, who is co-CEO of Atlassian. This home-grown software-as-a-service company has sold its products to 144,000 companies, it employs 3000 people in more than five countries and is valued at $US28 billion on the Nasdaq exchange in New York.

…Let’s face it, a handful of basis points not passed on is irrelevant compared to the available discounts, which are up to 170 basis points lower than the standard variable rate of about 5.12 per cent.

Advertisement

Great stuff, Mike, let’s get on with the reforms that will unleash productive enterprise:

negative gearing reform;

franking credits reform;

boosted incentives for capital investment;

boosted incentives for competition and innovation;

breaking the east coast gas cartel for cheap energy;

lower dollar policies like cutting interest rates while lifting macroprudential requirements;

reforms that will make banks lend more to business than mortgages.

Oh…whoops…that sounds like Labor. But no! From the AFR editorial:

Advertisement

Governor Phil Lowe has made a start, but only a start, in providing a compelling rationale for taking the Reserve Bank’s monetary policy into risky and uncharted territory, cutting its cash rate to a record low of 1.25 per cent and signalling a further reduction to 1 per cent within months. And, with Treasurer Josh Frydenberg, he has made just a start on forcing attention onto what needs to be done elsewhere to revive Australia’s economic growth performance: onto “structural policies that support firms expanding, investing, innovating and employing people”.

…Australia has just been through an election that, thankfully, rejected the Labor opposition’s agenda of higher taxes, bigger government, more regulation and returning bargaining power to the trade unions.

Such are the contradictions of “businessomics” that the AFR wouldn’t recognise productive structural reform if it ran it down in a truck.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.