US April durable goods orders only missed estimates by a small amount (-2.1%m/m, est. -2.0%m/m) and non-defence, ex transport (0.0%m/m, est. -0.1%) showed that other than impacts from Boeing the data seemed solid. However, downward revisions to March gave a decidedly more negative profile to the volatile data series (headline +1.7%m/m from 2.6%m/m, non-defence/ex transport -0.6%m/m from flat). This raises downside risks for both 1Q GDP and 2Q GDP.

UK PM May announced her resignation. She will step down from Conservative Party leader on 7 June (so will remain PM in word at least during Trump’s 3-6 June State Visit) and then act as care-taker PM until a new leader is elected. The process is likely to take several weeks, but is hoped to complete prior to the summer recess begins (20July).

UK April retail sales defied expectations and ex-fuel sales dipped only -0.2%m/m after a revised +1.4%m/m (prior 1.2%m/m) for March. Better weather and strong on-line clothing sales offset weakness in High Street activity but the real story is that consumers remained active despite Brexit uncertainty.

Event Outlook

There are no major events on Monday. The US and UK have holidays.

European Parliament elections will be wrapping up, with results only released after the last poll is closed (after 7 am Sydney time today). Early indications are that voter turnout could be the highest in 20 years. Exit polls are indicating a populist win in France.

US growth is on the slide, as expected. Various pundits now have H1 with a “1” in front of it. From Merrill Lynch:

Advertisement

We lowered 2Q GDP tracking by 0.2pp to 1.6%, while 1Q remained unchanged at 2.9%.

From Goldman Sachs:

We lowered our Q2 GDP tracking estimate by two tenths to +1.3% and our past-quarter GDP tracking estimate for Q1 by one tenth to +3.0% (qoq ar).

The New York Fed Staff Nowcast stands at 1.4% for 2019:Q2. News from this week’s data releases decreased the nowcast for 2019:Q2 by 0.4 percentage point. Negative surprises from the Advance Durable Goods Report drove most of the decrease.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2019 is 1.3 percent on May 24, up from 1.2 percent on May 16.

Advertisement

Trade war impacts will be marginal but worsen this slowdown even as they lift inflation, via Alphaville:

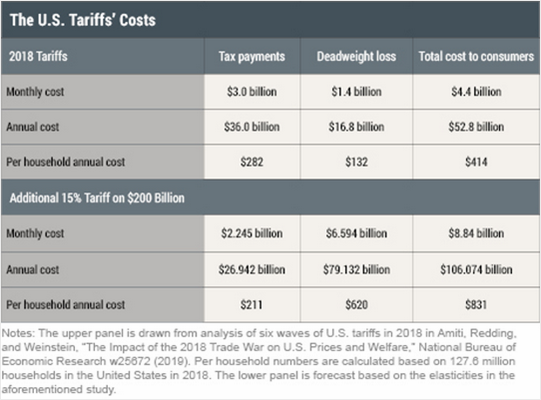

In a new report, the New York Fed puts a number on just how much it’ll cost. According to estimates crunched by Mary Amiti, Stephen Redding and David Weinstein, the latest round of tariffs will cost the average American household $831 this year, or collectively $106bn annually. As the FT reported here, it’s a combination of an added tax burden borne on importers, who have had to pay more for the same goods since China has not adjusted its prices, and “deadweight losses,” which accumulate when firms switch to cheaper but less efficient producers to reduce their exposure to tariffed goods.

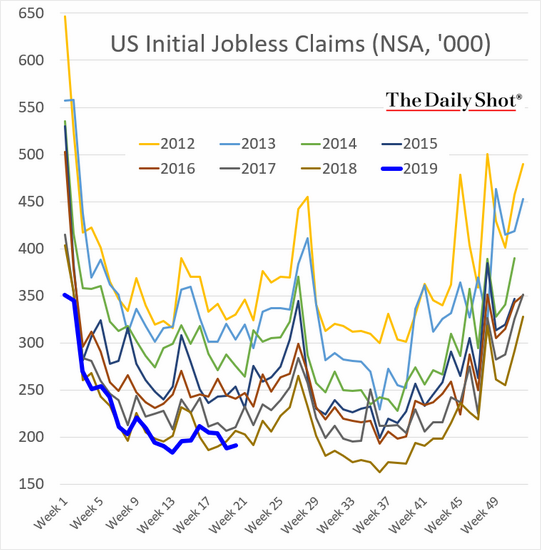

And the US labour market remains in good health:

Advertisement

With no serious damage to the economy unless housing rolls over and it is so far OK, via Calculated Risk:

1) When the YoY change in New Home Sales falls about 20%, usually a recession will follow. The one exception for this data series was the mid ’60s when the Vietnam buildup kept the economy out of recession. Note that the sharp decline in 2010 was related to the housing tax credit policy in 2009 – and was just a continuation of the housing bust.

2) It is also interesting to look at the ’86/’87 and the mid ’90s periods. New Home sales fell in both of these periods, although not quite 20%. As I noted in earlier posts, the mid ’80s saw a surge in defense spending and MEW that more than offset the decline in New Home sales. In the mid ’90s, nonresidential investment remained strong.

Although new home sales were down towards the end of 2018, the decline wasn’t that large historically. As I noted last Fall, I wasn’t even on recession watch. Now new home sales are up year-over-year. No worries.

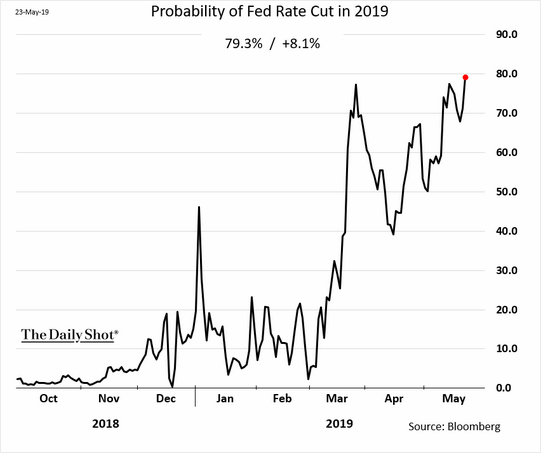

Which is not to say that the Fed won’t cut but it will have too “look through” trade war inflation to do so and the market expects just that:

Advertisement

If the Fed cuts then obviously it will pressure the USD downwards and the Australian dollar upwards. But I still can’t see a cut before markets really break down on trade war pressures. So the time to position for any round of AUD strength (however brief) would be as equities break lower as the trade war blows back into US earnings. Oil and junk debt are the leading indicators.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.