By Chris Becker

Stock markets were a little calmer overnight as the US GDP print came in strong as expected, although revised a little lower. The big mover was DOE oil inventories which were much larger than expected, sending crude prices at least 4% lower. The USD remained firm against the majors as the Australian dollar finally slipped back down to the 69 cent level.

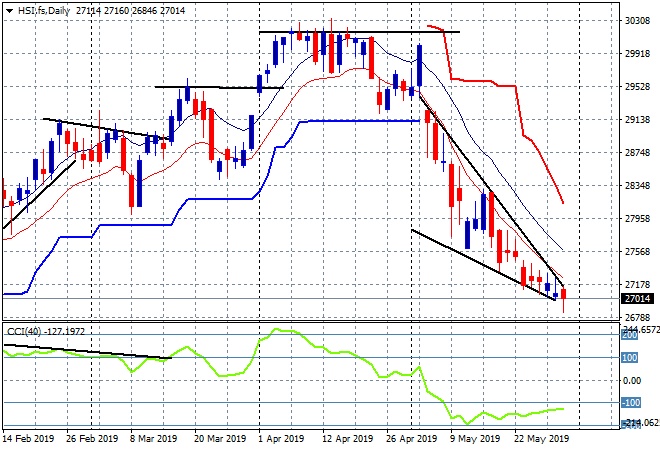

Yesterday saw Asian stock markets all close lower with the Shanghai Composite down 0.3% but still clinging above 2900 points, while the Hang Seng Index finished 0.4% lower to 27133 points, unable to arrest the recent decline. The daily chart still shows a deceleration pattern with a target at the 27000 point level but sentiment and momentum remains against this market:

Advertisement