So far its been a neutral day for risk markets here in Asia as traders weigh up the potential volatility around the ongoing trade war between the US and China while locally a slew of bad economic news has firmed expectations of a rate cut by the RBA as the Australian dollar remains depressed agianst USD.

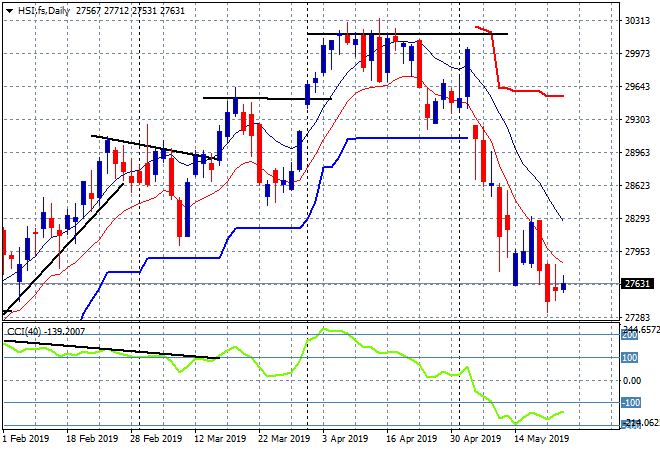

The Shanghai Composite is treading water slightly above 2900 points, currently down just a few points, while the Hang Seng Index is doing a bit better, up 0.3% to 27740 points finally not making another new daily low and getting a little bit of confidence back:

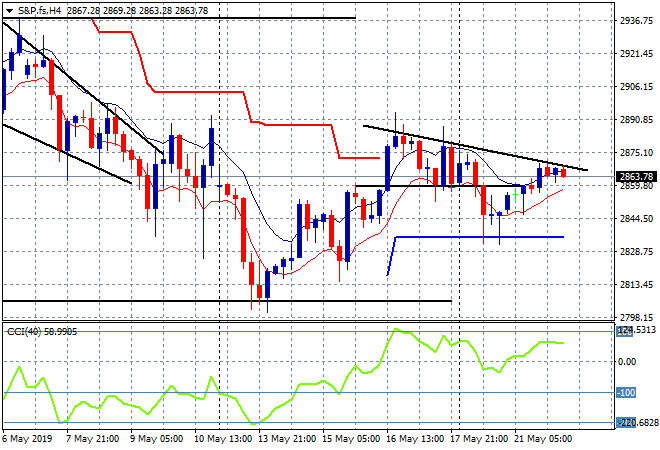

US and Eurostoxx futures are flat lined here with the four hourly chart of the S&P500 chart showing a desire to get back above last Friday’s high but so far, no new highs is weighing down this market, wheret he upside target is at 2870 or so:

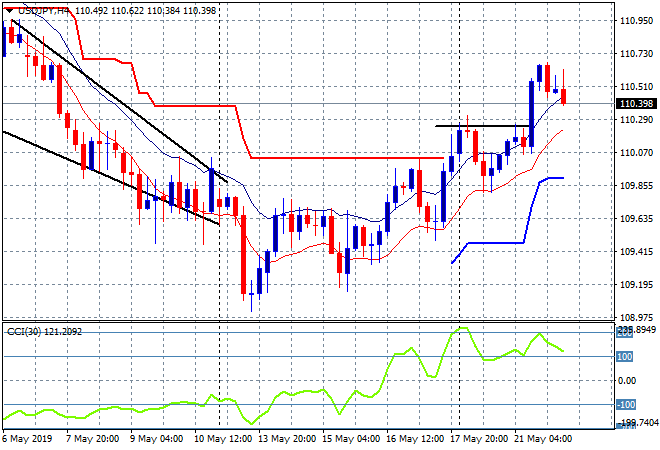

Japanese share markets are up slightly despite a firmer Yen, with the Nikkei 225 currently up 0.3% to 21337 points while the broader TOPIX is treading water. The USDJPY pair has failed to make a new high since last night’s session which was overcooked after the recent breakout above the 110 handle and could retrace there tonight if risk sentiment doesn’t improve:

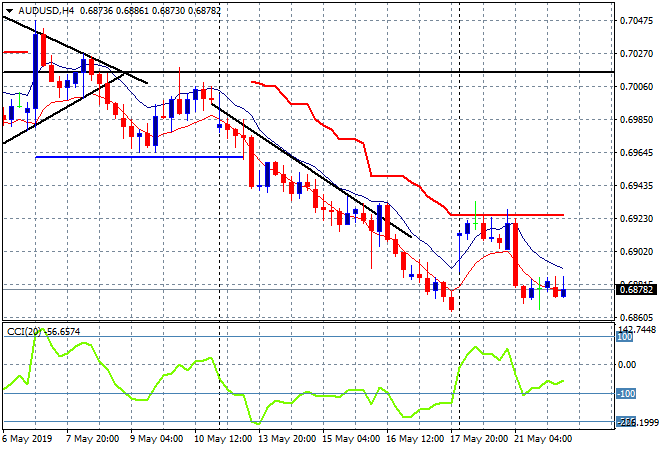

Australian stocks are also treading water, with the ASX200 still above the 6500 point barrier, but only advancing a few points. The Australian dollar looks to have already priced in the next rat cut, not reacting against the very poor construction numbers this morning, but watch the recent series of session lows which could break tonight:

The economic calendar is packed tonight with central bank catalysts including speeches by President Mario Draghi at the ECB and then the release of the latest FOMC Minutes. There’s also the April UK CPI print and another DOE oil inventory report.