The bounce continues here in Asia with stocks up across the board while currency markets are steady as the USD firms. The trifecta of Chinese internal economic releases came in lower than expected but this was overshadowed by the PBOC cutting the Yuan fix again to its lowest point since January, as the trade war of words settles down. Until tonight at least!

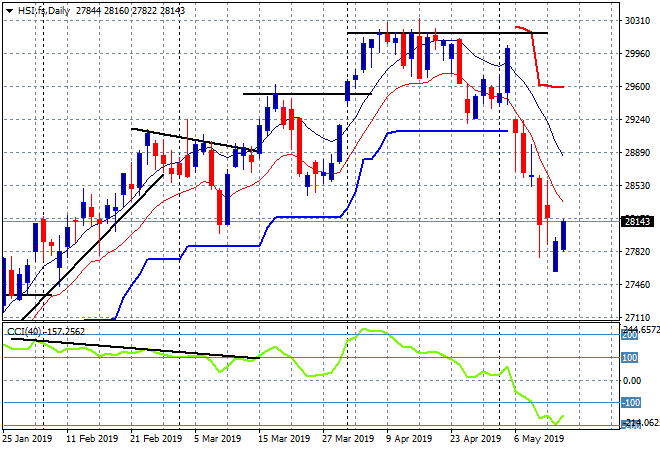

The Shanghai Composite has bounced the strongest, lifting over 2% higher to close back above 2900 points again, currently at 2943 points. In Hong Kong, the Hang Seng Index has continued it owns little relief rally to be up just over 1% to 28433 points. Momentum was clearly way oversold and is coming back to a swing play but there’s a lot of daylight overhead to fill:

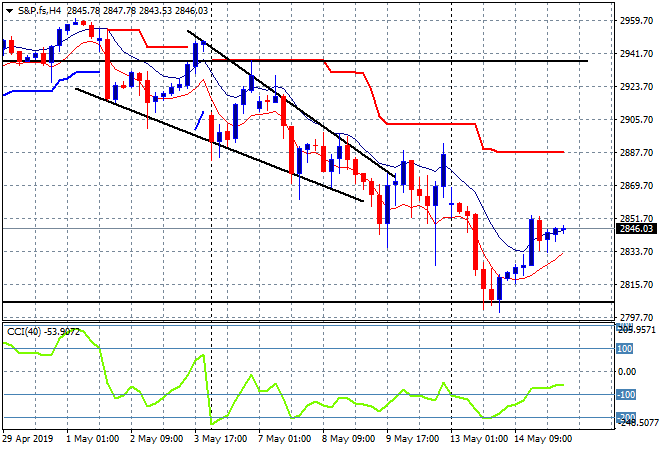

US and Eurostoxx futures are lifting on the back of the Asian rally with both up around 0.3% with the four hourly S&P500 chart showing an inclination to swing higher, but trailing resistance at 2890 points maybe too far a hurdle:

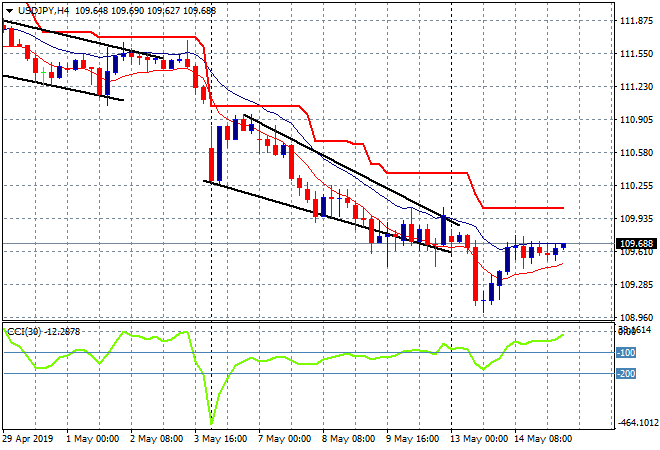

Japanese share markets came back fairly strongly as Yen didn’t provide as much as a headwind, with the Nikkei 225 closing 0.5% higher at 21188 points. The USDJPY pair has remained steady at the 109.70 level for over a day now and is poised to clear higher:

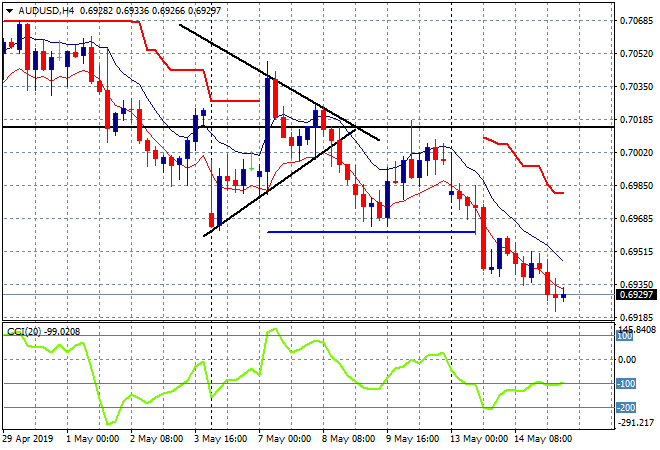

Australian stocks have done well, not quite catching up yesterday’s losses but close with the ASX200 lifting 0.7% to be at 6284 points. The Australian dollar has helped due to its own depressive mood, falling again to another new low and threatening the 69 cent handle:

The economic calendar has several major releases tonight, first off being German GDP then the EZ wide print for the first quarter. Next its US advanced retail sales for April and the latest DOE oil inventory report.