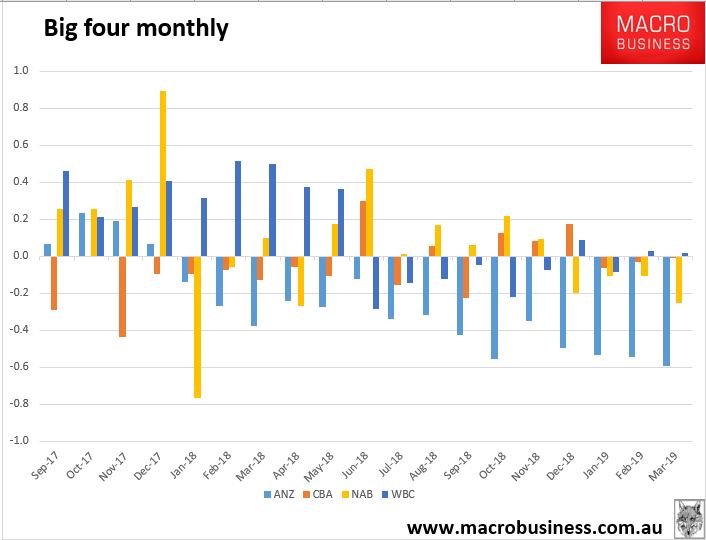

First, ANZ’s mortgage book is literally disappearing, as I noted yesterday vis investor loans:

Second, it is sinking below the water much faster than the RBA said that it should:

ANZ Banking Group chief executive Shayne Elliott is concerned about a spike in customers struggling to repay their mortgages, warning “stubbornly low” wage growth in a weakening housing market could prompt more defaults.