Big miners are splitting between bulks and the rest:

Advertisement

EM stocks were smashed:

Junk held on:

Treasuries sold:

Advertisement

Bunds were bought:

Aussie bonds too:

Stocks sold moderately:

Advertisement

Data on the night was positive with good US consumer confidence and OK European data.

But all eyes remain on the trade war, which is not going well as both sides ready themselves for an all-out brawl. The US has eased tensions with Europe and NAFTA partners as it focuses on China. And the Communist Party of China (CPC) is bleating through its media foghorn:

Huawei is not only strong but wise, sober-minded and tenacious. Cutting off supplies from the US will not defeat Huawei, which has long been preparing for the dark moment. On the contrary, Huawei will start getting even stronger.

Huawei is the symbol of China’s ability to do independent research. As a private company, it is the forerunner of China’s reform and opening-up. It has been deeply engaged in the development of global communications and become the leader of 5G technology. That Huawei will not lose to the US is significant for China’s response to the US’ strategic suppression.

The US has completely abandoned commercial principles and disregarded law. Its barbaric behavior against Huawei by resorting to administrative power can be viewed as a declaration of war on China in the economic and technological fields. It is time that the Chinese people throw away their illusions. Compromise will not lead to US goodwill.

We must dare to compete with evil characteristics embedded in the US. While sticking to opening-up, China should become good at countering the US.

In this fight against the US, we should abide by international rules and take into consideration the general trend of China’s reform and opening-up on the one hand. On the other hand, we should not be too gentle or worry about Western opinion. Any measure that can bite into the US and do no harm to China can be adopted.

Advertisement

This is very foolish. Embarking on economic war with the United States destroyed three tyrannies in the twentieth century. China is putting its hand up to be the first of the twenty first, via Bloomberg:

U.S. tariffs on Chinese products have already set in motion a profound shift in global supply chains that won’t be easily reversed. That threatens to accelerate the departure of manufacturers that already are reeling from rising labor and other costs.

Japanese office equipment maker Ricoh Co. said Thursday it is moving some production from China to Thailand to avoid trade war risks and Taiwan’s Kenda Rubber Industrial is investing in Vietnam for the same reason. Big consumer brands Samsonite International SA, Macy’s Inc. and Fossil Group Inc. have all said on recent calls with analysts that they are continuing to move production and sourcing out of China.

“Both foreign multi-national companies and Chinese private enterprises are more actively seeking alternative manufacturing bases,” said Klaus Baader, global chief economist at Societe Generale. “A lower trend growth in investment, coupled with more restricted access to foreign know-how, would mean permanent damage to long-term productivity growth.”

…Even worse may await should Trump add export tariffs or ban shipments of key technology components to China, especially semi-conductors, said Alicia Garcia Herrero, chief Asia-Pacific economist at Natixis SA in Hong Kong. That would strangle the Chinese economy, she says.

Altogether, an economic war with the U.S. “blows China up,” said Michael Every, head of Asia financial markets research at Rabobank in Hong Kong. “China would be cut off from Western markets, ideas, technology, and U.S. dollar-flow long, long before it’s ready to replace the U.S. for real.”

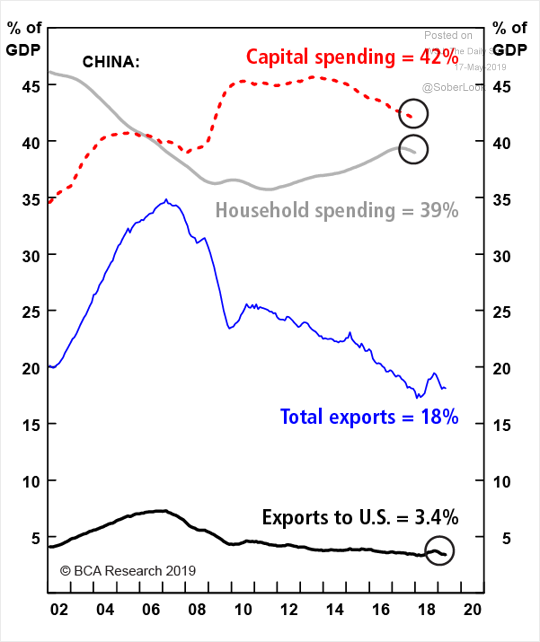

Exactly. We know China can respond by building more empty apartments but so what? That only accelerates China’s demise into the debt maw of the middle income trap, cut off from higher-income growth development options. Notice how in recent years, so-called Chinese rebalancing is now seeing both investment and consumption fall, via BCA research

Advertisement

Normally, in the short term, this would still be AUD bullish given more building means more Aussie dirt. And bulk commodities are tearing the roof off. It is very unusual for the AUD not to follow the Terms of Trade (ToT):

Advertisement

And, despite the risks longer term, the PBOC is signalling more building to come:

The People’s Bank of China warned that the escalating trade war could destabilize the global economy, and vowed to continue with its targeted stimulus policy at home.

“Trade friction and uncertainties in global policy could impact the global economy negatively” by driving up inflation, damaging household and corporate confidence and causing financial market turbulence, the PBOC said in its quarterly monetary policy report published late Friday.

But there are two very good reasons why the Australian dollar is breaking the mold this time. The first is that the link between resource wealth and the broader economy has been broken by two decades of atrocious policy making so Aussie interest rates are cratering even as national income booms, dragging the yield spread to the US to screaming sell territory for the AUD:

Advertisement

And the second reason is the conundrum faced by China on its own currency as it is forced to ease monetary policy again. Via FTAlphaville:

So what do the wonks at Deutsche reckon the catalyst is this time? Well, here’s their reasoning: Based on our recent trip to Beijing, we feel policymakers will be more agreeable to CNY depreciation now. First, Chinese policymakers appear more prepared for trade frictions and proactive in managing the growth fallout; growth is in better shape than last year, and the economy has responded to earlier stimulus. In 2018, when domestic data was poorer and there were fears of growth falling below 6.0%, a break above 7.00 was less acceptable, given risks of a negative feedback loop to an already weak economy. With the trade war likely to be protracted, finding ways of keeping domestic growth supported should be a priority for policymakers. This is likely to require looser monetary policy, which could come at the cost of a weaker currency.Authorities should be more willing to bear that cost this time.

Second, concerns over the “externalities” to currency weakness — hot money outflows and corporate stress seem more limited this time. Regulators appear more confident that years of regulatory measures will keep hot money outflows manageable. Corporates are now better hedged against FX weakness, and industrial profitability has been stronger, reducing concerns about the corporate balance sheet impact from a weaker CNY. Importantly, we have noted that CNY has been reacting predictably to the imposition of tariffs over the past year, with the move higher in USD/CNY proportional to the weighted average tariff being borne by Chinese exports to the US. The latest increase in tariffs to 25% on $200bn of goods is consistent with USD/CNY close to 7.10. If Trump proceeds with tariffs on $300bn, even at an initial 10% rate, this could take USD/CNY to 7.40.

Advertisement

So two interlinked reasons: stimulus from policymakers, in part due to the trade war putting pressure on growth.

The latter argument is accompanied by this excellent chart, that matches the weighted average of Trumps tariffs versus the renminbi:

And then there’s the question of corporate balance sheets. While a weakening renminbi might be okay for relatively debt-light technology companies like Tencent and Alibaba, it’s not so simple for the systemic real estate businesses.

Throw your mind back to this FT article from late April, on the dollar-denominated debt of the real estate giants, such as FT Alphaville favourite Evergrande, who had raised $6.6bn in debt this year, as of mid-April.

This chart for the whole market tells its own story;

Whether these companies will be happy with a weaker RMB remains to be seen. A UBS note, out Thursday, in particular, was dour on China’s real estate market going forward:

Real estate fundamentals are weakening amid decelerating economic growth, but the government dialled back its deleveraging efforts and is enabling more relaxed monetary conditions . . .[and] Fully let properties in liquid markets are being exchanged at yields below financing costs. This poses a greater risk, as room for capital appreciation is limited given the sluggish economic outlook. Investors should be aware of city-specific policies.

Higher dollar financing costs for the providers of these assets, who also hold a lot of them on balance sheet as investment properties, probably won’t be of much help with yields already slipping below financing costs.

But it feels like the same old story with China. Investors point to deteriorating fundamentals but then, without fail, the can manages to get kicked down the road. Somehow. However with Trump, rather than local authorities, now available to blame for the economic slowdown, perhaps there’s never been a more opportune time for the People’s Republic to let the renminbi slip past 7.

In short, it will be difficult for China to stimulate growth at all and the direct consequence of doing so is a materially lower CNY.

Advertisement

That, in turn, is a nightmare scenario for EMs worldwide as China turns from stealing DM production to EM, and the USD firms at the same time draining them of capital.

I don’t think that this scenario is sustainable for very long. For me it most likely ends in another big stock market accident as weakness in EM growth feeds back into oil and other commodities (though there will be some offset in China losing supply chains). At a certain point that feeds back from the margin to the centre as US profits also get hit and Fed is forced to cut, eventually sinking the USD (and lifting CNY and AUD), though nor necessarily before we see a global recession nor, for that matter, a soaring USD.

But today’s point is simply that we’re not there yet anyway. For now, while China foolishly fights the greatest economic power the world has ever seen, and its currency falls as a result, so will the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.