DXY looks very bullish as EUR and CNY sink:

The Australian dollar held on by its finger nails versus DMs:

But is still being left behind by EMs:

Gold confirms DXY firmness:

Oil was belted:

Metals too:

Miners were hit, GLEN broke:

EM stocks were OK:

So was junk:

Helped by a big Treasury bid:

And bund bid:

Aussie bonds roared to all-time record highs:

As stocks eroded:

Westpac has the warp:

Event Wrap

The FOMC minutes for their May 1-2 meeting showed there was widespread agreement that the recent dip in PCE inflation was likely “transitory”, and the commitment to a patient approach remains strong, with that stance likely to be appropriate “for some time” even if global conditions continued to improve.

Fedspeakers generally espoused a patient and balanced stance, NY Fed President Williams noted that he doesn’t see any strong arguments to move interest rates, “one way or the other,” Boston Fed President Rosengren said he sees, “no clarion call,” to raise interest rates any time soon. St Louis Fed President Bullard didn’t rule out a cut later this year if inflation continued to disappoint.

UK inflation data for April proved to be mixed around market expectations. Although RPI rose to 3.0%y/y (vs est. 2.8%y/y), the rise was due to fuel and holiday prices. Core CPI at 1.8%y/y and headline CPI at 2.1%y/y both undershot market estimates (1.9%y/y and 2.2%y/y).

UK markets continued to focus on the potential of an imminent forced or cajoled resignation of PM May given the increased lack of support for her latest version of the Withdrawal Agreement Bill (WAB).Event Outlook

NZ: Finance Minister Robertson gives the pre-Budget speech today, with potential for signals about the 30 May Budget.

Germany: May IFO business survey is released.

Euro Area: ECB President Draghi participates at the G30 meeting in Spain.

US: Apr new home sales are expected to fall back 2.5% after a 4.5% gain in Mar. Fedspeak involves Kaplan,

Daly, Bostic and Barkin on a panel.

Fed minutes were released and Phil Lowe appears to have taken over with “patience” now the key:

Participants discussed the potential policy implications of continued low inflation readings. Many participants viewed the recent dip in PCE inflation as likely to be transitory, and participants generally anticipated that a patient approach to policy adjustments was likely to be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective. Several participants also judged that patience in adjusting policy was consistent with the Committee’s balanced approach to achieving its objectives in current circumstances in which resource utilization appeared to be high while inflation continued to run below the Committee’s symmetric 2 percent objective. However, a few participants noted that if the economy evolved as they expected, the Committee would likely need to firm the stance of monetary policy to sustain the economic expansion and keep inflation at levels consistent with the Committee’s objective, or that the Committee would need to be attentive to the possibility that inflation pressures could build quickly in an environment of tight resource utilization. In contrast, a few other participants observed that subdued inflation coupled with real wage gains roughly in line with productivity growth might indicate that resource utilization was not as high as the recent low readings of the unemployment rate by themselves would suggest. Several participants commented that if inflation did not show signs of moving up over coming quarters, there was a risk that inflation expectations could become anchored at levels below those consistent with the Committee’s symmetric 2 percent objective—a development that could make it more difficult to achieve the 2 percent inflation objective on a sustainable basis over the longer run. Participants emphasized that their monetary policy decisions would continue to depend on their assessments of the economic outlook and risks to the outlook, as informed by a wide range of data.

In their consideration of the economic outlook, members noted that financial conditions had improved since the turn of the year, and many uncertainties affecting the U.S. and global economic outlooks had receded, though some risks remained. Despite solid economic growth and a strong labor market, inflation pressures remained muted. Members continued to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes for the U.S. economy. In light of global economic and financial developments and muted inflation pressures, members concurred that the Committee could be patient as it determined what future adjustments to the target range for the federal funds rate may be appropriate to support those outcomes.

After assessing current conditions and the outlook for economic activity, the labor market, and inflation, members decided to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent. Members agreed that in determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee would assess realized and expected economic conditions relative to the Committee’s maximum-employment and symmetric 2 percent inflation objectives. They reiterated that this assessment would take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. More generally, members noted that decisions regarding near-term adjustments of the stance of monetary policy would appropriately remain dependent on the evolution of the outlook as informed by incoming data.

Members observed that a patient approach to determining future adjustments to the target range for the federal funds rate would likely remain appropriate for some time, especially in an environment of moderate economic growth and muted inflation pressures, even if global economic and financial conditions continued to improve.

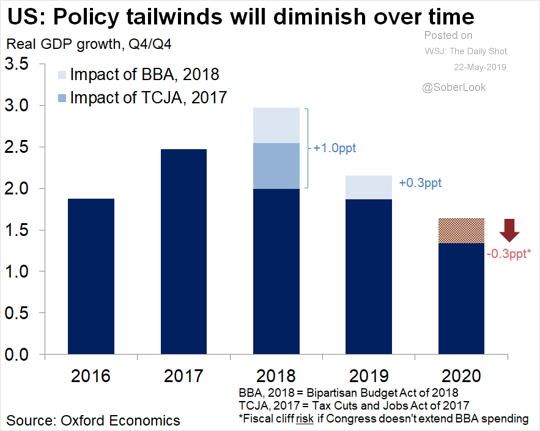

I am beginning to think that rate cuts may not be that far away. Although growth, employment and wages are still solid, the fiscal cliff ahead will challenge the US:

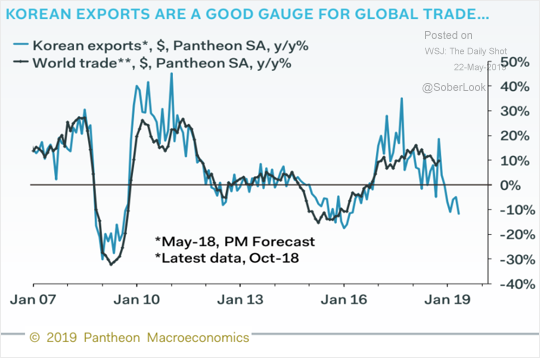

Especially amid a trade war that is still slowing global trade and growth and looks likely to drag it towards the 2% considered a global recession:

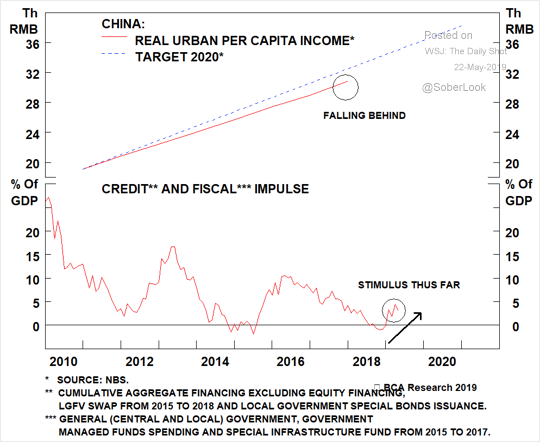

China is struggling to stimulate, as we can see in metals:

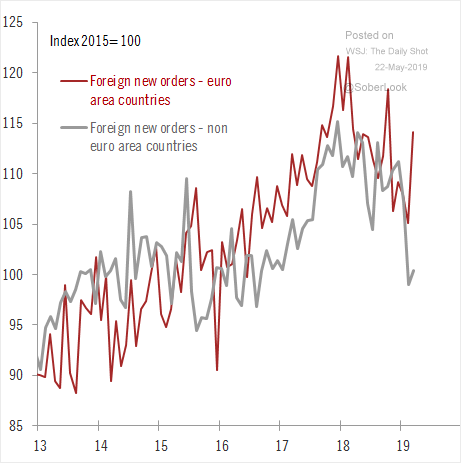

That leaves Europe buggered:

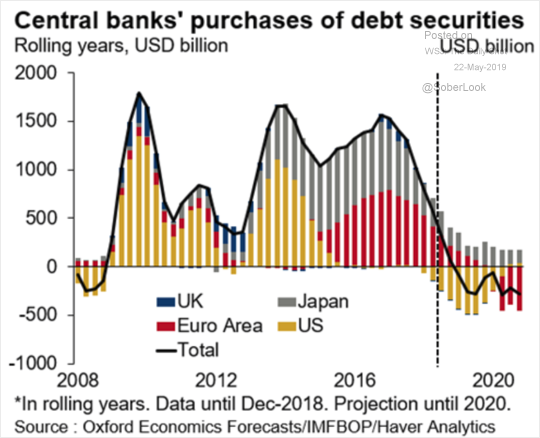

And in this environment, can the Fed (or anyone else) really be withdrawing liquidity?

I mean, seriously? Looks to me like we’re on the verge of another round of global central capitulation.

The key will be oil, as usual. If global growth slows enough to upset the oil market, and it looks like it is, then junk debt and stocks will be right on its tail. So there is still downside ahead for the AUD.

If the Fed leads off another round of easing then that would lift the AUD but not for long because everyone else will follow, most especially China. And they’ll do MOAR.

David Llewellyn-Smith is Chief Strategist at the Macrobusiness Fund and MacroBusines Super, which is long international stocks to benefit from a falling AUD, so he definitely talking his book.