Down she goes, via Westpac:

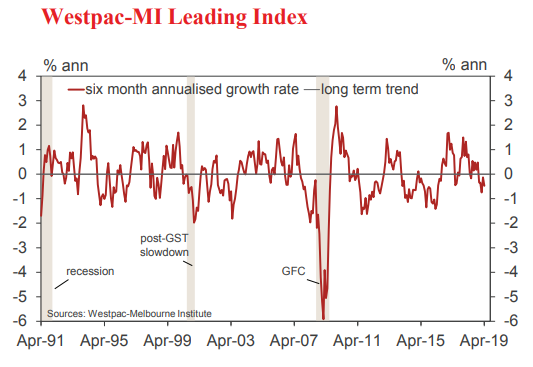

The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, declined from –0.13% in March to –0.47% in April.

The Index growth rate has been consistently negative over the last five months, a clear signal that economic growth through the three quarters of 2019 is likely to be below trend.

As noted last month, the improved signal in March was entirely due to a sharp lift in one component – dwelling approvals – which saw a spike in high rise activity drive a 19.1% surge. A 15.5% fall back in this component accounts for almost all – 0.32ppts out of 0.34ppts – of this month’s lapse in the Leading Index growth rate to more negative territory.

This consistent ‘below trend’ signal from the Index is in line with Westpac’s growth forecast for 2019 of 2.2%. We note that the Reserve Bank has recently lowered its growth forecast for 2019 from 3% to 2.6%. That adjustment is in the right direction and is official recognition that growth in 2019 will be below trend (generally accepted as around 2.75%).

The Index growth rate has swung sharply over the last six months, from +0.48% in November to –0.47% in April. Six of the eight components have driven the turnaround, led by a weaker pulse from US industrial production (–0.66ppts) and a narrowing yield spread (–0.25ppts) with drags from a levelling out in commodity prices (–0.14ppts); a softening in the Westpac-MI Unemployment Expectations index (–0.12ppts); dwelling approvals (–0.11ppts) and the Westpac-MI CSI Expectations Index (–0.11ppts).

The only significant offsetting positive has been from a sustained rally in the ASX 200, an 8.5% lift over the last six months adding +0.43ppts to the six month Leading Index growth rate. The contribution from the last component – aggregate monthly hours worked – has been unchanged.

The Reserve Bank Board next meets on June 4. On February 21 Westpac forecast that the RBA would cut the cash rate by 25 basis points at the August and November Board meetings.

Recently we have seen an even sharper than expected slowdown in inflation while prospects for the labour market have weakened. These disappointing outcomes culminated in a speech from the Reserve Bank Governor on May 21 where he appears to have committed to a rate cut at the June meeting.

Consistent with our original view, that there will be two cuts in this cycle, we have moved forward our rate cut timetable from August and November to June and August.

This is a little earlier than we expected back in February but we are pleased that we have been able to provide our customers with a consistent rate cut theme for most of this year.