DXY has broken out and is flying as EUR and CNY cop it:

AUD has been mauled versus DMs and the technicals are ugly with a bearish descending triangle right at breaking point:

It is mixed against EMs:

Gold is under pressure but doing OK all things considered:

Oil has flamed out:

Metals are not bullish China suddenly:

Nor miners though they lifted last night:

EM stocks have turned cold:

But junk is OK:

Treasuries sold:

Bunds were bought:

Aussie bonds have given back a little post-CPI:

And stocks are relentless:

So, my short term Aussie dollar bullish call has turned pear-shaped. The violence of the selling post-CPI is now being compounded by jitters around Chinese stimulus as the Poliburo failed to endorse endless debt (though did enough to signal it is still forthcoming in my view) and the PBOC hinted at no more RRR-cuts, via Reuters:

China’s central bank is likely to pause to assess economic conditions before making any further moves to ease lenders’ reserve requirements, after better-than-expected growth data reduced the urgency for action, policy insiders said.

Although the central bank’s easing bias remains unchanged, it sees less room this year for cutting reserve requirement ratios (RRRs) – the share of cash banks must hold as reserves – as fiscal stimulus plays a bigger role in spurring growth, according to government advisers involved in internal policy discussions.

The People’s Bank of China (PBOC) is also worried that pumping too much cash into the economy could reignite bubbles over time, the policy insiders said, and wants to save some of its policy ammunition.

“In the short term, it’s not necessary to use RRR cuts to boost economic growth,” one policy adviser told Reuters. “Monetary policy should leave some room – if economic uncertainties rise or economic conditions deteriorate, the central bank could ease policy.”

Worried about bubbles and already a strong rebound? Both are a laugh. The entire economy is a bubble now and the Q1 rebound was pure data bullshit. Even so, there probably doesn’t need to be more cuts given the rate of growth in credit over Q1 but markets want MOAR or its no dice for now.

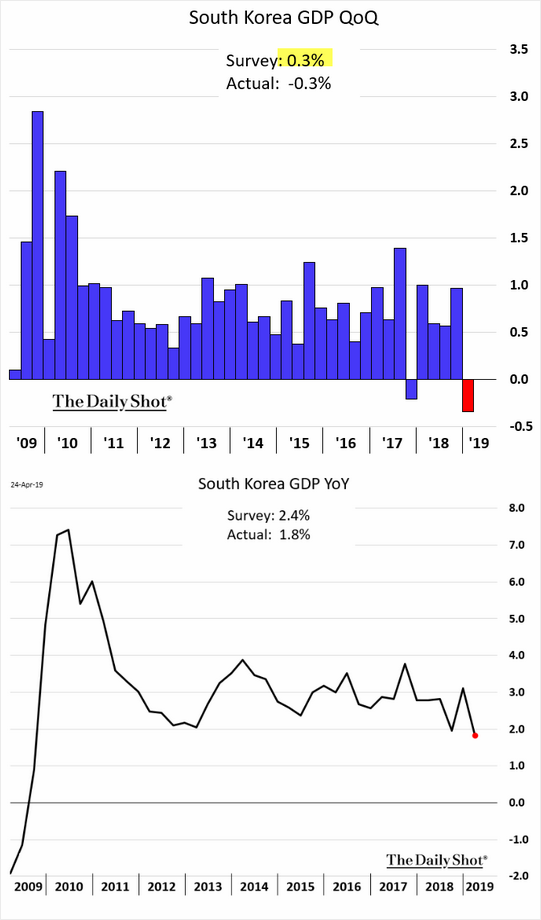

As for the rebound, tell that to the key China barometer in Korea:

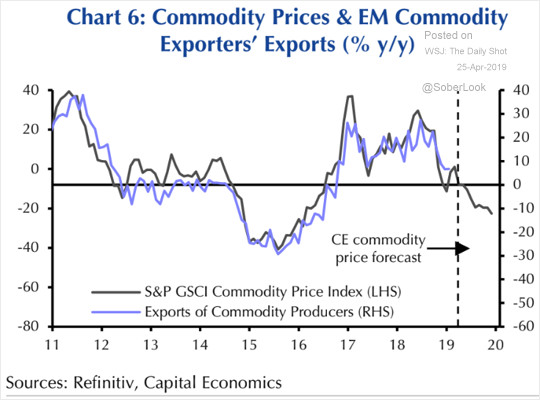

So long as China is doubt so are EMs and commodities:

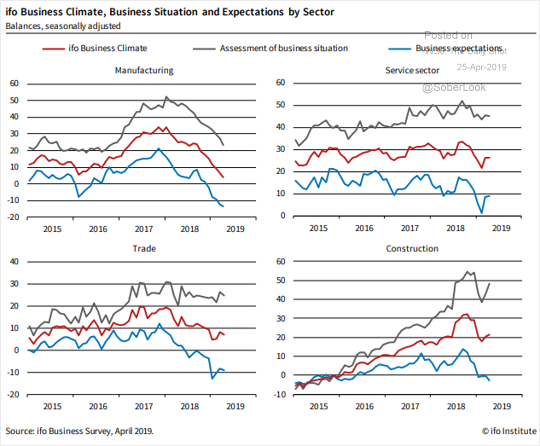

As well as any European rebound as the German IFO remained ugly:

The China rebound story is for H2 but it appears that is too long a wait for markets that are drunk on lowflation. Until China and the Europe see more life the US out-performance story holds sway and the Australian dollar falls.