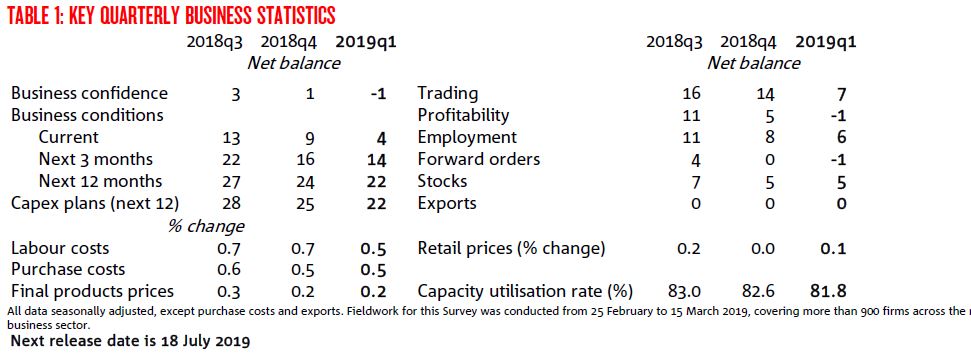

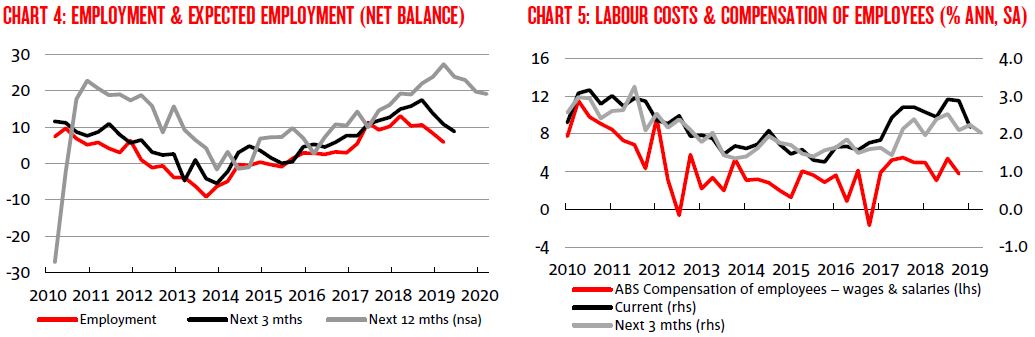

Both business conditions and confidence declined in the quarter. Conditions continued its downward trend since peaking in early 2018 and is now only just above average, suggesting the loss of momentum in the business sector has continued into early 2019. Confidence and forward orders turned negative in the quarter suggesting the outlook for conditions remains weak. The falls in trading and profits in Q1 were significant. Also, medium term expectations for conditions (3 and 12 months) and capital expenditure eased further. While the slowing in activity indicators continues unabated, attention has turned to the labour market (and the differences between activity and labour market indicators). In the Survey the decline in employment in Q1 (and expectations for Q2) were much more moderate and, in level terms, remain above average. Interestingly, firms reported that the difficulty in obtaining suitable labour edged lower – albeit it remains at elevated levels. Labour costs growth – a wage bill measure – edged lower also suggesting that wage pressure remains weak. Alongside the slowing in activity, the survey suggests that price pressures continue to track at a relatively subdued pace.

There’s lots more in the survey. The jobs outlook is falling near term but remains very strong long. Wages are fading:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.