DXY was up Friday night, CNY too, EUR down:

AUD was up anyway:

CFTC positioning remains very short at -53k contacts:

Gold held on:

Oil is breaking out:

Metals were firm:

Big miners flew:

EM stocks were also firm:

Junk was strong, especially US:

Treasuries were hosed:

The bund curve slumped:

Aussie bonds were still strong:

So were stocks:

Wrap from Westpac:

US personal incomes and spending both underwhelmed in the new year, underlining soft growth projections for Q1; Feb incomes rose a smaller than expected 0.2% (est: +0.3%) while Jan spending rose just 0.1% (est: +0.3%). The Fed’s preferred inflation gauge, the core CPE deflator rose a lower than expected 0.1% in Jan, sending the annual pace to an eleven month low 1.8% from 2%.

Fed speakers included Quarles, who said further rate increase are need at some point but pausing now after some weak data is prudent; Kaplan, who said current monetary policy is around neutral; and Kashkari, who said that the Fed should take seriously the yield curve’s signal of slower growth ahead. White House economic adviser Kudlow said the Fed should cut by 50bp immediately.

PM May’s Brexit agreement was rejected in the House of Commons by a majority of 58 votes. The EU has called an emergency summit, and the UK now has until April 12 to present a viable alternative. Absent a deal, the UK will need to leave the EU on April 12. The House of Commons will on Monday debate and vote on a further series of proposals to discover where consensus may lie.

China’s manufacturing PMI for Mar rebounded sharply, from 49.2 to 50.5, indicating policy stimulus may be having some effect.

Event Outlook

Australia: Mar NAB business survey is released with conditions having trended down from the latter part of 2018. Mar CoreLogic home price index is expected to continue to show declines.

Euro Area: Mar CPI and Feb unemployment is released. National releases have shown a still lack of price pressure but with continuing reduction in slack in the labour market.

US: Feb retail sales are released and will be in greater focus after the sharp drop in Dec was followed by a partial rebound in Jan. Mar ISM manufacturing index is anticipated to hold around 54, a still solid pace of expansion in contrast to PMI weakness in Europe, and subdued reads in China and across east Asia. Feb construction spending is released.

Final Markit manufacturing PMI’s are released for Japan, the Euro Area and the US.

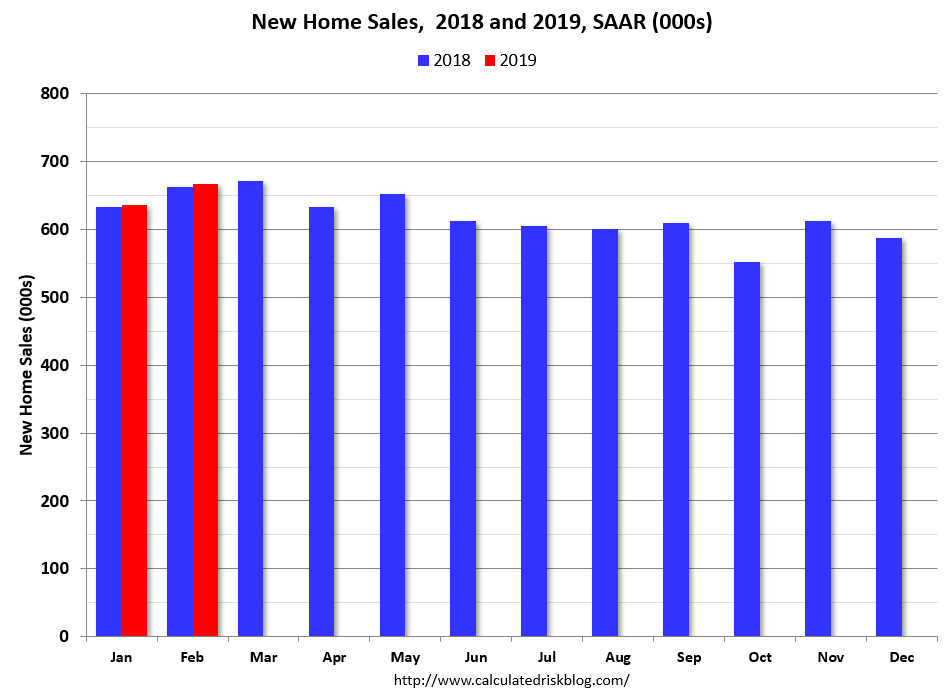

Friday night trade was lifted by the bullish comments of Li Kequiang Friday which will was followed by the rebounding PMI Sunday. As well, US data was good with new home sale strong:

I continue to think that US worries are over-egged. A slowdown certainly but no recession. Not, at least, without an external trigger.

So, what is the driver of the global slump then? Gavekal has a go at that:

Scenario #1: There is no brake

The first possibility—contrary to what we’ve suggested above—is that there is nothing acting as a brake on the global economy, and that the recent softness in the data is just noise. To some extent, this is the message being sent by global equity markets, which have continued to rally in the face of weaker economic data and earnings downgrades.

Scenario #2: The brake is politics

A second possible reason why global activity is slowing despite the absence of the usual “brakes” is that this time around the global economy is evolving in a much more uncertain environment. Over the past year, the typical corporate CEO has had to face up to: 1) Fears of a global trade war centered on the US-China relationship, but which could quickly escalate to encompass the US-Europe relationship, 2) Renewed fears about Europe’s structural integrity following the formation of the populist Five Star and Lega coalition in Italy, 3) Brexit uncertainty, 4) A flare up in tensions between India and Pakistan, which brought the two nuclear-armed countries perilously close to war, 5) And the far-fetched accusation in Washington DC the US president was actually a Manchurian candidate in the pocket of Vladimir Putin. Against this backdrop, it would be no great surprise if companies delayed major investment decisions, causing growth to slow.

Scenario #3: The brake is industry-specific headwinds

…in China (as in a number of other countries), auto sales and smartphone sales have been disappointing. One question for investors is whether this weakness is cyclical (but why would it be at a time of low interest rates and low unemployment?) or structural. There is some evidence for the latter. When it comes to cars, it seems that in some countries, millennials are no longer passing their driving tests in the same numbers as their parents (choosing to use ridesharing apps instead). Meanwhile, older drivers may be holding back from purchases out of a fear that today’s cars will turn out to be as valuable as a Ford Pinto when a new generation of electric/hybrid/self-driving cars is rolled out in the coming years. Meanwhile, on the smartphone side, the lack of new killer features means that the latest models are essentially the same as three-year old smartphones. Sure, the cameras are better, and the screens display colors more sharply, but as the sales figures indicate, these incremental improvements aren’t enough to persuade consumers to dig deep into their pockets. In short, we are living in a world where (i) the auto industry is struggling with some significant headwinds that could last for years to come, and (ii) the tech sector hasn’t brought out a must-have killer new product for several years. Given the size and importance of these two industries, maybe their respective slowdowns help explain the unfolding global slowdown.

Scenario #4: We are entering a secondary depression In the deflationary 19th century, economists often spoke of “secondary depressions”. Back then, the driver of the economy—more than consumption— was capital spending. This was never more true than during the railway boom of the 1870s. As railroads were built, economies underwent a massive boom. The demand for steel, for cement, for copper, for coal simply soared. This demand lead to massive increases in capacity, in part because there was a “double” demand for many of these products.

Consider steel: first, there was enormous end-user demand for steel to build all the new machinery and infrastructure. Second, there was heavy demand for steel from the steel industry itself, which needed steel to build the steelmaking capacity to meet all the end-user demand. As a result, when end-user demand finally plateaued, or worse still started to go down, the steel industry found itself left with massive overcapacity. This led to a collapse in profits, to bankruptcies, and to economies falling out of bed. This was what economists of the time would call the “primary depression”.

Invariably, after the “liquidation phase” triggered by the primary depression, after some time (usually two to three years) the affected economies would find their footing, and markets would rally. Unfortunately, these rallies proved to be false dawns, as the realization set in that final demand for steel (or coal, or copper, or cement) was now in a structural decline. Activity then entered what 19th century economists called the “secondary depression”. On average, these lasted around 10 years. For example, the US entered into a primary depression in 1873, and only came out of its secondary depression in 1896.

Fast forward to today: in the last 20 years, China has gone through the biggest capital spending boom in history. As a result, shouldn’t we suspect that the “capital investment” industry might have overbuilt? Won’t China’s great investment boom repeat the “secondary depression” pattern? The lousy performance of eurozone banks hints at a deflationary bust. And shouldn’t we also worry that the countries that fed China’s capital spending boom and benefited from it—China itself, but also Germany, South Korea and maybe Australia—will now have to deal with the consequences of the roll-over in Chinese capital spending? With this in mind, could we be seeing the start of a primary depression in countries such as Germany? And if so, shouldn’t we be troubled that this slump is beginning when banks are already in a precarious position.

Scenario #5: As societies age, growth will remain lackluster

Economic growth is made up of productivity gains and population growth. Now, as everyone knows, population growth in most Western and East Asian countries, has either slowed to a trickle, or even moved into negative territory. This alone would account for a weaker growth environment. Less well understood is the effect that an aging population might have on an economy’s productivity growth.

Of course, both Charles and Anatole would argue that being in your 60s and 70s is the new 40. For some, that is undeniably true. Better diets, better medicine, and healthier lifestyles mean that baby boomers can remain productive members of society for far longer than their own parents did. But can the very large cohort of retiring baby boomers be as productive, or as entrepreneurial, or as creative, as people in their 20s, 30s, or 40s?

Anecdotal evidence would suggest “probably not”. Charles likes to point out that Sam Walton was 52 before he took Walmart public, and became anything more than a small local retailer. But, almost all of the corporate behemoths that are changing the face of business today—Google, Facebook, Amazon, Alibaba, Apple, Tencent, Microsoft, etc.—were founded by visionaries in their 20s, 30s or (at most) 40s.

Beyond the creative urges of an aging society, the bigger question may concern the allocation of resources in the aging, democratic societies of the West. Take the UK as an example. When he was first elected prime minister, David Cameron’s earliest policy moves were (i) to guarantee and boost state pensions, while (ii) simultaneously introducing tuition fees for university students, who until then had enjoyed free tertiary education. Obviously, the political calculus was that there were more votes to be won pandering to Britain’s aging voters than to its youth. Perhaps this calculus made sense politically… but economically?

So, was Cameron’s decision to invest in old people rather than the young a one-off? Or is it likely to become the norm as all Western democracies age?

You have go back to the height of the 1999-2000 tech bubble to find household equity holdings comparable with today’s. But since then, the population has got older, and it will get older even more quickly from here—the US now gains some 3mn people over 70 years old each year. This means that the ability of the final investor to withstand any kind of downward equity price shock is much lower than it was a couple of decades ago. Perhaps this helps to explain the recent weakness in US consumption data and overall US growth. The fourth quarter of 2018 delivered very poor equity market returns, and almost immediately consumption fell back, and the economic data promptly softened.

Putting all this together, we could conclude that (at least in the US) we live in a world where: 1) The federal government, and also state and local governments, have so much debt that it is almost impossible for the Fed to raise interest rates without triggering some serious fiscal policy problems. 2) Corporates have so much debt that when interest rates start to rise, an economic slowdown may not be far behind. 3) Individuals are getting older, and are so exposed to equities that their ability to withstand even a modest bear-market is limited. If all this is true, then—just as we have seen in Japan—the aging of our societies may mean that interest rates will have to stay low forever.

My take is that forces 4 and 5 are structural and inescapable. Along with wealth inequality, that leaves us in a state of lowflation and secular stagnation which makes the global economy more vulnerable to cyclical headwinds such as 3 and 4. Add that the US has tightened quite a lot for such a context and a material slowdown makes plenty of sense. Number 1 is the plaything of liquidity not fundamentals.

As said previously many times, Japan is now the playbook for the global economy which means that monetarism is, for all intents and purposes, dead. This is now Keynesian world in which unconventional monetary and fiscal stimulus plays the major role in cyclical ebbs and flows that never raise inflation beyond its knees before being knocked over again. As China slows into the 2020s, and its interest rates also fall to zero pressuring CNY, this will only get worse.

So, for the AUD, it remains a structurally weak period without end. Whether we’re about to see a rebound on a China credit-juiced rebound is up for grabs. The deep market short makes us ripe for rebound. But if we do it will be temporary. Even short term I can’t see it getting overly far given my view of any China rebound will be L-shaped at best.