DXY was firm last night as EUR eased:

AUD was strong anyway against DMs:

Mixed against EMs:

Gold sank:

Oil jumped again:

Metals fell:

And miners:

EM stocks are still poised for higher:

Junk was stable:

Treasuries sold:

And bunds:

The RBA has missed its window:

Stocks keep climbing:

Westpac has the wrap:

Event Wrap

US industrial production fell 0.1% in March, weaker than expected; capacity utilization edged down to 78.8% from 79%.

The National Association of Homebuilder’s sentiment survey increased slightly in April, to 63 from 62, led by a firming in the prospective buyers sub-index, likely attributable to lower mortgage rates fostered by the Fed’s patient stance.

The German ZEW expectations index rose to +3.1 in April, above expectations and its first positive reading in twelve months (i.e. optimists outnumber pessimists among respondents), supporting expectations for second-half rebound in Europe.

The GDT dairy auction resulted in little price movement in the main products – a 0.5% rise in prices overall, with whole milk powder down 0.7%, and skimmed milk powder up 0.2%. These results were in line with earlier futures market predictions.

Event Outlook

NZ: CPI is expected to rise 0.3% in the March quarter, for a 1.7% annual pace (down from 1.9% in Q4). Westpac and the RBNZ forecast 0.2% and 1.6%.

Australia: Mar Westpac-MI Leading Index is released.

China: Q1 GDP is expected to show the annual growth pace decelerate to 6.3% from 6.4%. The authorities’ growth target is a range of 6.0-6.5% for 2019 compared to the point target of 6.5% last year. Mar retail sales, industrial production and fixed asset investment will provide further information on the growth breakdown and momentum.

Euro Area: Feb trade balance is released and Mar CPI final is expected to confirm the flash read of 0.8% annual core inflation.

UK: Mar CPI is anticipated to show annual headline inflation edge up to 2.0% with core tracking at 1.9%.

US: Feb trade balance is expected to be a deficit of $53.5bn, slightly wider than Jan’s $51.1bn. The Federal Reserve Beige Book is released. Fedspeak involves Bullard at the Minsky conference and Harker in New Jersey.

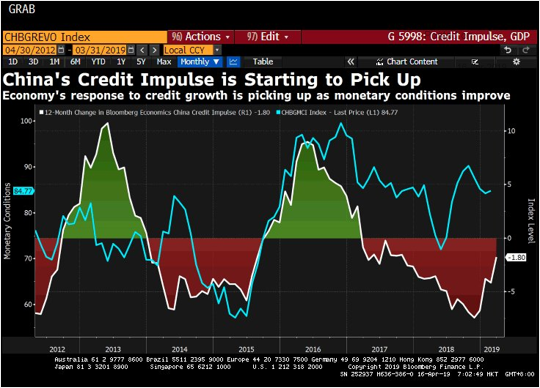

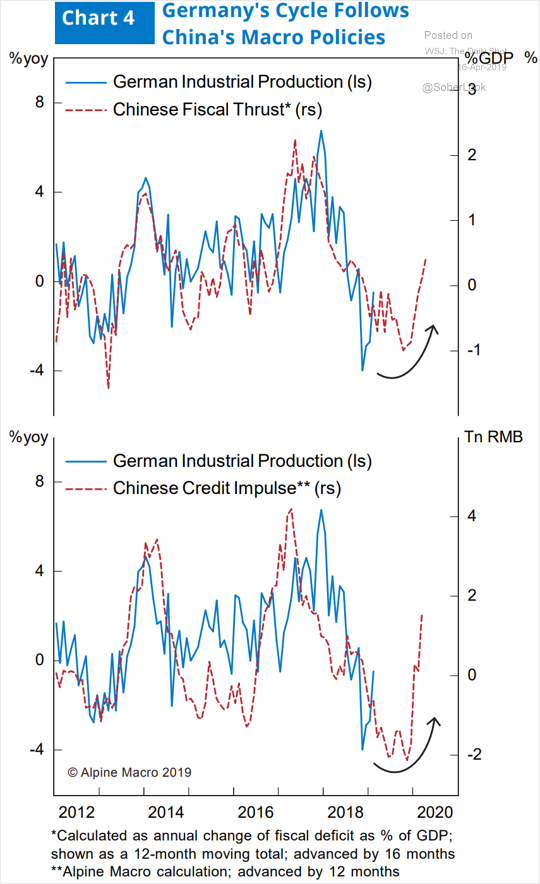

I have made a shift in my narrative. It is clear enough now that China has turned the credit tap on with enough force to produce a growth bounce:

The pulse appears strong enough to radiate outwards with the usual implications. That will be a lift in European and emerging market growth:

With the US still set to slow with its fiscal cliff, we’ll see a shift in global growth leadership for a while away from it. That should be enough to lift the CNY and EUR as DXY falls. That, in turn, boosts commodities and commodity currencies further, including the AUD.

I still don’t think that this will be strong enough to resemble 2016, nor give us a return the “global synchronised growth” chimera and the RBA is till going to cut. But it does appear strong enough for another late cycle tradable rally in risk, commodities and the AUD, as well as steepen the global bond curve for a while.

We have re-positioned accordingly.