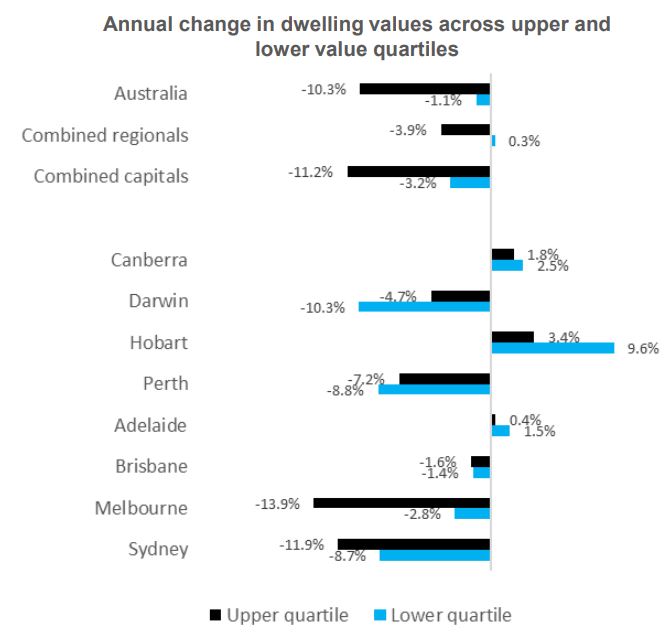

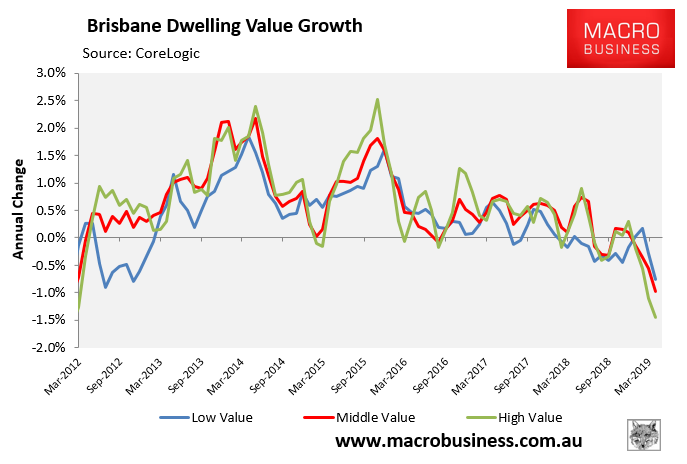

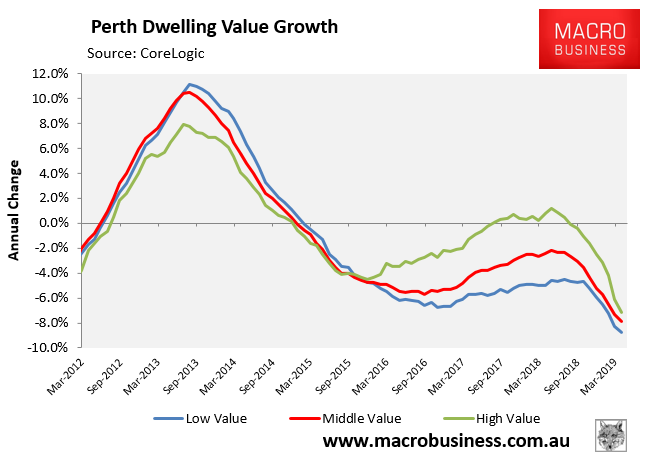

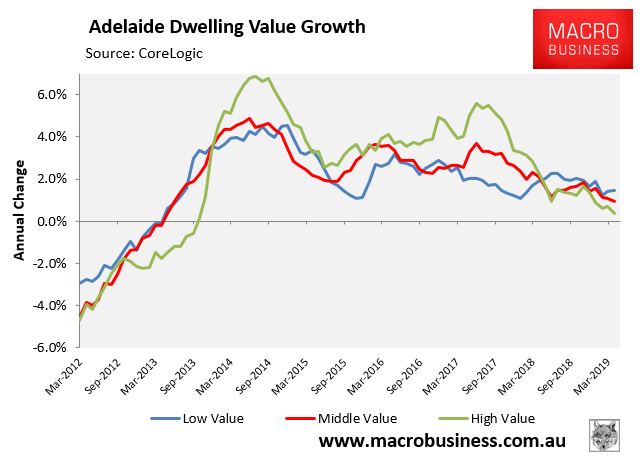

CoreLogic’s dwelling values results for March reported that losses have been driven by the premium end of the market, whereas values across the most affordable 25% segment have held up comparatively well:

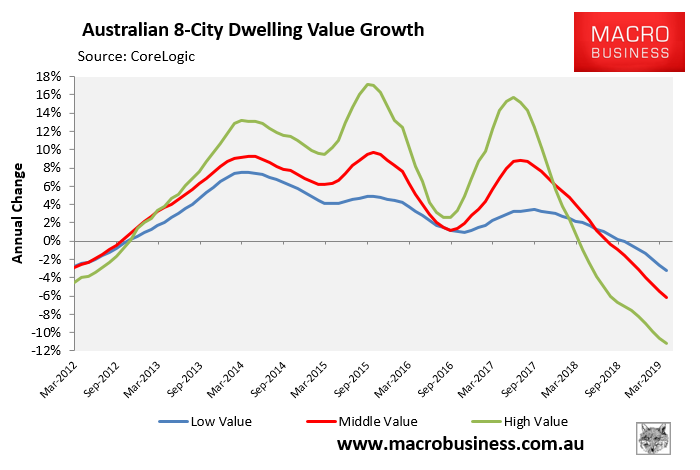

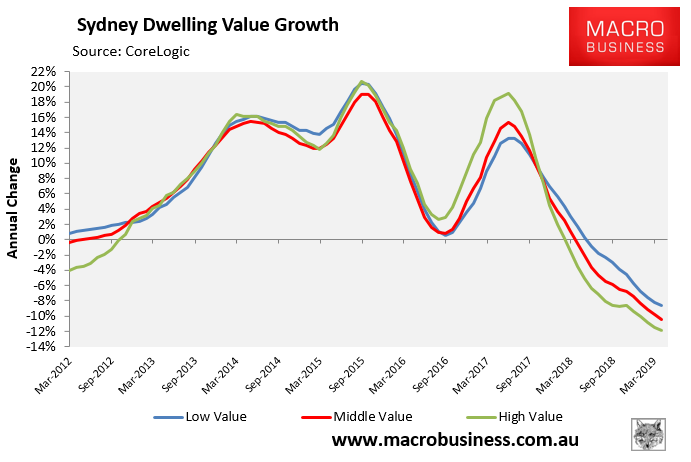

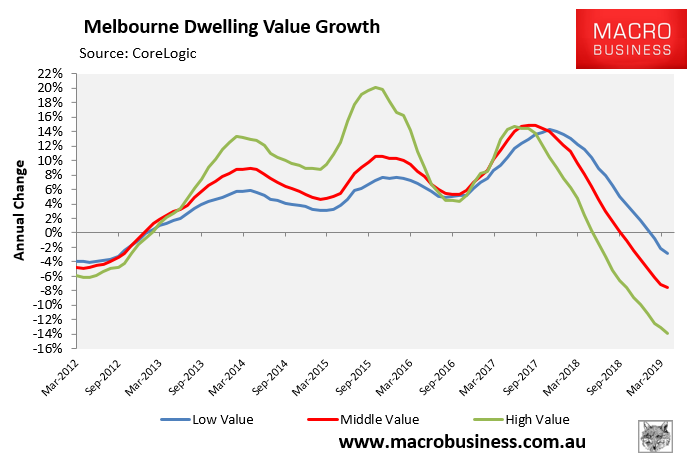

While this is true when viewed on an annual basis, growth rates are negative and trending down across virtually all price segments – low value (bottom 25%), middle value (middle 50%) and high value (top 25%):

Advertisement