DXY remains strong with CNY firm and EUR weak:

The Australian dollar was universally sold as RBA cuts firm and Budget stimulus was minor:

Gold is marking time:

Oil is up and away. This is DXY bullish given the signal it sends US shale:

Metals were soft:

Miners are in ecstasy:

EM stocks pulled back:

Junk firmed:

Treasuries too:

And bunds:

Aussie bonds were bid anew:

Stocks managed small gains:

Westpac has the wrap:

Event Wrap

The volatile US durable goods orders report showed a 1.6% decline in February, slightly less than expected, though the prior month was downwardly revised. Excluding volatile top-line items such as aircraft and defence equipment, the picture is flat: core capital goods orders fell a lesser 0.1% while core capital goods shipments were flat.

The GDT dairy auction resulted in an overall price gain of 0.8%, with whole milk powder down 1.3%, skimmed milk powder up 1.8%, and butter up 5.3%.

Event Outlook

Australia: Feb retail sales are expected to rise 0.3%. Westpac’s forecast is for a 0.1% decline, continuing the run of soft results with business surveys suggesting very difficult conditions in the retail sector. Feb trade balance is expected to be a $3.7bn surplus, down from Jan’s very strong $4.5bn. Westpac’s forecast is +$3.8bn as exports slip 0.9% with a decline in gold and coal partly offset by higher iron ore exports.Euro Area: Feb retail sales are expected to rise 0.3%, seeing the annual pace edge up to 2.3% from 2.2% in Jan.

US: Mar non-manufacturing ISM is released with the survey last at 59.7, indicating strong activity. Fedspeak involves Bostic in Washington, D.C.

Final Mar Markit Services PMI’s are released for China, the Euro Area and the US.

The Budget has mercifully done little damage with a little tax cut and nothing overly stupid. If anything it is on he conservative side for stimulus, firming the timetable for rate cuts. The AUD reflected these domestic forces last night and they remain a headwind. The bond market is yet to fully price cuts and yield spreads are going get much wider yet.

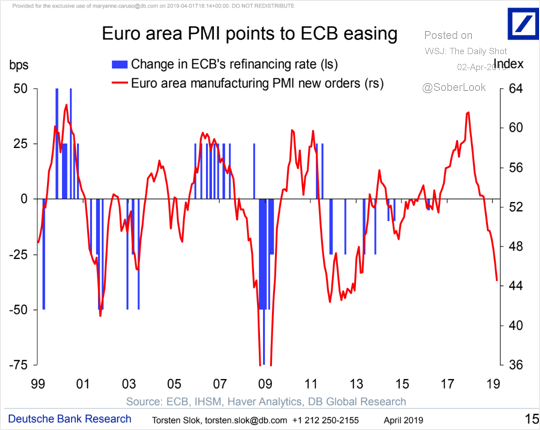

On the international front, European weakness remains entrenched, also AUD bearish. Manufacturing is weak:

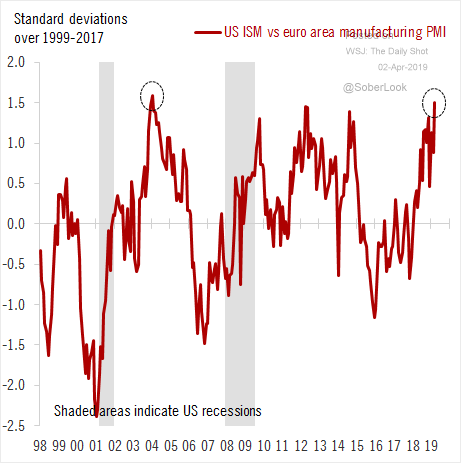

The comparison with the US is dire:

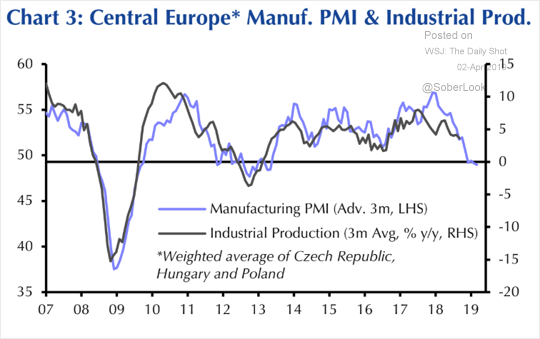

It’s still spreading:

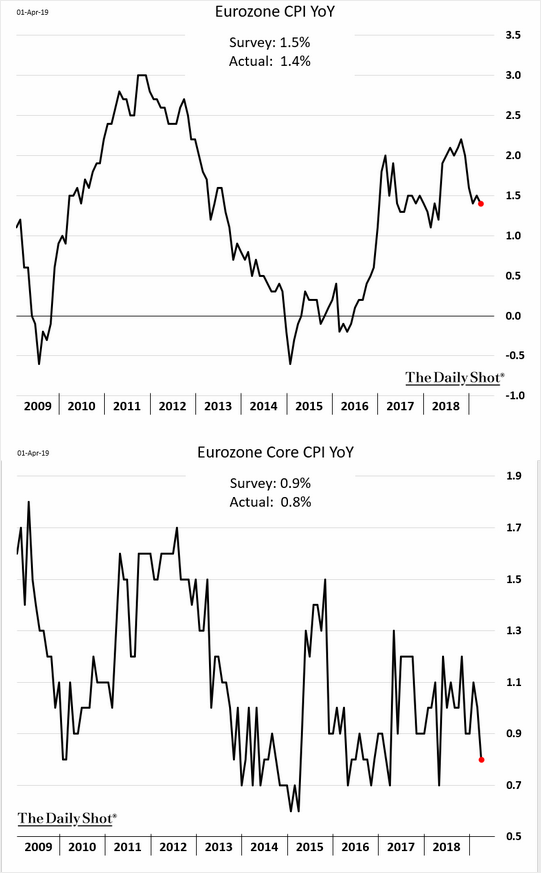

And lowflation won’t budge:

The bump in Chinese PMIs could signal a turn for German output but I remain skeptical it will last amid the trade downdraft. A weak EUR means a strong DXY means a weak AUD.

Both domestic and international forces still point the AUD lower.