What a difference a day makes. DXY was down, EUR and CNY up:

AUD was universally bought:

Gold struggled:

Advertisement

Oil too:

Metals did better:

Big miners continue the ascent to heaven:

Advertisement

EM stocks look poised for breakout:

Junk fell:

As did Treasuries:

Advertisement

And bunds:

Aussie bonds entered the woodshed:

Stocks soared on:

Advertisement

Westpac has the wrap:

Event Wrap

The US ISM services sector PMI printed on the low side of expectations at 56.1 (est: 58) from 59.7, an 18-month low though still consistent with reasonable growth momentum; new orders slipped but employment encouragingly held firm. The ADP survey of employment showed a lower than expected gain of 129k vs an upwardly revised 197k in the prior month, flagging a loss of hiring momentum though the track record of this report as a gauge of payrolls (due later this week) is an open question.

Markit’s services sector PMI for the Eurozone was revised higher for March, to 53.3 from a preliminary estimate of 52.7, a welcome uptick. Regionwide retail sales rose 0.4%, also stronger than expected, though the prior month was revised lower.

Event Outlook

Germany: Feb factory orders is released after the PMI signalled contraction in the manufacturing sector has worsened in 2019.

Euro Area: Mar ECB minutes will be examined for any indication on possible TLTRO-III incentives and members’ views on alleviating some of the burden of negative interest rates on banks (in relation to recent discussion on a tiered deposit rate).

US: Fedspeak involves Kashkari in North Dakota and Mester in Ohio.

US data was softish with the greater worry being the stalled ADP number:

Private sector employment increased by 129,000 jobs from February to March according to the March ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…“March posted the slowest employment increase in 18 months,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Although some service sectors showed continued strength, we saw weakness in the goods producing sector.”

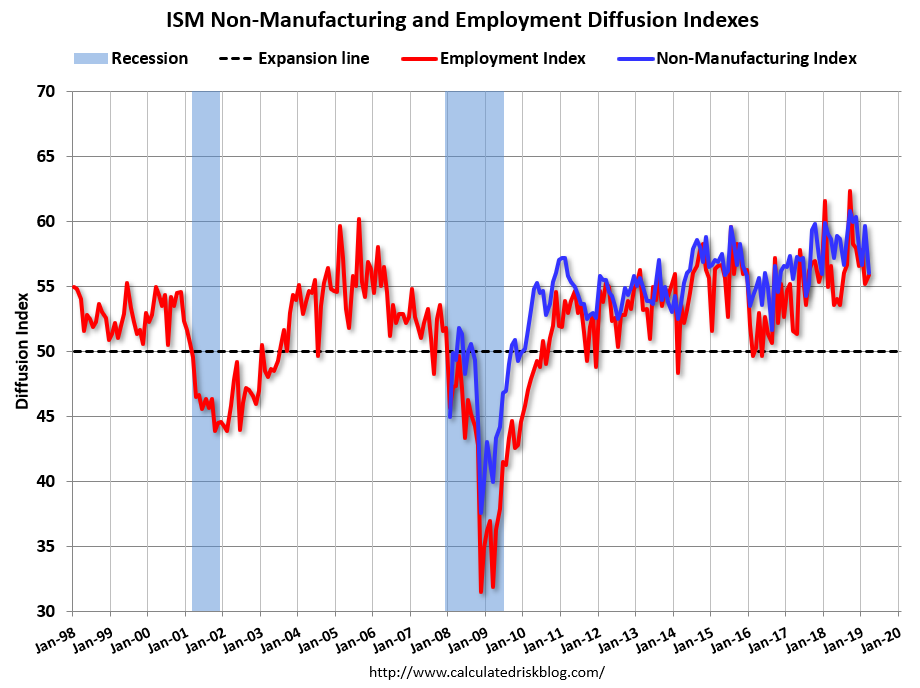

Too early to call that a trend and the ISM at 56 is still very good:

The NMI® registered 56.1 percent, which is 3.6 percentage points lower than the February reading of 59.7 percent. This represents continued growth in the non-manufacturing sector, at a slower rate. The Non-Manufacturing Business Activity Index decreased to 57.4 percent, 7.3 percentage points lower than the February reading of 64.7 percent, reflecting growth for the 116th consecutive month, at a slower rate in March. The New Orders Index registered 59 percent, 6.2 percentage points lower than the reading of 65.2 percent in February. The Employment Index increased 0.7 percentage point in March to 55.9 percent from the February reading of 55.2 percent. The Prices Index increased 4.3 percentage points from the February reading of 54.4 percent to 58.7 percent, indicating that prices increased in March for the 22nd consecutive month. According to the NMI®, 16 non-manufacturing industries reported growth. The non-manufacturing sector’s growth cooled off in March after strong growth in February. Respondents remain mostly optimistic about overall business conditions and the economy. They still have underlying concerns about employment resources and capacity constraints.”

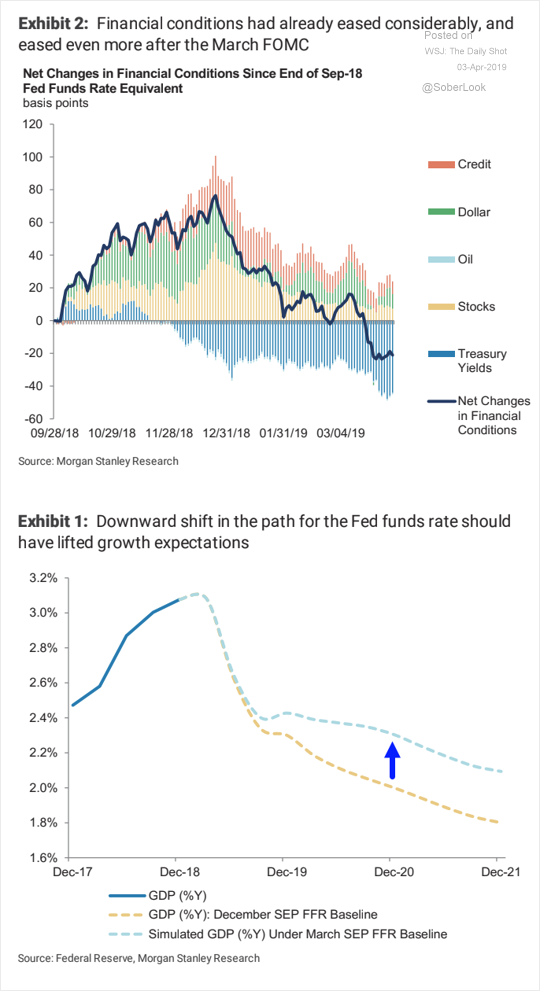

Meanwhile, financial conditions have already loosened a lot:

With mortgages surging:

I have long expected a US slowdown this year with the “fiscal cliff” and Fed tightening but it still looks well in hand. The US still has a better outlook that a China-dependent Europe though right now sentiment is pretty equal:

If China rebounds more strongly that I expect then so will EUR and AUD. If not, DXY remains in control and AUD weak. Still favour the latter.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.