And building nice little inflation shock within six months:

Advertisement

Base metals were soft:

Big miners too:

And EM stocks:

Advertisement

Plus junk:

Treasuries were sold:

Bunds bought:

Advertisement

And stocks firm:

Westpac has the wrap:

Event Wrap

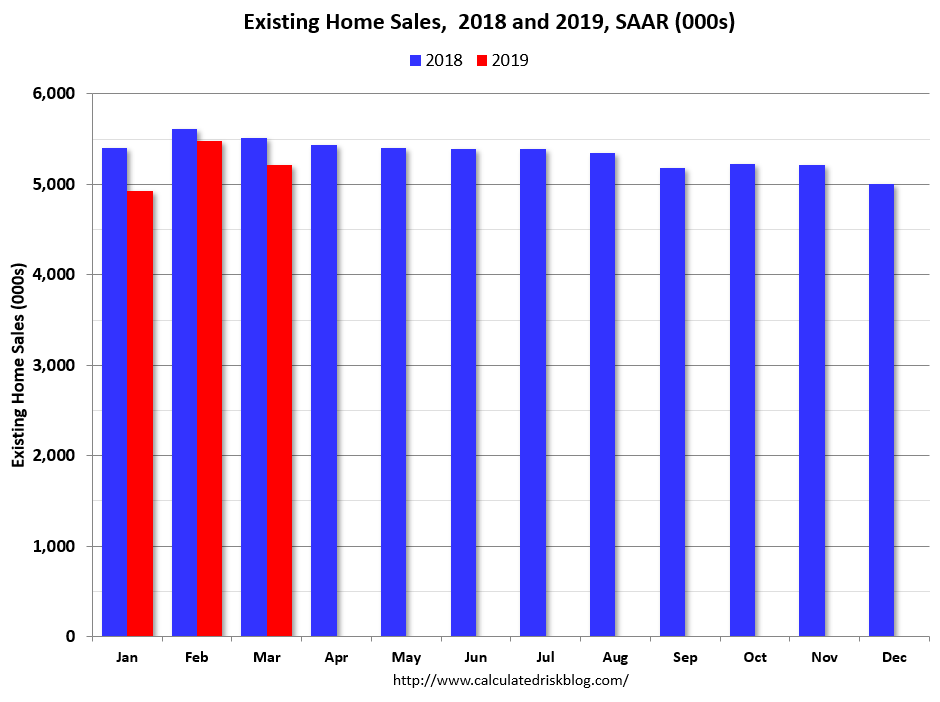

US existing home sales fell 4.9% in March, a steeper than expected decline, but that follows an outsized 11.2% increase in the prior month. US housing starts were also on the weaker side despite lower mortgage rates, slipping 0.3%, below expectations for a 5.4% gain.

Reuters reported that the United States demanded a cessation of Iranian oil exports to major importers, such as China and India, who had been granted exemptions from sanctions. Crude oil prices rose to six-month highs, in response, on fears the US action could restrict supply. Secretary of State Mike Pompeo, in a briefing on Monday, said the aim was to halt Iran’s exports entirely, as it continues to pressure Tehran to curtail its nuclear program, ballistic missile tests and support for conflicts in Syria and Yemen.

EventOutlook

NZ: Electronic retail spending has been growing at a 6%+ pace this year, with government stimulus benefitting households.

Euro Area: Apr consumer confidence is expected to edge up to -6.9 from -7.2, with sentiment having stabilised in recent months.

US: Mar new home sales are expected to bounce 4.9% following a 2.6% decline in Feb.

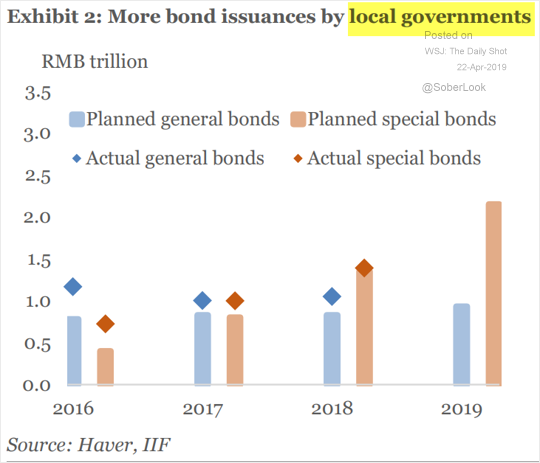

Readers will know that MB has shifted its outlook a little on surging Chinese credit. We are looking for a modest European rebound ahead as US growth slows. Some data supported this view over the break with Chinese bond issuance surging:

Advertisement

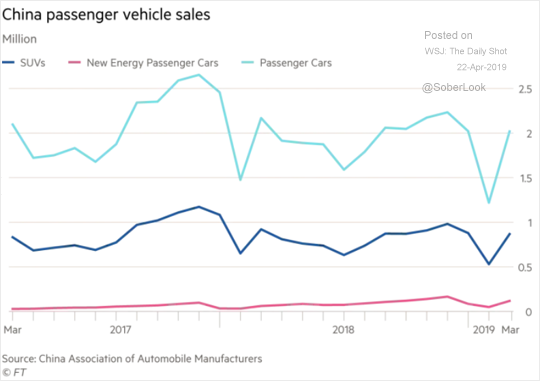

And car sales rebounding:

But it is still too early for Europe to track higher. PMI improved marginally in the second derivative but were mostly weak:

Advertisement

▪ Flash Eurozone PMI Composite Output Index(1) at 51.3 (51.6 in March). 3-month low.

▪ Flash Eurozone Services PMI Activity Index(2) at 52.5 (53.3 in March). 3-month low.

▪ Flash Eurozone Manufacturing PMI Output Index(4) at 48.1 (47.2 in March). 2-month high.

▪ Flash Eurozone Manufacturing PMI(3) at 47.8 (47.5 in March). 2-month high.

Given we are of the view that the recent surge in Chinese industrial production is complete horseshit, this is not surprising. It’s over H2 that we expect to see Europe firm as China’s credit deluge makes its way into firmer imports.

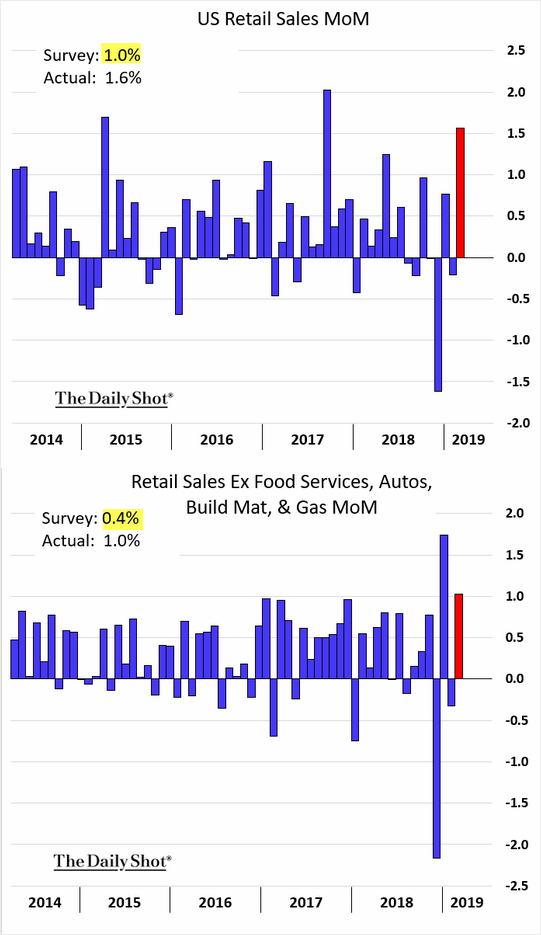

Meanwhile, US growth was mixed with a strongly rebounding consumer:

Advertisement

But still weakening property:

I hold no real fears for the US. There’s a further softening coming but no worse.

Advertisement

Until Europe firms up and improves relative to the US, the AUD will not rise.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.