Oil is running again as OPEC jawbones. US shale will not stand on ceremony:

Advertisement

Base metals were weak:

Big miners were all up:

EM stocks jumped with Shanghai:

Advertisement

Junk is powering with oil:

Treasuries were sold:

The bund curve flattened:

Advertisement

Stocks tacked on modest gains:

Westpac has the wrap:

Event Wrap

The National Homebuilders’ (NAHB) confidence gauge held steady at 62 in March; well down on the twenty-year highs hit early last year (72) but consistent with ongoing decent momentum in the US housing sector.

Event Outlook

NZ: Westpac consumer confidence rebounded from a six-year low in Dec 2018.

Australia: RBA Assistant Governor Financial Markets Kent speaks on “Bonds and Benchmarks”, Sydney 9 am. The Mar RBA minutes are released but are unlikely to contain many surprises given Governor Lowe spoke post the meeting, though note this was prior to the Q4 GDP release. The AusChamber-Westpac survey is released.

Euro Area: Mar ZEW survey of expectations was last at -16.6 in Feb – a still soft result but it has stabilised over the past three months.

US: Jan factory orders are expected to be flat following the preliminary durable goods orders estimate and Dec’s 0.1% gain.

So, why won’t the Australian dollar fall? Global conditions are not good and getting worse, via Capital Economics:

Advertisement

The continued weakness in key economic data, together with the recent abrupt change in tone by the European Central Bank, has prompted renewed questions about the health of the global economy. At times of heightened uncertainty, I think it’s useful to split any analysis into three parts: what we know, what we think we know and what we don’t yet know.

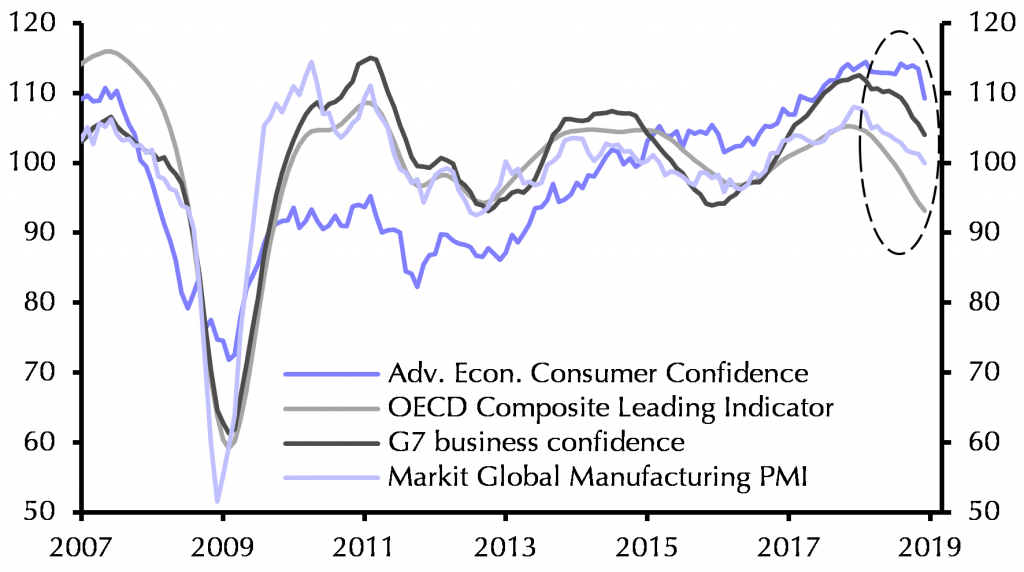

Let’s start with what we know. First and foremost, there’s growing evidence that the global economy is losing steam. As Chart 1 shows, a broad range of survey indicators have turned lower over the past quarter or so. All told, we reckon that global GDP growth has slowed from 3.8% y/y in the first quarter of last year to around 3% y/y now. That may not sound like a big deal but keep in mind that the IMF has previously suggested that a figure below 3% constitutes a global recession. So this looks serious.

Chart 1: Indicators of Economic Activity (Standardised, LR Avg = 100)

We also know that, while the slowdown in growth has been widespread, it has been particularly severe in Europe and, to a lesser extent, Asia. The US economy has held up relatively well so far, but the monthly activity data and business surveys are now pointing to a more marked slowdown in growth in Q1.

And we know that, at a sectoral level, manufacturing has borne the brunt of the downturn. The counterpart of this has been a sharp decline in global trade. In contrast, the service sector has been comparatively resilient.

What about the things that we think we know? These relate mainly to the causes of the downturn. One-off factors appear to have played a role in some countries, particularly in the euro-zone, where vehicle production has been affected by the disruption caused by new emissions regulations.

But something more fundamental also seems to be afoot. As we’ve noted before, the trade war between the US and China is likely to have had some effect on world growth, but this is only a small part of the story. Instead, as I argued a few weeks ago, the most likely explanation for the slowdown in global growth is that country-specific problems have started to weigh on activity in the world’s three major economic regions – the US, China and Europe – which have then been amplified through various feedback loops. In addition to this, it’s possible that political uncertainties are beginning to weigh on business investment in some countries (especially in Europe) and that a particularly large inventory cycle may be starting to unwind in the tech sector.

If all of this sounds a bit unsatisfactory then it’s worth bearing in mind that it’s common for global downturns to have their roots in several different areas. The last downturn in 2008-09 was unusual both because of its size but also because it had a single cause (debt and housing).

This leaves the things that we don’t yet know. The big question here is: how severe will this downturn be? It’s possible to envisage that all of this blows over relatively quickly. The one-off factors that have weighed on growth in some regions will fade, a trade truce between the US and China may help to shore up business sentiment and central banks may come to the rescue. It’s equally easy to see how things could spiral downwards. After all, the recovery from the 2008-09 crisis has been unusual in several respects: growth has been unusually weak, debt levels remain unusually high, policy has been unusually supportive and asset prices remain unusually high. Against this backdrop, it wouldn’t be a surprise if the global economy now experienced a sharp slowdown.

I suspect that the reality will lie somewhere in between. Growth in the euro-zone is likely to pick up over the next quarter or so as some of the headwinds that have been weighing on the region fade. Meanwhile, policy support should eventually help to stabilise growth in China, probably from the middle of this year. But at the same time new challenges will emerge. In particular, we expect that the US economy will remain weak through the course of 2019 and into 2020 as the sugar-high from last year’s fiscal stimulus wears off and the lagged effects of earlier Fed tightening weighs on interest rate sensitive sectors of the economy (notably housing).

The net result of this is likely to be that global growth remains depressed over the next year or so. We don’t anticipate a downturn on the same scale as 2008-09, but we do expect world GDP growth to fall below 3% y/y over the course of 2019-20. That would be a worse outcome than most analysts (and policymakers) currently anticipate – and it is likely to produce a combination of weaker stock markets, lower bond yields and renewed loosening by the world’s major central banks.

That’s my view. But it is not the view of markets, at least, not entirely, via FTAlphaville:

And once again, investors are bullish on emerging markets.

With the Fed on pause and trade tensions between the US and China ebbing, investors have been quick to forget the crises that hobbled emerging markets last year. But with investor sentiment shifting closer to “exuberance,” as one strategist puts it, and sources for further upside waning, the tide could soon turn against those who have been over-eager allocating money to emerging markets this year.

After a trying 2018, investors have poured billions into hard currency emerging market deb since January, with ten consecutive weeks of positive inflows, according to EPFR Global. Interest in the local currency denominated fixed income has lagged, but the swift uptick in hard currency debt has more than made up for it.

Here’s a chart from Citi’s James Barry showing the surge:

Sentiment has shifted a notch higher as well, approaching “exuberance” territory, according to David Hauner at Bank of American Merrill Lynch. To reach this conclusion, Hauner uses the firm’s EM Carry Sentiment Indicator, which tracks investor bullishness and bearishness, and a Bloomberg index tracking carry-trade returns from eight emerging markets (a popular carry trade is when investors borrow in dollars to buy higher yielding emerging market assets).

As the chart below shows, the EM Carry Sentiment Indicator has surpassed 80 (the light blue shaded area corresponding with the right-hand y-axis), while the Bloomberg EM carry index (the dark blue line corresponding with the left-hand y-axis) has bounced back from last year’s lows: A reading of 90 or higher means the “exuberance” threshold has been crossed, a level that historically precedes sell-offs. Despite this worrisome milestone, investors across Europe and the US surveyed by Hauner and his team seem unperturbed. The 80 or so investors the BofA strategists spoke to were “universally bullish,” and a recent BofA fund manager survey found “long EM” to be the most crowded trade.

That may soon change, however, because as Hauner points out, most of the good news bolstering the bullish case for emerging markets — namely the stabilising economic situation in China, the trade war stand-down, and the Fed’s dovish tilt — has already been priced in.

This reality is already cropping up in emerging market sovereign credit spreads. While they have tightened some 45 basis points so far this year, with emerging market returns closing in on 5 per cent, the pace has slowed this month. Total returns have fallen to just 0.5 per cent since February, and spread compression has stalled, with those for frontier markets actually widening.

Here’s a chart from Nafez Zouk of Oxford Economics showing this dynamic for emerging market debt, JPMorgan’s Emerging Market Bond Index ex-Venezuela and frontier markets:

What’s needed to propel emerging markets further following the Fed’s rate-hike pause is brighter growth prospects globally.

While Chinese officials have shown a willingness to pull monetary and fiscal levers to stimulate the economy, the growth situation there appears tenuous at best. In fact, analysts reckon growth in the People’s Republic will remain under pressure for many more months. A slower expansion will hamstring the government’s deleveraging efforts, so sky-high debt levels will continue to weigh on the country’s outlook. And in Europe, the doom-and-gloom is so dire that this month ECB president Mario Draghi had to again revive stimulus measures that the central bank had removed just two years prior.

Advertisement

Markets have tilted to embrace a new growth surge in EMs and commodities. This always delivers capital flows into Australia, the world’s only developed, emerging market. That lifts the AUD.

So, for the Australian dollar it is a case of domestic weakness and a widening negative yield spread deterring the carry trade versus global capital flows that want to buy global reflation as they see it (augmented in Australia’s case by the Vale accident). So far, the former has won out with a weak AUD and a the net market balance substantially short at CFTC:

Advertisement

But that makes the currency vulnerable to short squeezes as the EM trade continues.

Something will have to break to end this AUD impasse. Either EMs get materially better or Australia gets materially worse. I still think the latter is the base case as house price falls continue and bulk commodities join them regardless of an EM growth pick-up as the Vale crisis eases.

But investors should be ware that beyond the May election, political stability, new fiscal stimulus and RBA rate cuts may be enough to lift the AUD amid the EM trade for a time.

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund and MB Super which is long international equities and local bonds that will benefit from a weakening Australian economy and dollar so he is definitely talking his book.

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

A reading of 90 or higher means the “exuberance” threshold has been crossed, a level that historically precedes sell-offs. Despite this worrisome milestone, investors across Europe and the US surveyed by Hauner and his team seem unperturbed. The 80 or so investors the BofA strategists spoke to were “universally bullish,” and a recent BofA fund manager survey found “long EM” to be the most crowded trade.