Westpac: Housing slump to keep inflation lower for longer

By Justin Smirk, senior economist at Westpac

Key points:

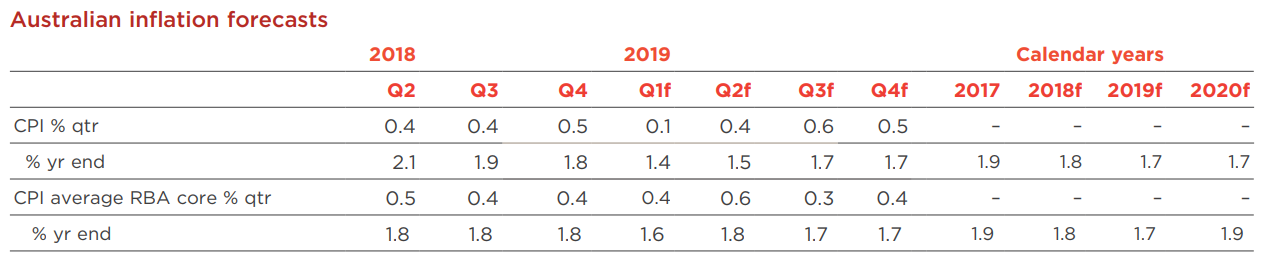

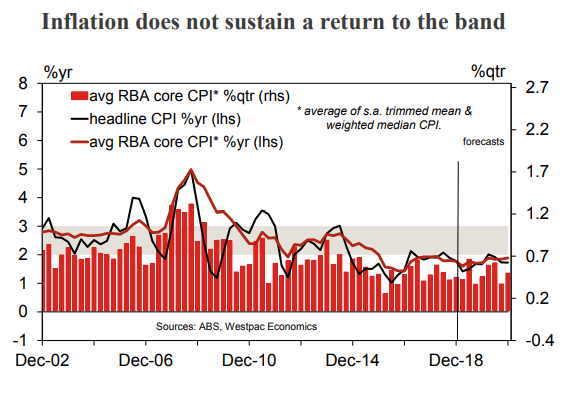

- The CPI rose 0.5%/1.8%yr in Q4; the average of the RBA core inflation measures rose 0.4%qtr/1.8%yr. Inflation continues to hold under the RBA’s target band and with the two quarter annualised pace running at 1.2% suggests it is unlikely get back into the band anytime soon.

- Moderating housing inflation has been key to containing inflation below the RBA target band. Even with our expectation for a modest lift in housing inflation through 2020, we still don’t see it being able to sustain inflation within the target band.

- With downside risks to dwellings and rents inflation in the CPI, downside risks are apparent for our forecasts for both headline and core inflation.

- The fall in unemployment through 2018, along with the depreciation of the AUD, should be pushing the pace of inflation through 2019. However, retail margins remain under pressure as household consumption slows and inflation expectations remain well anchored. As such, housing costs present the key risk to the inflation outlook.

- Our preliminary estimate for the March quarter 2019 CPI is 0.1%qtr /1.4%yr for headline and 0.4%qtr/1.6%yr for the average of the core measures.

Australian headline inflation surprised to the upside, finally

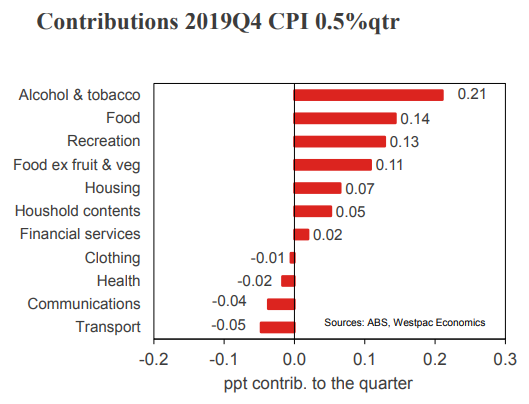

For the first time in two years the December quarter CPI exceeded market expectations rising 0.5% compared to a median expectation of 0.4%. Compared to Westpac’s expectations, what surprised to the upside included alcohol & tobacco (3.2% vs 2.8% expected), utilities (0.1% vs –0.3% expected), auto fuel (–2.5% vs –4.2% expected), household contents & services (0.5% vs –0.5% expected) and holiday travel (2.6% vs 1.6% expected). On the softer side, food rose just 0.9% (1.2% expected) and clothing & footwear fell –0.2% (a small rise was expected).

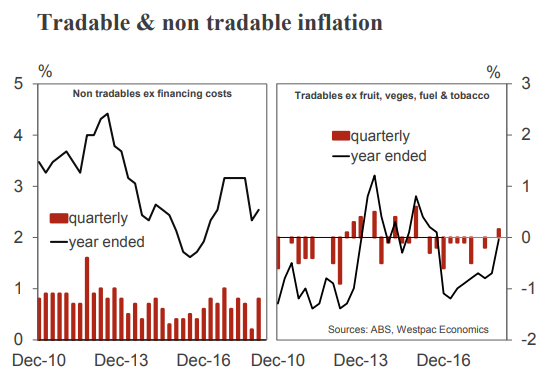

Tradables – AUD impact greater for services than goods

Looking at the tradable/non–tradable spit brings to the fore some key highlights. Tradables fell –0.3% in the December quarter. The tradable goods component fell –0.1% due to

automotive fuel (–2.5%), audio, visual & comp equipment (–3.3%) and wine (–1.9%). The tradable services component fell –0.7% due to international holiday travel & accommodation (–0.8%). Non–tradables rose 0.9% in the December quarter. The non–tradable goods component rose 1.5% due to the excise tax increase for tobacco (9.4%). The non–tradable services component rose 0.6%, due to domestic holiday travel & accommodation (6.2%).

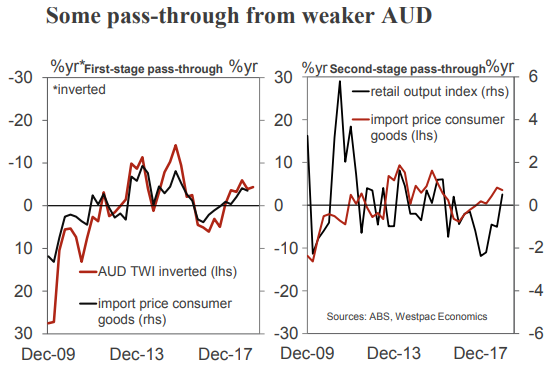

Some signs the AUD devaluation may be having an impact on retail prices

For some time now household contents & services prices have been experiencing downwards pressure but in the December quarter there were tentative signs of a turn around. Throughthe year this group reported a modest –0.8%yr fall but we are closely watching the +1%yr gains in appliances & furniture. ABS seasonally adjusted series suggests furniture prices lifted 2.5% in the last half of 2018 while major household appliances gained almost 5%. Are we now observing the impact of the weaker AUD on imported goods prices? Maybe, but we are cautious before we take this observation too far given our expectation for housing activity to moderate through 2019. In addition audio, visual & computing fell more than expected (–2.1%qtr vs –1.7%) to be down almost 5% in 2018 H2 on a seasonally adjusted basis.

Recreation rose 1.1%qtr vs our forecast for 0.4%qtr with the surprise coming from holiday travel (2.6%qtr vs 1.6%qtr) in response to an out–sized 6.2%qtr gain in domestic holiday

travel & accommodation. Domestic holiday & travel prices have risen 3.3% in the last half of 2018 on a seasonally adjusted basis but this is a small moderation from almost +4% in the first half of 2018 and the seasonally adjusted rise in Q4 was just 0.4%.

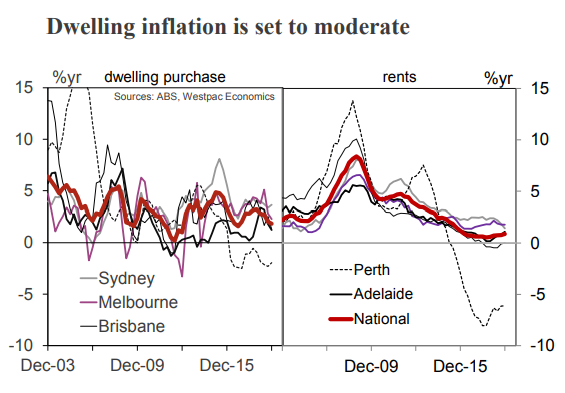

Housing holds the key for inflation momentum

The 0.2%qtr rise in housing costs resulted from a 0.2% rise in rents (a flat print was expected), dwelling purchases rose 0.4% (on par with expectations) while utilities prices were stronger at 0.1% vs. an expected –0.3% fall. Gas prices fell as expected but there was a surprisingly strong rise in Brisbane electrical prices. As housing has a significant group weighting in the CPI (15%) it has a meaningful impact on inflation.

Housing is also key to core inflation

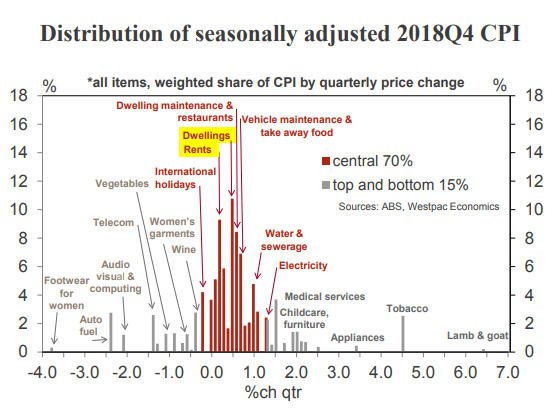

In December, the average of the core measures, which are seasonally adjusted and exclude extreme moves, rose 0.4%qtr meeting market expectations. In the quarter, the trimmed mean gained 0.43% while the weighted median lifted 0.36%. The annual pace of the average of the core measures held the 1.8% pace from Q3 following 1.8%yr in Q2. Incorporating revisions, the two quarter annualised growth in core inflation is only 1.5%yr well below the bottom of the RBA target band and the slowest pace since December 2016.

As the quarterly movement in dwelling and rents are not often in the extreme range they are rarely trimmed from the core measures. In December, dwellings prices were the median for the trimmed mean at 0.4%qtr. Also in the trimmed mean was rents (0.2%qtr), dwelling maintenance and restaurants (both 0.5%qtr), vehicle maintenance (0.6%qtr), water & sewerage (1.1%qtr) and electricity (1.3%qtr). Outside some near term modest risk for electricity & gas, it is hard to find reasons to expect an acceleration in housing inflation. In fact, considering dwelling purchase prices and rents, it is more likely that we will see a moderation rather than acceleration.

Medium term forecasting – bottom up

1) Housing costs

Dwelling purchase prices in the CPI measures the cost of constructing a new home; land values are not included. However that is not to say house prices, which include land

values, have no impact on the CPI. Changes in house prices will have an impact on the final prices builders sell their properties for and thus their margins. As such, dwelling purchase prices in the CPI can be influenced by reported house prices. It is also important to note that the dwelling purchase prices series includes apartments as well as detached houses.

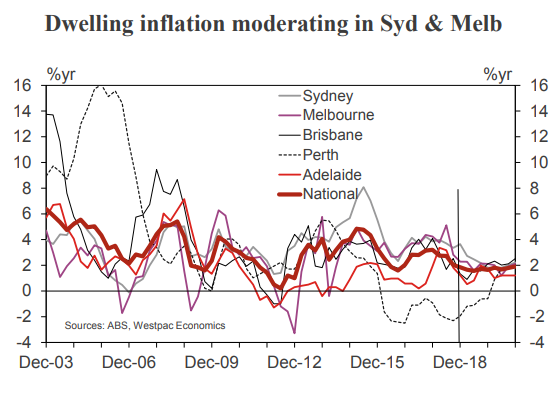

Westpac is forecasting dwelling price inflation to moderate from 1.8%yr in December 2018 to 1.4%yr by June 2019 before lifting a little to 1.7%yr by end 2019 to then be just under 2.0%yr by end 2020. Dwelling price inflation in Melbourne and Sydney is forecast to moderate to around 1.0%yr through 2019/2020 but by the end of 2020, both are back to around 2.0%. Brisbane dwelling price inflation eases a touch further through 2019 H1 before a modest recovery takes it back to 2.0%yr by end 2019 and 2½%yr by end 2020. Dwelling prices in Perth are forecast to continue to fall through the first half of 2019 before stabilising at around a –0.5%yr pace by year end before lifting to 2.0%yr by end 2020.

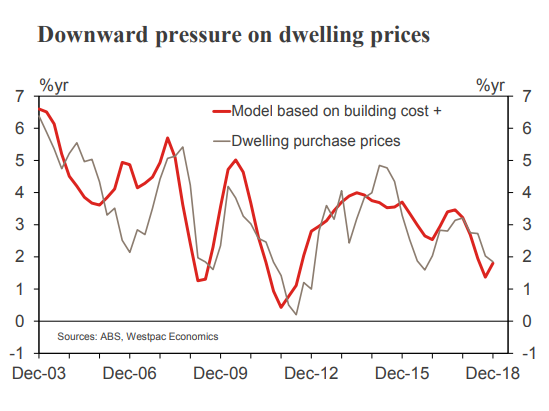

However, our research suggests the risk to this profile is to the downside. Westpac has been working with various building cost indexes to generate a bottom up (or cost push) profile for dwelling price inflation. Through 2018, dwelling construction cost inflation trended lower and our preliminary analysis suggests this could see dwelling purchase price inflation ease by more than we currently expect through the first half of 2019. This points to near term downside risks to our current dwelling price inflation profile while downside risks to the demand profile in 2020 suggests this disinflationary risk in dwelling prices could extend into a second year.

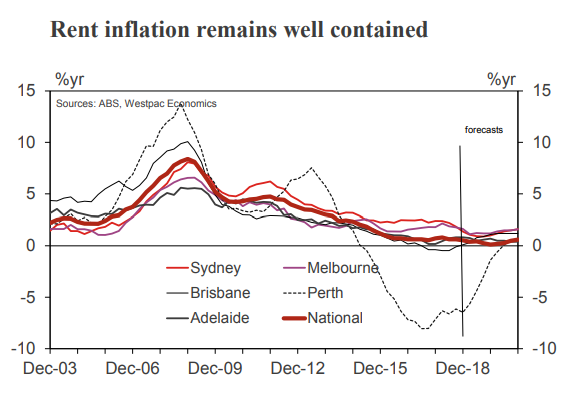

Annual rent inflation was running at just 0.5% in the December quarter and data on advertised rents suggest little prospect of a pick-up anytime soon. Rent inflation is trending lower in Sydney and vacancy rates have started to lift. Rents in Perth continue to fall while there are signs they may be stabilising in Brisbane. Our current forecasts have rent inflation finding a base at 0.4%yr in 2019 H1 before lifting to 0.9%yr by end 2020. For the near term we believe the risks to our rent forecasts lie to the downside.

Following significant increases in the previous years, utilities inflation, eased through 2018 from a 9.2%yr pace at the end of 2017 to 2.0%yr at end 2018. There has been a recent summer bump in wholesale electricity prices which is likely to reverse some of the discounting seen in power bills through 2018. Through 2019 we see electricity bills rising by 1.0%yr lifting further to 2.0%yr by end 2020. Gas & other fuels will continue to see upwards pressure, rising from 2.8%yr though 2019 to around 6%yr by end 2020, as local gas prices remain elevated due to constrained supply.

2) Auto fuels

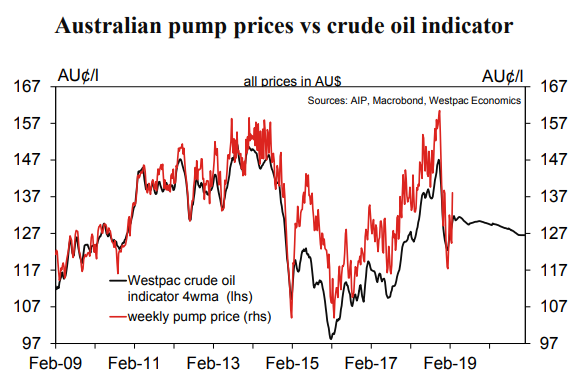

Auto fuels are set to be a significant drag in the March quarter. Pump prices started to fall in the December quarter and continued to fall into the March quarter. This has been driven by two factors: the sharp drop in crude oil prices (from a peak of US$85bbl in October 2018 to a recent low of US$60bbl in January 2019); plus the drop in gasoline refining margins as an oversupply of gasoline in Asia has put downward pressure on global gasoline prices. From here we are looking for oil prices to hold around US$65bbl through the first half of 2019 before easing back to a year end price of US$62bbl and then drifting down to US$60bbl through 2020. Through this time we are also forecasting the AUD to weaken to US68¢ by end September, holding that level to end 2019 before lifting back to US70¢ by end 2020.

On this basis we expect auto fuel prices to fall -6.8%yr to end 2019 (but it is worth noting that all of the fall occurs in Q1 with a modest recovery from there) and then be broadly flat through 2020.

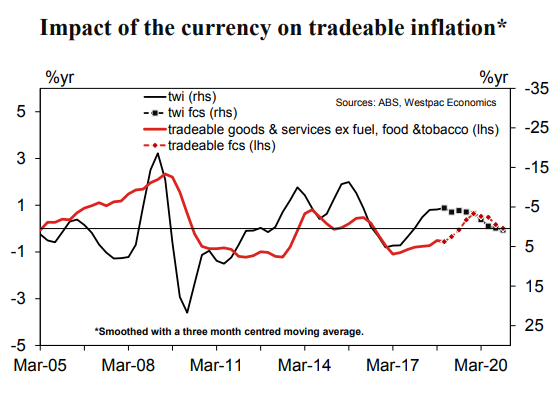

3) Weaker AUD to have a very modest impact, if at all

In trade weighted terms we are looking for the AUD to weaken a bit more than 3% through 2019 before being broadly flat through 2020.

Our forecasts have tradables rising 1.3%yr through 2019, and something similar through 2020, but if you exclude volatile fruit, vegetables, auto fuels & tobacco then tradables rise around 1% through 2019 and are broadly flat through 2020.

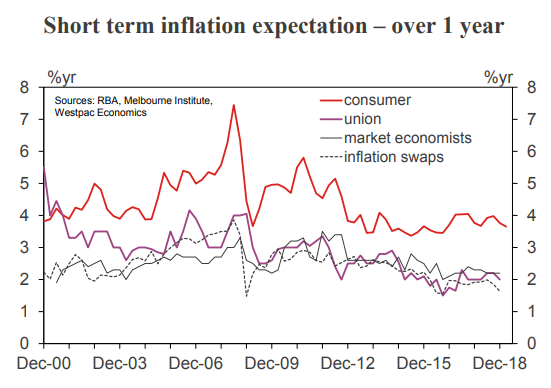

4) Inflationary expectations remain well contained

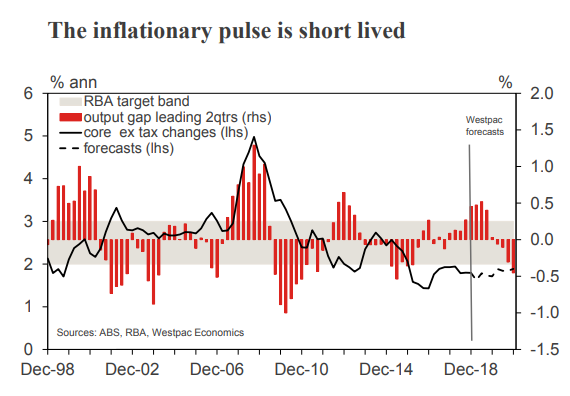

No matter how you measure them, from household sentiment surveys, market pricing via inflation index bonds or the various surveys of economists, unions or businesses, all suggest that inflationary expectations have responded to the extended period of low inflation and remain well contained. As such, given our expectation for the economy to slow through 2019

and excess capacity to increase, as represented by rising unemployment and a widening output gap, it is likely these expectations will remain stable with a small risk they could ease further.

Housing is the key risk to the inflation outlook

The stabilisation in housing cost inflation through 2019, which lifts a bit through 2020, is a key factor underpinning our forecast for headline inflation to get back towards the RBA’s target band. However, our forecasts just return inflation temporarily into the band in early 2020 before easing back to 1.7%yr by year end. For core inflation, the annual pace never gets any higher than 1.9%yr which it hits a couple of times through 2020. Also helping to lift inflation, even if somewhat modestly, is an assumption for some modest pass through from the weaker Australian dollar.

So if the risks to housing costs are to the downside and these risks are realised, then inflation is going to struggle to get back near the band; this is especially true for core inflation where housing’s components tend to have a bigger weight (30% of the index, by weight, is trimmed out of the core measures).

The December quarter of 2019 was the first time in two years that financial market inflation forecasters underestimated the quarterly rise in the CPI. We do not see this as a signal of the return of a more sustainable inflationary pulse.

Our preliminary estimate for the March quarter 2019 CPI is 0.1%qtr which would see the annual pace drift down to 1.4%yr. Our preliminary estimate for the average of the RBA core

measures in the March quarter is 0.4%qtr which sees the annual pace moderate 0.2ppt to 1.6%yr.