The Chicago Fed’s National Activity index – a composite index of 85 indicators that track US growth – came in at -0.29 in February, topping estimates but signaling subdued growth conditions in the new year.

The Dallas Fed’s manufacturing activity index eased to 8.3 in March from 13.1, a touch below estimates. The detail shows new orders falling to two-year lows.

GermanIFO business survey for March beat forecasts, posting gains from last month across all three categories: business climate 99.6, est. 98.5, prior 98.7; expectations 95.6, est. 94.0, prior 94.0; current assessment 103.8, est. 102.9, prior 103.6.

Brexit: EU published their preparations for a “no-deal” Brexit which the EU see as rising in potential. PM May announced to Parliament that she does not have sufficient support for her twice defeated deal and so will hold off from tabling it for another vote but still sees it as the best option and proposes to push for further support to table the deal once more. The UK tonight will vote on whether Parliament will take control of the Parliamentary timetable, away from the Government, in order to determine what will be debated in order to seek Brexit solutions/proposals.

Event Outlook

NZ: Feb’s trade balance is expected to be -$200m, a smaller deficit than Jan’s -$914m, as exports rise and imports fall.

Australia: RBA Assistant Governor (Economic) Ellis speaks at the HIA Industry Outlook, Sydney 7:30 am.

Euro Area: German and French consumer confidence is released.

US: Mar Conference Board consumer confidence is anticipated to edge up to 132.0 from 131.4. Feb housing starts and building permits are released. Jan FHFA house prices and S&P/CS home price index are expected to show moderate growth in home prices. Fedspeak involves Rosengren and Evans in Hong Kong, Harker at an ECB/Bundesbank event, and Daly discusses managing inflation in the current environment.

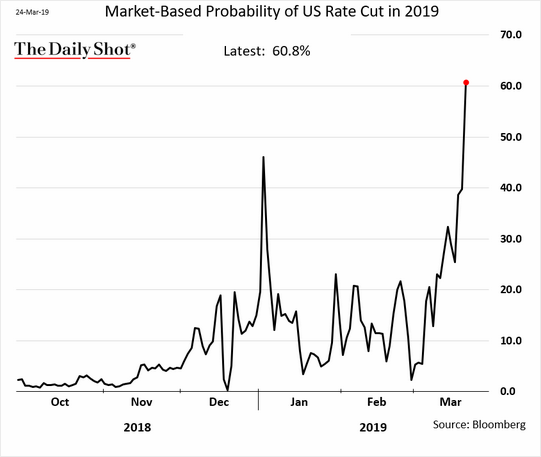

Bloody strange market action. The US economy and outlook is much better than the Australian yet markets have now priced a full rate cut into the short end of the yield curve in the US versus none in Australia.

Advertisement

Do bond markets seriously content that the risk of rate cuts is higher in the US than Australia? More from Westpac:

How much further can they go? Does this tell us anything about timing of a cut? There are 2 questions on my mind as we enter the new trading week at or near all-time lows in yields. First, now that 3yr bond yields are trading significantly below cash, what does that usually mean for the timing of the first rate cut, and second, has the RBA ever disappointed the market when this much has been factored-in? The charts at right and middle attempt to provide some insights into the first of these questions. Ahead of each phase of the easing cycle that began back in late 2011, 3yr bonds have spent time below cash, in some cases significantly so. The middle chart shows that as the easing cycle has extended to record low cash rates, the degree to which 3yr bond yields moved below cash has fallen. That is not unexpected. As can be seen the range in 2016 was -30bp to +8bp and the first time 3yr yields when below the prevailing cash rate was 4 months before the delivery of the rate cut. In prior periods, however, it was as short as 70 days. We have currently been negative for around a week, so there is still some time to go and our assessment suggests that there is as much as 15-20bp of 3yr outperformance possible. That will be determined by how extended the easing cycle is expected to be (right chart). History shows that when the rate cut is delivered the market has tended to underestimate how far the RBA could ease (although August 2016 was an exception). We do not think that will be the case this time, as we expect that the market will not quickly factor-in significantly higher rates.

Meanwhile, globally, Europe is still worse than the US as well:

Advertisement

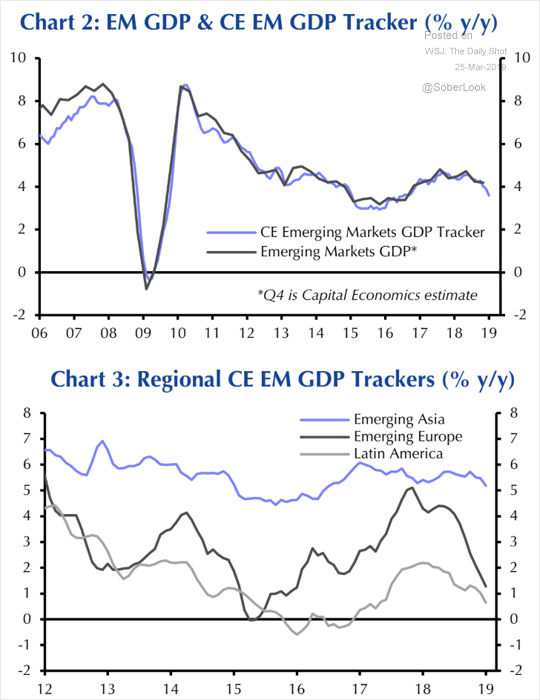

EMs are too, led by China:

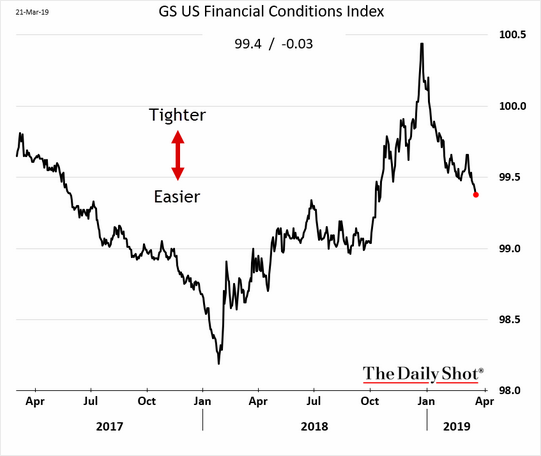

And the US has already eased:

Advertisement

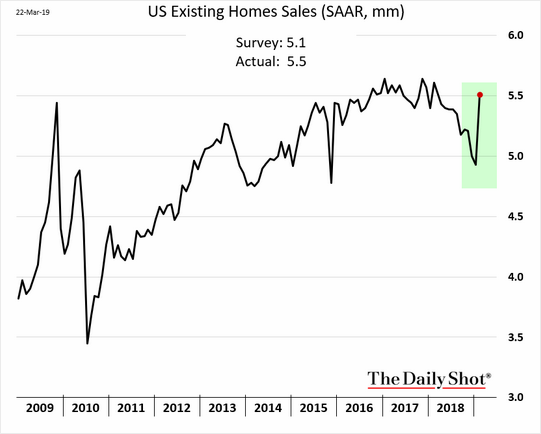

With success:

Yet this:

Markets appear distorted around views of central bankers rather than focused on respective economies. They’ve gone all-in on the politics of a dovish Fed that has no reason to cut and are still far behind the reality of a dying Aussie economy owing to a lunatic RBA.

Advertisement

In due course I expect this situation to be mugged by reality with more downside for the AUD and upside to Aussie bonds.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.