Over the past few years, senior Coalition ministers claimed repeatedly that Labor’s negative gearing policy would destroy both the housing market and economy.

For example, in February 2017, then Prime Minister Malcolm Turnbull claimed Labor’s negative gearing changes would “smash the residential housing market” and warned that “every homeowner in Australia has a lot to fear from Bill Shorten”.

In a similar vein, in June 2017 then Treasurer Scott Morrison stated on ABC’s The Business that “Changing negative gearing is not an ambitious reform, it’s a bad idea. It’s going to undermine the value of people’s homes and it’s going to crash house prices”.

Today, the ABC has released a Freedom of Information request from the Australian Treasury, which undermines the Coalition’s claims about the dire impact on the housing market from Labor’s proposed reforms:

Since 2016, the Coalition has continued to claim the plan would “smash” housing values with a “sledgehammer”.

But it can now be revealed Treasury explicitly told the Government it should not even claim home values “will” fall under the proposal…

Emails obtained by the ABC reveal that last January… the department sent back the following correction:

“The … statement is not consistent with our advice.

“We did not say that the proposed policies ‘will’ reduce house prices.

“We said that they ‘could’ put downward pressure on house prices in the short-term depending on what else was going on in the market at the time.

“But in the long-term they were unlikely to have much impact.”

Labor’s Shadow Treasurer Chris Bowen said “the Government’s been caught red-handed” misrepresenting official advice…

Treasury appears to have maintained its view about the likely impact of the ALP’s negative gearing and capital gains policy on prices in the three years since it was announced…

“This is quite a significant revelation,” Mr Bowen said.

“[The Government should] stop abusing the Treasury processes, abusing the independence of the Treasury, misrepresenting what the Treasury has said.”

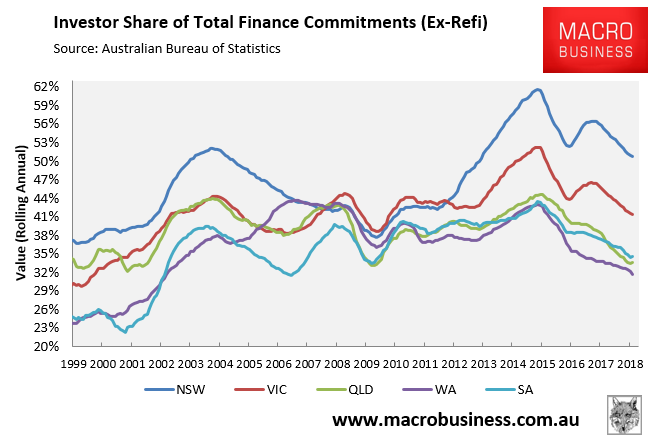

MB does not agree with the Australian Treasury’s assessment that Labor’s policy are “unlikely to have much impact” over the long-term. We see it having a significant impact in Sydney and Melbourne where investors are most prevalent, but less elsewhere:

Nevertheless, neither do we see Labor’s policy as being calamitous either. Now is actually a good time to implement Labor’s policy. Since investor demand has already crashed, there is far less risk of investor flight and widespread market disruption than if investor demand was running at the extreme levels of two years ago.

What Labor’s policy will do, however, is prevent a future investor bubble, moderate the cycle, and boost the first home buyer share over the longer-term.

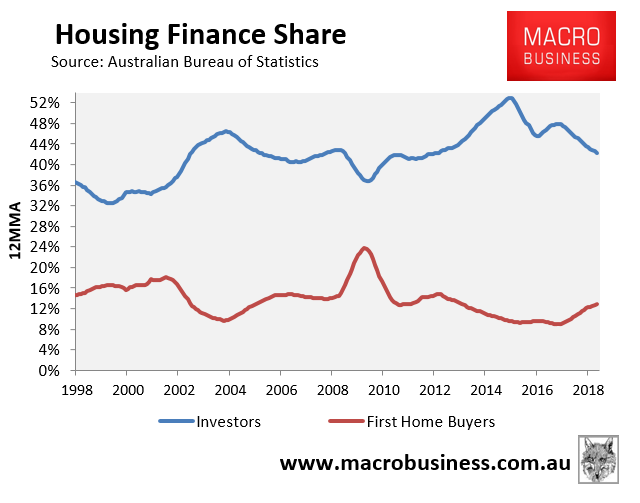

Finally, and related to the above, Labor’s policy should also improve home ownership rates, given the strong negative correlation between investors and first home buyers:

That is, as the share of investors in the market rises, the share of FHBs falls proportionately.

Therefore, any reduction in investor demand arising from Labor’s policy would unambiguously benefit FHBs, who would no longer be crowded-out. And by making investment in existing housing less attractive, home ownership rates should improve.