A much better than expected finish to the week here in Asia for share markets, with Chinese bourses leading the way while Japanese markets finally gain some strength following the USD wide rally that is suppressing Yen in the main. The Australian dollar remains stubborn while the Kiwi is also trying to get off its self induced bottom from the RBNZ earlier in the week.

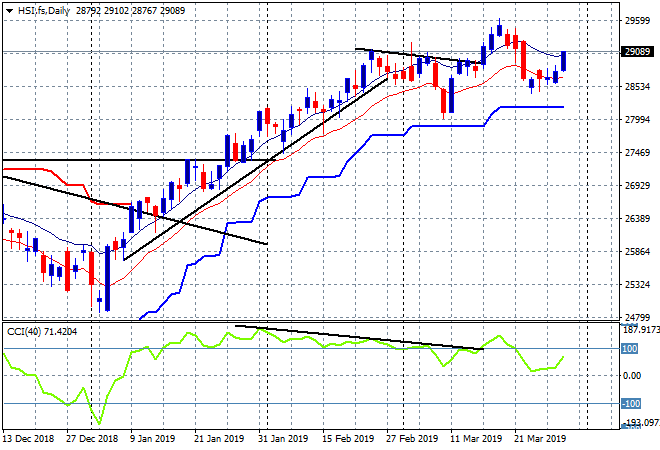

The Shanghai Composite has launched nearly 3% higher to zoom straight through 3000 points and is nearing 3100 going into the close, while the Hong Kong Hang Seng Index is up nearly 1% higher to 29048 points. Momentum remains in the positive zone as price respects the previous daily lows at the 28500 point level and looks to end the month above the February high:

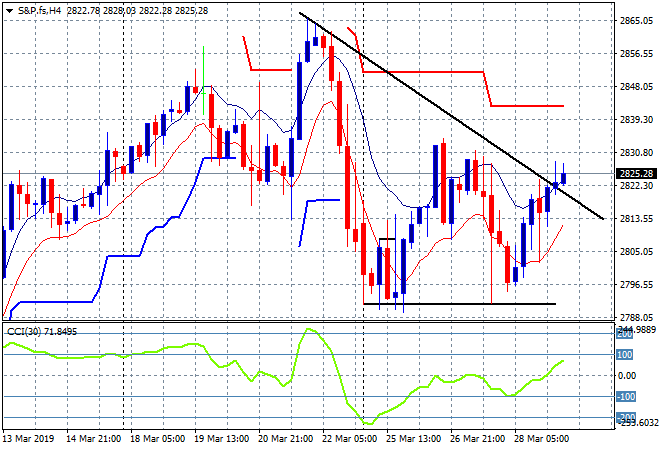

US and Eurostoxx futures are slowly lifting going into tonight’s session with the four hourly chart of the S&P 500 again looking to break the downtrend from last Friday’s reversal and finish the month above the 2800 points key level amid this yield curve inversion test:

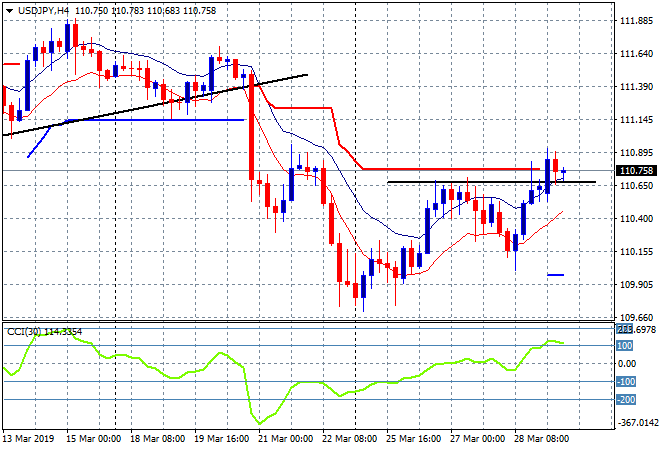

Japanese stock markets are gaining some traction because of a weaker Yen, with the Nikkei 225 looking to close 0.9% higher to 21215 points, after looking to threaten key support at the 20600 level throughout the week. The USDJPY pair has pushed above trailing ATR resistance at the 110.70 level, making a new intrasession high for the week but can it stick this tonight:

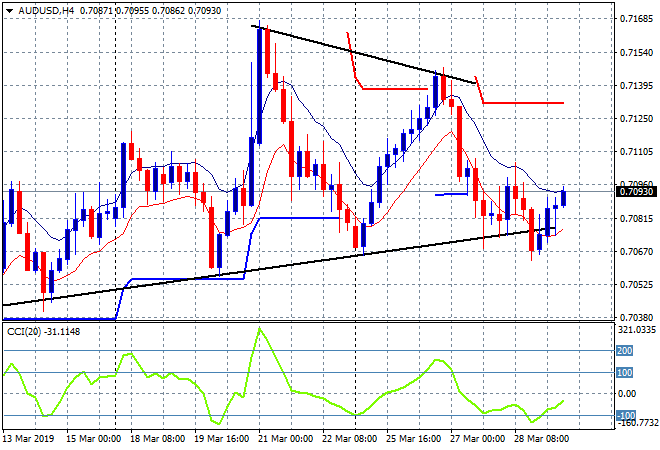

The ASX200 is having a scratch session today, only able to close a few points higher to 6180 points, still shy below staunch resistance at 6200 points but at least still showing some signs of life. The Australian dollar continues to find buying support just below the 71 handle. The series of higher lows on the four hourly/daily charts since the start of March is still supporting the Pacific Peso, but this looks to be a swing move only with last week’s high at 71.60 a bridge too far:

The economic calendar finishes the week with two major releases – German unemployment (the only number that matters on the continent) and US PCE or personal consumption expenditure for January.

Have a great weekend!