Asian share markets are having another mixed session despite the positive sentiment from overnight with all eyes still on the bond markets, particularly the Australian. The Aussie dollar took a dive in sympathy with the Kiwi as the RBNZ signalled another possible rate cut is on the way while Yen remained soft against USD.

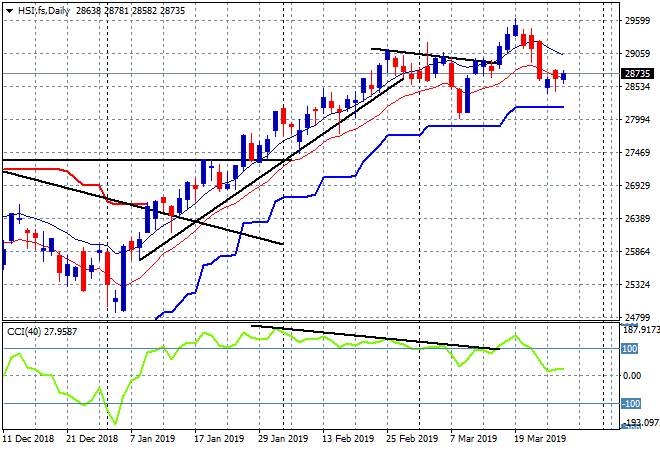

The Shanghai Composite is hanging on just above 3000 points going into the close, currently up 0.4% to 3009 while the Hong Kong Hang Seng Index is doing even better, up over 0.5% to 28723 points. This keeps momentum in the positive zone and respecting the previous daily lows at the 28500 point level, but it’s still looking weak here:

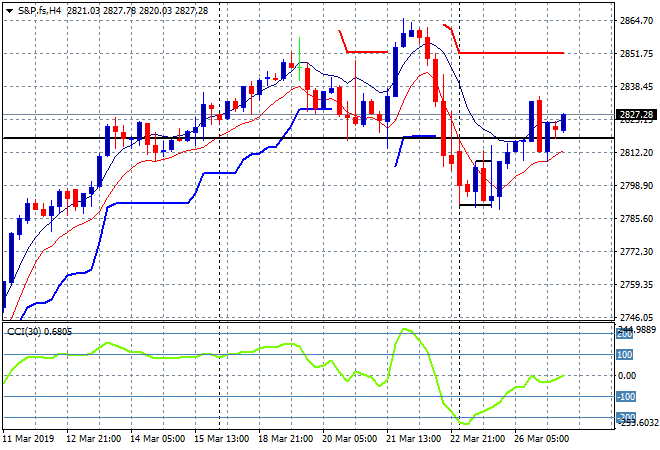

US and Eurostoxx futures are rising going into tonight’s session with the four hourly chart of the S&P 500 continuing its bounce off support at the 2800 points key level with a retest of the previous high at 2860 points still probable as the week rolls on:

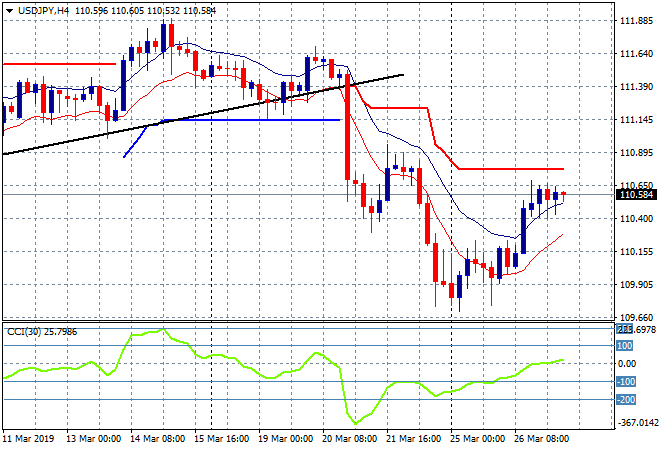

Japanese stock markets have failed to continue their own bounce back, with the Nikkei 225 closing 0.2% lower to 21378 points, but still maintaining a good distance above key support at the 20600 level. The USDJPY pair is still unable to gain any upside traction here, not filling last night bounce as it comes up to trailing ATR resistance at the 110.70 level on the four hourly chart:

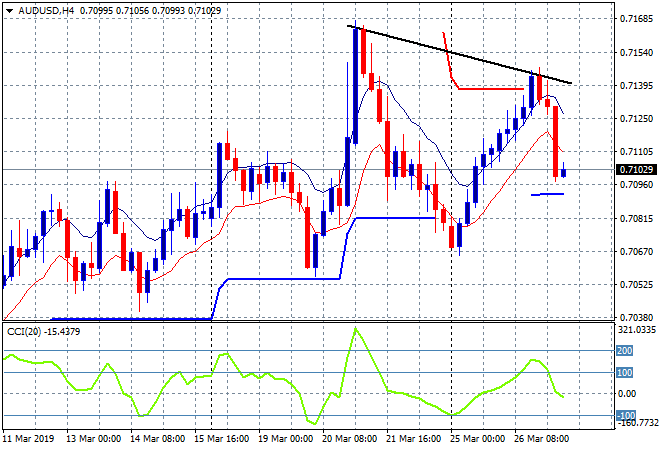

The ASX200 is up a few points again, closing only 0.1% higher to 6136 points to remain well below staunch resistance at 6200 points. The Australian dollar swiftly reversed all of the previous two nights gains as the Kiwi dropped over one handle lower on the RBNZ shift. The 71 handle is the support level to watch going into tonights session as this rally failedto push up to last week’s high at 71.60:

The economic calendar continues tonight with no big releases, rather a series of central banker speeches, starting with Super Mario but finishing the night with oil sensitive DOE inventory data.